Trouble in Your Tank: Implementing Direct Metallization in Advanced Substrate Packaging

Trouble in Your Tank: Implementing Direct Metallization in Advanced Substrate Packaging It’s Only Common Sense: Storytelling That Sells—Stop Pitching, Start Painting Pictures

It’s Only Common Sense: Storytelling That Sells—Stop Pitching, Start Painting Pictures The Right Approach: Get Ready for ISO 9001 Version 6

The Right Approach: Get Ready for ISO 9001 Version 6

LG Display Retains Its Lead in Area Shipments of Large Displays in 1Q18

May 15, 2018 | IHS MarkitEstimated reading time: 2 minutes

Despite the low seasonality factor and brands turning their focus away from volume growth, the demand for large display panels showed better-than-expected results in the first quarter of 2018, albeit still weak, according to IHS Markit.

First quarter of each year is typically a slow season for the display market as set brands try to clear out carried inventories before they launch new models in a new year. In addition, particularly this year, top-tier brands were expected to stop focusing on volume growth, which lowered market expectation on the panel demand.

However, shipments of large display panels posted better-than-expected results in the first quarter of 2018, according to Large Area Display Market Tracker by IHS Markit. Compared to a year ago, shipments of large displays -- larger than 9 inches -- increased by 6% in unit and by 10% in area.

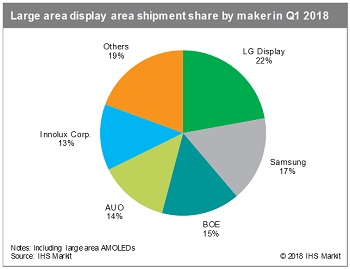

LG Display retained its lead in the large display panel market in terms of area shipments with a stake of 22%, followed by Samsung Display with 17%, while, in terms of unit shipments, BOE led the market with a 22% share.

“In area shipments, South Korean panel makers keep their leading position in the large display market as they are strong in the TV display market,” said Robin Wu, principal analyst at IHS Markit.

Shipments of TV displays increased by 12% in unit and by 11% in area in the first quarter of 2018 compared to a year ago, leading to the better-than-expected trend. In particular, unit shipments of 55-inch and larger TV panels jumped 20% year on year in the first quarter. 4K TV display unit shipment also increased by 19% during the same period to 24.6 million units, and OLED TV display shipments reached some 600,000 units with 110% year-on-year growth.

“Increases in large display panel production capacity, particularly in China, helped the year-on-year shipment growth, which was somewhat expected,” Wu said. “But, if you look at the shipment growth in a quarter-on-quarter term, it is quite interesting.”

For the past three years from 2015 to 2017, on average, unit shipments of large display declined 10% in the first quarters compared to the previous quarter, and area shipments were down 8%.

This year also shows declines in the first quarter with a 4% drop in unit shipments and 7% down in area shipments, but the contraction is narrower than the previous years,” Wu said. “This indicates the shipment trend in first quarter 2018 was better than expected.”

Wu noted, however, that shipments dropped 10% in value due to continued erosion in panel price, which began in mid- 2017.

“The major concerns to the panel makers is how to achieve a turnaround in panel prices and when,” Wu said. “Trends in TV display panels that are shifting to larger sizes and heading to higher-end products can be the key to overcome the challenge.”Wu noted, however, that shipments dropped 10% in value due to continued erosion in panel price, which began in mid- 2017.

The Large Area Display Market Tracker by IHS Markit provides information about the entire range of large display panels shipped worldwide and regionally, including monthly and quarterly revenues and shipments by display area, application, size and aspect ratio for each supplier.

About IHS Markit

IHS Markit is a world leader in critical information, analytics and solutions for the major industries and markets that drive economies worldwide. The company delivers next-generation information, analytics and solutions to customers in business, finance and government, improving their operational efficiency and providing deep insights that lead to well-informed, confident decisions. IHS Markit has more than 50,000 business and government customers, including 80% of the Fortune Global 500 and the world’s leading financial institutions.

Share on:

Testimonial

"We’re proud to call I-Connect007 a trusted partner. Their innovative approach and industry insight made our podcast collaboration a success by connecting us with the right audience and delivering real results."

Julia McCaffrey - NCAB GroupSuggested Items

Global Interposer Market to Surge Nearly Fivefold by 2034

09/15/2025 | I-Connect007 Editorial TeamRevenue for the global interposer market is projected to climb from $471 million in 2025 to more than $2.3 billion by 2034, according to a new report from Business Research Insights. The growth represents a CAGR of nearly 20 percent over the forecast period.

Indium Promotes Huang to Senior Manager, Marketing Communications

08/28/2025 | Indium CorporationWith its commitment to innovation and growth through employee development, Indium Corporation announces the promotion of Jingya Huang to Senior Manager, Marketing Communications, to continue to lead the company’s branding and promotional efforts.

India’s PC Market Grows 5.7% YoY in 1H25, Shipping 6.8 Million Units

08/22/2025 | IDCIndia’s traditional PC market (desktops, notebooks, and workstations) grew 3.0% year-over-year (YoY) in 2Q25 with 3.5 million units shipments, according to data from the International Data Corporation (IDC) Worldwide Quarterly Personal Computing Device Tracker. This marks the eighth consecutive quarter of growth.

Ta Yang Group Holdings Limited Announcing AI Transformation Blueprint

08/21/2025 | ACN NewswireTa Yang Group Holdings Limited, a well-established Hong Kong-listed company with nearly two decades of market presence, plans to further advance comprehensively into the Web 4.0 field and artificial intelligence (AI) industry.

Standardized Hinges and Apple’s Entry Expected to Push Foldable Phone Penetration Beyond 3% by 2027

08/19/2025 | TrendForceTrendForce’s latest investigations reveal that the anticipated launch of Apple’s first foldable device in the second half of 2026 is expected to lift foldable phone penetration from 1.6% in 2025 to over 3% in 2027.