American Made Advocacy: Success in Washington Requires Patience, Persistence, and Sustained Focus

American Made Advocacy: Success in Washington Requires Patience, Persistence, and Sustained Focus The Government Circuit: News on Defense Electronics, Europe, and Sustainability

The Government Circuit: News on Defense Electronics, Europe, and Sustainability Defense Speak Interpreted: SWaPing Nanosatellites for Defense Systems

Defense Speak Interpreted: SWaPing Nanosatellites for Defense Systems

DRAM Suppliers Must Carefully Plan Capacity to Maintain Profitability Amid Rising Bit Output in 2025

November 6, 2024 | TrendForceEstimated reading time: 1 minute

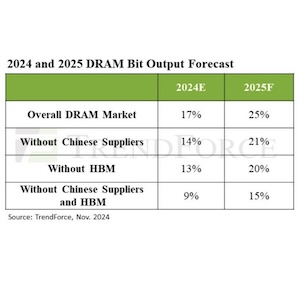

The DRAM industry experienced inventory reductions and price recovery in the first three quarters of 2024; however, pricing momentum is expected to weaken in the fourth quarter. TrendForce’s Senior Vice President of Research, Avril Wu, noted that some DRAM suppliers, after achieving profitability this year, have begun planning new capacity expansions. This could lead to a 25% YoY increase in total DRAM bit output in 2025—marking a more substantial growth compared to 2024.

TrendForce’s latest investigations reveal that the DRAM market structure is becoming increasingly complex. In addition to traditional categories such as PC, server, mobile, graphics, and consumer DRAM, HBM has been added to the product mix. Geopolitically, China’s rapid capacity expansion in recent years is expected to impact the global supply landscape. Wu indicated that among the three major DRAM manufacturers, SK hynix will have the largest capacity expansion in 2025, driven significantly by its highly profitable HBM products.

Overall, TrendForce projects a 25% increase in DRAM bit output industry-wide in 2025, or 21% when excluding Chinese suppliers. Notably, most of the output from Chinese companies primarily serves domestic customers, with minimal supply directed to overseas markets.

HBM has emerged as a critical growth engine for the DRAM industry thanks to burgeoning AI demand. Excluding HBM, conventional DRAM bit output is expected to increase by 20% in 2025. When further excluding HBM and supply from Chinese companies, the bit output from the three major DRAM manufacturers is forecast to grow by only 15%—a relatively low level compared to historical trends. Conventional DRAM includes products like DDR5, DDR4, LPDDR4/5, as well as graphics and consumer DRAM.

TrendForce warns that with an abundant supply of DRAM bits projected in 2025, any underperformance in demand could place downward pressure on prices. From a geopolitical perspective, China’s DRAM supply achievement rate is expected to surpass other regions, focusing primarily on older-process LPDDR4x and DDR4, which will face higher pricing pressure compared to other DRAM types. Additionally, the HBM supply—particularly HBM3e—is anticipated to remain tight throughout next year.

Share on:

Suggested Items

WiSA Technologies Inks Definitive Agreement to Acquire CompuSystems

12/27/2024 | BUSINESS WIREWiSA Technologies, Inc., which anticipates closing its acquisition of Datavault® intellectual property and information technology assets of privately held Data Vault Holdings Inc.® and changing its name to Datavault Inc.

'Qualcomm AI Program for Innovators' Launched to Foster On-Device AI Innovation in the Asia-Pacific Region

12/27/2024 | Qualcomm Technologies, Inc.Qualcomm Technologies, Inc. announced the launch of the Qualcomm AI Program for Innovators (QAIPI) 2025 - APAC, a new initiative aimed at supporting professional developers and startups from Japan, Singapore, and South Korea to create cutting-edge on-device AI solutions across diverse sectors.

Wistron Announces Strategic Investments

12/27/2024 | WistronWistron Corporation announced several strategic investments to support its ongoing business growth and development.

Indian IT Services Market Grows 6.4% in 1H2024 Driven by AI and Digital Transformation

12/27/2024 | IDCAccording to the International Data Corporation (IDC) Worldwide Semi-annual Services Tracker, the Indian IT Services market grew by 6.4% year-over-year (YoY) in 1H2024, contributing 79.2% of the overall IT & Business Services market.

Kimball Electronics Thailand Namlee School

12/26/2024 | Kimball ElectronicsKimball Electronics Thailand (KETL) has continued its commitment to supporting education and community development in Thailand.