The Marketing Minute: Cracking the Code of Technical Marketing

The Marketing Minute: Cracking the Code of Technical Marketing Trouble in Your Tank: Implementing Direct Metallization in Advanced Substrate Packaging

Trouble in Your Tank: Implementing Direct Metallization in Advanced Substrate Packaging

TrendForce Projects Contract Prices of Server DRAM Modules to Increase in Q3

June 15, 2017 | TrendForceEstimated reading time: 2 minutes

DRAMeXchange, a division of TrendForce, reports that the average contract price of server DRAM modules rose sequentially by nearly 40% and 10% respectively for the first and second quarter of 2017 due to tight supply. In the third quarter, the average contract price of 32GB server DRAM modules for first-tier customers is projected to arrive around US$260, while the average contract price of 32GB modules for second-tier customers may be higher than that threshold. The latest forecast by DRAMeXchange indicates that the average sequential price increase for server DRAM modules in the contract market for the third quarter will be in the range between 3% and 8%.

According to DRAMeXchange analyst Mark Liu, server DRAM modules are supporting higher data transfer bandwidths, from 2133MHz and 2400MHz to 2666MHz. In terms of capacity, the mainstream modules have also expanded to 32GB. “Going into the second half of 2017, the growth in the memory content per box for servers and the increase in the market penetration of 32GB product lines are expected to be the main demand drivers,” said Liu. DRAMeXchange projects that the penetration of 32G capacity option in the total server DRAM module shipments will surpass 60% by the end of 2017.

Shortage of server DRAM modules will not ease any time soon as the server market is expected to get hotter in the second half of 2017

Looking at the server market, product orders during the second half of 2017 will be mostly related to the procurement contracts that were made in the year’s first half by data center operators, enterprises and government organizations. Furthermore, a sizable part of this demand will be for servers based on Intel’s Purley platform. The initial shipments of Purley-based servers are expected to mostly go to data centers that will be replacing outdated hardware. As for enterprise servers with Purley solutions, their market releases are mainly scheduled in the first quarter of 2018. The market penetration of high-capacity modules such as 32GB RDIMMs and 64GB LRDIMMs is expected to accelerate with the arrival of Intel’s new platform.

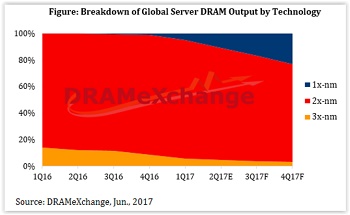

With regard to server DRAM supply, currently memory suppliers’ shipment fulfillment rates have been around 60% to 70% since the start of this year. The market therefore is still in undersupply. At the same time, procurement contracts made during this year’s first half together with the arrivals of Purley-bases servers will keep pushing up demand for server DRAM products – especially high-capacity modules – to the end of the year. On the technology front, the majority share of the server DRAM production is still done using older generations of manufacturing processes. Transitioning to 10nm-class nodes has been a major challenge for the whole industry. Server DRAM suppliers therefore have been fairly cautious in their process migration to ensure product reliability, and volume production of server DRAM using 1x-nm nodes is expected to become mainstream later in 2018.

DRAMeXchange also estimates that global server shipments in the latter half of 2017 will grow by around 10% compared with the first half of the year. In terms of shipment market shares for 2017, the top three server vendors will still be HPE, Dell and Lenovo with a combined global market share of about 40%. Huawei has the highest estimated year-on-year shipment growth for 2017 at almost 30%. Sugon and Inspur are expected to share second place for shipment growth with year-on-year grow rates of both server makers estimated at 15%.

Share on:

Testimonial

"Our marketing partnership with I-Connect007 is already delivering. Just a day after our press release went live, we received a direct inquiry about our updated products!"

Rachael Temple - AlltematedSuggested Items

LPKF Strengthens Structural Resilience: 'North Star' Initiative Aims to Secure Long-term Profitability

09/16/2025 | LPKFLPKF Laser & Electronics SE has launched the "North Star" initiative, a far-reaching package of measures designed to strengthen the company's long-term profitability.

The Marketing Minute: Cracking the Code of Technical Marketing

09/17/2025 | Brittany Martin -- Column: The Marketing MinuteMarketing is never a one-size-fits-all endeavor, but the challenges are magnified for highly technical industries like electronics. Products and processes are complex, audiences are diverse, and the stakes are high, especially when your customers are engineers, decision-makers, and global partners who depend on your expertise.

Beyond the Board: What Companies Need to Know Before Entering the MilAero PCB Market

09/16/2025 | Jesse Vaughan -- Column: Beyond the BoardThe MilAero electronics supply chain offers opportunities for manufacturers that are both prestigious and strategically important. Serving prime contractors and Tier-1 suppliers can mean long-term program stability and the satisfaction of contributing to national security. At the same time, this sector is unlike commercial electronics in almost every respect. Success requires more than technical capabilities, it requires patience, preparation, attention to detail, and a clear understanding of how the business model differs.

Global Interposer Market to Surge Nearly Fivefold by 2034

09/15/2025 | I-Connect007 Editorial TeamRevenue for the global interposer market is projected to climb from $471 million in 2025 to more than $2.3 billion by 2034, according to a new report from Business Research Insights. The growth represents a CAGR of nearly 20 percent over the forecast period.

Indium Promotes Huang to Senior Manager, Marketing Communications

08/28/2025 | Indium CorporationWith its commitment to innovation and growth through employee development, Indium Corporation announces the promotion of Jingya Huang to Senior Manager, Marketing Communications, to continue to lead the company’s branding and promotional efforts.