The Marketing Minute: Cracking the Code of Technical Marketing

The Marketing Minute: Cracking the Code of Technical Marketing Trouble in Your Tank: Implementing Direct Metallization in Advanced Substrate Packaging

Trouble in Your Tank: Implementing Direct Metallization in Advanced Substrate Packaging

Semiconductor Shipments Dominated by Opto-Sensor-Discrete Devices

March 10, 2017 | IC InsightsEstimated reading time: 3 minutes

Annual total semiconductor unit shipments (integrated circuits and opto-sensor-discrete, or O-S-D, devices) are forecast to continue their upward march in the next five years and are now expected to top one trillion units for the first time in 2018, according to data presented in IC Insights’ soon to be released March Update to the 2017 edition of The McClean Report—A Complete Analysis and Forecast of the Integrated Circuit Industry, and the 2017 O-S-D Report—A Market Analysis and Forecast for the Optoelectronics, Sensors/Actuators, and Discretes.

Semiconductor shipments totaled 868.8 billion in 2016 and are forecast to top one trillion units in 2018. Figure 1 shows that semiconductor unit shipments are forecast to climb to 1,002.6 billion devices in 2018 from 32.6 billion in 1978, which amounts to average annual growth of 8.9% over the 40 year period and demonstrates how dependent on semiconductors the world has become.

Figure 1

The largest annual increase in semiconductor unit growth during the timespan shown was 34% in 1984, and the biggest decline was 19% in 2001 following the dot-com bust. The global financial meltdown and ensuing recession caused semiconductor shipments to fall in both 2008 and 2009; the only time that the industry experienced consecutive years in which unit shipments declined. Semiconductor unit growth then surged 25% in 2010, the second-highest growth rate across the time span.

Despite advances in integrated circuit technology and the blending of functions to reduce chip count within systems, the percentage split of IC and O-S-D shipments within total semiconductor units remains heavily weighted toward the O-S-D category. In 2016, O-S-D devices accounted for 72% of total semiconductor units compared to 28% for ICs. Thirty-six years ago in 1980, O-S-D devices accounted for 78% of semiconductor units and ICs represented 22% (Figure 2).

Figure 2

Surprisingly, shipments of commodity-filled discretes devices category (transistor products, diodes, rectifiers, and thyristors) accounted for 44% of all semiconductor unit shipments in 2016. The long-term resiliency of discretes is primarily due to their broad use in all types of electronic system applications. Consumer and communications applications remain the largest end-use segments for discretes, but increasing levels of electronics being packed into vehicles for greater safety and fuel efficiency have boosted shipments of discretes to the automotive market as well. Discretes are used for circuit protection, signal conditioning, power management, high current switching, and RF amplification. Small signal transistors are still used in and around ICs on board designs to fix bugs and tweak system performance.

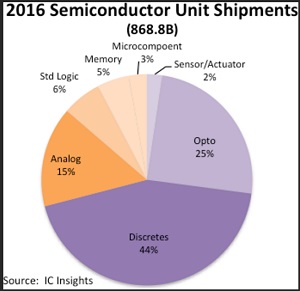

Among ICs, analog products accounted for the largest number of shipments in 2016. Analog ICs represented 52% of IC unit shipments in 2016, but only 15% of total semiconductor units. Figure 3 shows the split of semiconductor unit shipments by product type in 2016.

For 2017, semiconductor products showing the strongest unit growth rates are those that are essential building-block components in smartphones, new automotive electronics systems, and within systems that are helping to build out of Internet of Things. Some of the fast-growing IC unit categories for 2017 include Consumer—Special Purpose Logic, Signal Conversion (Analog), Auto—Application-Specific Analog, and flash memory. Among O-S-D devices, CCDs and CMOS image sensors, laser transmitters, and every type of sensor product (magnetic, acceleration and yaw, pressure, and other sensors) are expected to enjoy strong double-digit unit growth this year. More coverage about these semiconductor products and end-use applications are included in the 2017 editions of IC Insights’ McClean Report and O-S-D Report.

Further details on IC, O-S-D, and total semiconductor unit and market trends are provided in the 2017 editions of two reports from IC Insights. The McClean Report—A Complete Analysis and Forecast of the Integrated Circuit Industry is IC Insights’ flagship report covering the IC market. A subscription to The McClean Report includes free monthly updates from March through November (including a 250+ page Mid-Year Update), and free access to subscriber-only webinars throughout the year. An individual-user license to the 2017 edition of The McClean Report is priced at $4,090 and includes an Internet access password. A multi-user worldwide corporate license is available for $7,090.

IC Insights expands its coverage of the semiconductor industry with its 360-page O-S-D Report—A Market Analysis and Forecast for the Optoelectronics, Sensors/Actuators, and Discretes (released in late March 2017). Details in this one-of-a-kind report include a detailed forecast of sales, unit shipments, and selling prices for more than 30 individual product types and categories through 2021. Also included is a review of technology trends for each of the major segments. The 2017 O-S-D Report, with more than 240 charts and figures, is priced at $3,590 for an individual-user license and $6,690 for a multi-user corporate license.

Share on:

Testimonial

"In a year when every marketing dollar mattered, I chose to keep I-Connect007 in our 2025 plan. Their commitment to high-quality, insightful content aligns with Koh Young’s values and helps readers navigate a changing industry. "

Brent Fischthal - Koh YoungSuggested Items

Knocking Down the Bone Pile: Best Practices for Electronic Component Salvaging

09/17/2025 | Nash Bell -- Column: Knocking Down the Bone PileElectronic component salvaging is the practice of recovering high-value devices from PCBs taken from obsolete or superseded electronic products. These components can be reused in new assemblies, reducing dependence on newly purchased parts that may be costly or subject to long lead times.

On the Line With… Podcast: UHDI and RF Performance

09/17/2025 | I-Connect007I-Connect007 is excited to announce the release of a new episode in its latest On the Line with... podcast series, which shines a spotlight on one of the most important emerging innovations in electronics manufacturing: Ultra-High-Density Interconnect (UHDI).

The Marketing Minute: Cracking the Code of Technical Marketing

09/17/2025 | Brittany Martin -- Column: The Marketing MinuteMarketing is never a one-size-fits-all endeavor, but the challenges are magnified for highly technical industries like electronics. Products and processes are complex, audiences are diverse, and the stakes are high, especially when your customers are engineers, decision-makers, and global partners who depend on your expertise.

EV Group Achieves Breakthrough in Hybrid Bonding Overlay Control for Chiplet Integration

09/12/2025 | EV GroupEV Group (EVG), a leading provider of innovative process solutions and expertise serving leading-edge and future semiconductor designs and chip integration schemes, today unveiled the EVG®40 D2W—the first dedicated die-to-wafer overlay metrology platform to deliver 100 percent die overlay measurement on 300-mm wafers at high precision and speeds needed for production environments. With up to 15X higher throughput than EVG’s industry benchmark EVG®40 NT2 system designed for hybrid wafer bonding metrology, the new EVG40 D2W enables chipmakers to verify die placement accuracy and take rapid corrective action, improving process control and yield in high-volume manufacturing (HVM).

ROHM Develops Ultra-Compact CMOS Op Amp: Delivering Industry-Leading Ultra-Low Circuit Current

09/11/2025 | ROHMROHM’s ultra-compact CMOS Operational Amplifier (op amp) TLR1901GXZ achieves the industry’s lowest operating circuit current.