Dan’s Biz Bookshelf: ‘Dream First, Details Later

Dan’s Biz Bookshelf: ‘Dream First, Details Later Happy’s Tech Talk #40: Factors in PTH Reliability—Hole Voids

Happy’s Tech Talk #40: Factors in PTH Reliability—Hole Voids Facing the Future: Time for Real Talk, Early and Often, Between Design and Fabrication

Facing the Future: Time for Real Talk, Early and Often, Between Design and Fabrication

Inventory and Processor Supply Issues Weigh Against Holiday PC Shipments

January 11, 2019 | IDCEstimated reading time: 5 minutes

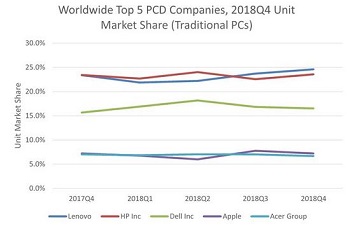

Preliminary results for the fourth quarter of 2018 (4Q18) showed shipments of traditional PCs (desktop, notebook, and workstation) totaled just over 68.1 million units, marking a decline of 3.7% in year-on-year terms, according to the International Data Corporation (IDC) Worldwide Quarterly Personal Computing Device Tracker. The results slightly outperformed the forecast, which called for a decline of 4.7%, but also produced the largest year-on-year decline since the third quarter of 2016 (3Q16) and capped the full year at a nearly flat rate of -0.4%.

Heading into the quarter there was industry-wide concern over processor shortages and rising economic tensions between the U.S. and China. Aggressive stocking of inventory during the previous quarter (3Q18) in anticipation of the shortage led to some sell-through challenges, driving a reduction of Q4 shipments in some regions. The fourth quarter is typically oriented toward consumer promotions that help drive the industry's biggest quarter of the year, but the confluence of events in 2018 led to the lowest sequential growth for a holiday quarter since the fourth quarter of 2012.

Nonetheless, the market performed better than expected, with corporate PC refresh—driven by the looming Windows 7 end of life (EOL) in January 2020—helping to offset consumer market challenges. Japan had an especially strong quarter driven by commercial refresh, which lifted virtually all aspects of the market. All regions except the U.S. exceeded the forecast, although Asia/Pacific (excluding Japan) faced challenges from a difficult Chinese commercial environment.

"The ongoing economic tensions between China and the United States continue to create a lot of uncertainty in the business environment in China. As demand for Chinese products in the U.S. drops, this particularly impacts businesses of all sizes from the manufacturing sector in China, which, in turn, translates to a drop in IT purchases by these companies," said Maciek Gornicki, research manager with IDC's Asia/Pacific Client Devices Group. "As a result, the PC market in China is expected to suffer bigger declines throughout the year. And if the trade war escalates further, we should expect spillover of the impact to other countries, particularly due to the expected fluctuations of the exchange rates impacting businesses across the region."

"As the U.S. PC market, especially the lower-end, continued to suffer from the ongoing shortfall of Intel CPUs, overall PC sales took a hit during the fourth quarter of 2018," said Neha Mahajan, senior research analyst with IDC’s Devices and Displays Group. "While the processor supply challenges are expected to continue into the first two quarters of 2019, PC makers are likely to see the situation improve before the back-to-school season begins during the latter half of the year."

Regional Highlights

USA: The traditional PC market in the U.S. saw a modest uptick in volume from the year prior. Total shipments for the quarter reached 16.7 million units, which was slightly below forecast. Commercial shipments remained fairly robust during the quarter, thanks to the ongoing Windows 10 refresh cycle. While market leader HP saw its year-over-year volumes modestly decline (despite a quarter-over-quarter improvement), the other top five vendors mostly saw volumes improve.

Europe, Middle East and Africa (EMEA): The traditional PC market was negative in 4Q18 for the first time in six quarters with both desktop and notebooks reporting a moderate decline. This weakening of the market stemmed from the ongoing component shortages and was further impacted by a level of disruption and uncertainty arising from challenging geopolitical and economic scenarios within major economies in the region.

Asia/Pacific (excluding Japan) (APeJ): The traditional PC market in APeJ posted a single-digit decline in 4Q18, which was relatively close to IDC's forecast. Overstock in the channels, coupled with Intel CPU shortages, impacted sell-in across the region. In India, a significant drop in consumer demand together with high inventory remaining in the channels led to a stronger than expected decline in the consumer and SMB segments, while Intel supply shortages led to a drop in sales to the enterprise customers. In China, the commercial PC market came in below expectations, impacted by Intel CPU shortages and slowness in spending from the public sector, while U.S.-China trade issues had a negative effect on demand from the private sector.

Japan: Corporate Windows 10 refresh entered its final phase and helped to beat expectations for 4Q18, with growth among virtually all OEMs, although multinational OEMs reaped most of the benefits.

Page 1 of 2

Share on:

Suggested Items

Microchip Expands Space-Qualified FPGA Portfolio with New RT PolarFire® Device Qualifications and SoC Availability

07/10/2025 | MicrochipContinuing to support the evolving needs of space system developers, Microchip Technology has announced two new milestones for its Radiation-Tolerant (RT) PolarFire® technology: MIL-STD-883 Class B and QML Class Q qualification of the RT PolarFire RTPF500ZT FPGA and availability of engineering samples for the RT PolarFire System-on-Chip (SoC) FPGA.

Infineon Advances on 300-millimeter GaN Manufacturing Roadmap as Leading Integrated Device Manufacturer (IDM)

07/10/2025 | InfineonAs the demand for gallium nitride (GaN) semiconductors continues to grow, Infineon Technologies AG is poised to capitalize on this trend and solidify its position as a leading Integrated Device Manufacturer (IDM) in the GaN market.

Bell to Build X-Plane for Phase 2 of DARPA Speed and Runway Independent Technologies (SPRINT) X-Plane Program

07/09/2025 | Bell Textron Inc.Bell Textron Inc., a Textron Inc. company, has been down-selected for Phase 2 of Defense Advanced Research Projects Agency (DARPA) Speed and Runway Independent Technologies (SPRINT) X-Plane program with the objective to complete design, construction, ground testing and certification of an X-plane demonstrator.

2025 ASEAN IT Spending Growth Slows to 5.9% as AI-Powered IT Expansion Encounters Post-Boom Normalization

06/26/2025 | IDCAccording to the IDC Worldwide Black Book: Live Edition, IT spending across ASEAN is projected to grow by 5.9% in 2025 — down from a robust 15.0% in 2024.

DownStream Acquisition Fits Siemens’ ‘Left-Shift’ Model

06/26/2025 | Andy Shaughnessy, I-Connect007I recently spoke to DownStream Technologies founder Joe Clark about the company’s acquisition by Siemens. We were later joined by A.J. Incorvaia, Siemens’ senior VP of electronic board systems. Joe discussed how he, Rick Almeida, and Ken Tepper launched the company in the months after 9/11 and how the acquisition came about. A.J. provides some background on the acquisition and explains why the companies’ tools are complementary.