Dan’s Biz Bookshelf: Four Important Books You Need to Read (Not Just Say You Have)

Dan’s Biz Bookshelf: Four Important Books You Need to Read (Not Just Say You Have) The Marketing Minute: Cracking the Code of Technical Marketing

The Marketing Minute: Cracking the Code of Technical Marketing

LCD Panel Market Experienced a Much More Moderate Oversupply

June 28, 2016 | TrendForceEstimated reading time: 2 minutes

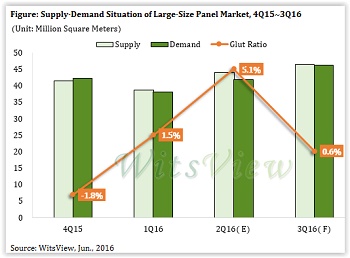

The first quarter conventionally is when the LCD panel market has abundant supply. However, the February earthquake in southern Taiwan and Samsung Display (SDC) having problems with transitioning to a new manufacturing process resulted in some loss of the panel industry’s overall capacity during the period. Furthermore, panel makers gained confidence in the market as the efforts to consume excess TV panel inventories were more efficient than anticipated. In sum, the panel market in the first quarter experienced a much more moderate oversupply situation.

With regard to the second quarter, WitsView, a division of TrendForce finds that the six major panel makers have ramped up their production as effects of the earthquake in Taiwan and SDC’s manufacturing issues subsided. The bottoming out of the panel prices has also spurred the panel makers to step up their production. According to WitsView’s latest report on panel capacity, the large-size panel’s glut ratio (an index used to measure market oversupply) in the second quarter has risen to 5.5%, a significant increase from the first quarter’s 1.5%.

According to WitsView, Innolux and SDC have made an all-out effort to boost their panel production in the current quarter to compensate for the capacity losses they experienced in the prior period. At the same time, LG Display (LGD), AU Optronics (AUO), BOE Technology (BOE) and China Star Optoelectronics (CSOT) have all expanded their respective Gen-8.5 capacities, further increasing the panel supply. From the demand side, branded vendors working in various application markets have begun stocking up ahead of the peak season in the third quarter. Panel prices therefore have also started to stabilize, and some size segments are even seeing signs of rebound. Panel inventories have gradually returned to a healthy level during this period after the entire supply chain underwent an adjustment in the first quarter. As panel makers become more reluctant to produce unprofitable products, supply for some size segments have tightened and prices have rallied.

WitsView’s analysis for the coming third quarter indicates that the industry’s capacity expansion will be limited and the market will benefit from the effects of the peak season. The large-size panel’s glut ratio for the period is forecast to drop sharply to 0.6%. The market on the whole will reach an equilibrium and may even shift a bit towards undersupply. Prices for some size segments may continue to recover for two straight quarters. This unusual trend is attributed to market concerns about these size segments facing constraints in yield rates and panel makers allocating capacities away from them to make other products. On the whole, TV panels such as those sized 55 inches and 43 inches and under plus monitor panels sized 23 inches and under are expected to experience price rebound in the third quarter.

Share on:

Testimonial

"We’re proud to call I-Connect007 a trusted partner. Their innovative approach and industry insight made our podcast collaboration a success by connecting us with the right audience and delivering real results."

Julia McCaffrey - NCAB GroupSuggested Items

LPKF Strengthens Structural Resilience: 'North Star' Initiative Aims to Secure Long-term Profitability

09/16/2025 | LPKFLPKF Laser & Electronics SE has launched the "North Star" initiative, a far-reaching package of measures designed to strengthen the company's long-term profitability.

The Marketing Minute: Cracking the Code of Technical Marketing

09/17/2025 | Brittany Martin -- Column: The Marketing MinuteMarketing is never a one-size-fits-all endeavor, but the challenges are magnified for highly technical industries like electronics. Products and processes are complex, audiences are diverse, and the stakes are high, especially when your customers are engineers, decision-makers, and global partners who depend on your expertise.

Beyond the Board: What Companies Need to Know Before Entering the MilAero PCB Market

09/16/2025 | Jesse Vaughan -- Column: Beyond the BoardThe MilAero electronics supply chain offers opportunities for manufacturers that are both prestigious and strategically important. Serving prime contractors and Tier-1 suppliers can mean long-term program stability and the satisfaction of contributing to national security. At the same time, this sector is unlike commercial electronics in almost every respect. Success requires more than technical capabilities, it requires patience, preparation, attention to detail, and a clear understanding of how the business model differs.

Global Interposer Market to Surge Nearly Fivefold by 2034

09/15/2025 | I-Connect007 Editorial TeamRevenue for the global interposer market is projected to climb from $471 million in 2025 to more than $2.3 billion by 2034, according to a new report from Business Research Insights. The growth represents a CAGR of nearly 20 percent over the forecast period.

Indium Promotes Huang to Senior Manager, Marketing Communications

08/28/2025 | Indium CorporationWith its commitment to innovation and growth through employee development, Indium Corporation announces the promotion of Jingya Huang to Senior Manager, Marketing Communications, to continue to lead the company’s branding and promotional efforts.