Trouble in Your Tank: Implementing Direct Metallization in Advanced Substrate Packaging

Trouble in Your Tank: Implementing Direct Metallization in Advanced Substrate Packaging It’s Only Common Sense: Storytelling That Sells—Stop Pitching, Start Painting Pictures

It’s Only Common Sense: Storytelling That Sells—Stop Pitching, Start Painting Pictures The Right Approach: Get Ready for ISO 9001 Version 6

The Right Approach: Get Ready for ISO 9001 Version 6

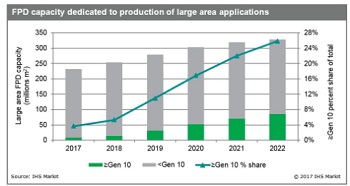

Gen 10 and Larger Flat Panel Display Capacity to Grow at 59% CAGR to 2022

December 6, 2017 | IHS MarkitEstimated reading time: 2 minutes

With BOE, China Star, LG Display and Foxconn expected to build seven new Generation 10.5 factories by 2020, Gen 10 and larger fab flat panel display (FPD) capacity is expected to grow at a compound annual growth rate of 59% between 2017 and 2022, according to IHS Markit.

“The majority of all new incremental capacity for producing FPD televisions and other large area applications will be added at Gen 10.5 in the future,” said Charles Annis, senior director at IHS Markit. “The new Gen 10.5 fabs will install 735,000 substrates per month of capacity by the end of 2022. This is enough capacity to produce more than 60 million 65-inch televisions a year.”

Gen 8 and 8.6 fabs that currently account for the bulk of large-area dedicated supply were designed to produce 55- and 58-inch panels respectively, but suffer from inefficiency at bigger sizes. Now with premium televisions rapidly moving to larger sizes as prices fall, FPD makers are racing to build Gen 10.5 factories that are highly optimized for 65- and 75-inch panels.

Gen 10.5 factories, which use enormous 2940 x 3370 mm glass substrates, require high capital outlays to construct. Based on panel makers’ public announcements, total project costs of a Gen 10.5 LCD fab with a monthly capacity of 60,000 substrates will range between $3.4 billion and $6 billion, varying by maker and process to be adopted. To help finance such expensive factories panel makers in most cases are turning to regional governments for support.

Outfitting these fabs is creating unprecedented opportunities for the supply chain that supports them, particularly for equipment makers. According to the Display Supply Demand & Equipment Tracker by IHS Markit, FPD equipment spending will reach a record high of more than $20 billion in 2018, of which new Gen 10.5 factories are a major contributing factor.

As the many new Gen 10.5 factories begin to ramp-up, IHS Markit expects 65-inch and larger panel prices will fall continuously, about 5% annually. Subsequently, demand for this high-end segment of the FPD market is forecast to expand 2.5 times to approximately 40 million units in 2022.

“Sixty-five-inch and larger panels are predicted to be one of the fastest growing segments of the FPD market over the next five years. Even so, with so many new Gen 10.5 factories being built, capacity is forecast to surge ahead of demand,” Annis said. “After 2020, smaller than Gen 10 capacity is expected to start to decline as legacy factories are shuttered. The 735,000 substrates per month of Gen 10.5 capacity in the pipeline will not only dramatically increase FPD capacity, but will also shift industry leadership towards to the four companies that are building them.”

The Display Supply Demand & Equipment Tracker by IHS Markit covers all key metrics used to evaluate supply, demand and capital spending for all major flat panel display technologies and applications.

About IHS Markit

IHS Markit is a world leader in critical information, analytics and solutions for the major industries and markets that drive economies worldwide. The company delivers next-generation information, analytics and solutions to customers in business, finance and government, improving their operational efficiency and providing deep insights that lead to well-informed, confident decisions. IHS Markit has more than 50,000 key business and government customers, including 85 percent of the Fortune Global 500 and the world’s leading financial institutions. Headquartered in London, IHS Markit is committed to sustainable, profitable growth.

Share on:

Testimonial

"We’re proud to call I-Connect007 a trusted partner. Their innovative approach and industry insight made our podcast collaboration a success by connecting us with the right audience and delivering real results."

Julia McCaffrey - NCAB GroupSuggested Items

Integrating Uniplate PLBCu6 With the Digital Factory Suite

09/12/2025 | Giovanni Obino and Andreas Schatz, MKS' AtotechPrinted circuit board manufacturing is rapidly changing, driven by miniaturization, stringent reliability requirements, and growing pressure for sustainable production. Meeting these challenges requires more than incremental improvements; it demands a combination of precise equipment and real-time process intelligence. The pairing of Uniplate® PLBCu6 with the Digital Factory Suite (DFS) demonstrates how hardware and software can work together to create more responsive, resource-efficient manufacturing.

Machvision Leads Shift to Automated Inline Final Inspection, AOI in North America

09/10/2025 | Ralph Jacobo, all4-PCBSchweitzer Engineering Laboratories (SEL) chose Machvision inspection equipment due to its capabilities and versatility. Machvision of Taiwan offers circuit inspection, hole inspection and measurement, IC Substrate and HDI inspection, and final visual inspection solutions. The best fit for SEL was the 4.0Pro Circuit Inspection for inner and outer layers, and the AFI6 for final visual inspection of finished panels.

Driving Innovation: Depth Routing Processes—Achieving Unparalleled Precision in Complex PCBs

09/08/2025 | Kurt Palmer -- Column: Driving InnovationIn PCB manufacturing, the demand for increasingly complex and miniaturized designs continually pushes the boundaries of traditional fabrication methods, including depth routing. Success in these applications demands not only on robust machinery but also sophisticated control functions. PCB manufacturers rely on advanced machine features and process methodologies to meet their precise depth routing goals. Here, I’ll explore some crucial functions that empower manufacturers to master complex depth routing challenges.

Securing the Future: The Battle for America's Flat Panel Display Industry

08/12/2025 | Marcy LaRont, I-Connect007The production and sourcing of flat panel displays have become a focal point of concern, particularly regarding national security. In this interview, Jim Will, executive director of the U.S. Partnership for Assured Electronics (USPAE), provides insights into the essential role of liquid crystal displays (LCDs) in both defense systems and everyday technology. Their conversation delves into the implications of America's dependence on Chinese manufacturers for these critical components, raising alarms about supply chain vulnerabilities amidst rising geopolitical tensions.

Omdia Forecasts Large-Area Display Shipments to Grow 2.9% YoY in 2025 Despite Economic Uncertainty

07/21/2025 | BUSINESS WIREAccording to the latest analysis from Omdia’s Large-area display market tracker – 2Q25 with 1Q25 results, large-area display (above 9-inch) unit shipments are forecast to increase by 2.9% year-over-year (YoY) in 2025.