Dan’s Biz Bookshelf: Four Important Books You Need to Read (Not Just Say You Have)

Dan’s Biz Bookshelf: Four Important Books You Need to Read (Not Just Say You Have) The Marketing Minute: Cracking the Code of Technical Marketing

The Marketing Minute: Cracking the Code of Technical Marketing

Semiconductor Sensor Sales Keep Hitting New Records Amid Price Erosion

July 22, 2016 | IC InsightsEstimated reading time: 2 minutes

Despite strong double-digit percentage increases in annual unit shipments, semiconductor sensor sales growth has become uncharacteristically lethargic because of steep price erosion in several major product categories. Strong unit demand is being fueled by new wearable systems, greater automation in vehicles, and the much-anticipated Internet of Things (IoT), but sharply falling average selling prices (ASPs) on accelerometers, gyroscope chips, and magnetic-field measuring devices are capping annual growth of total sensor revenues in the low- to mid-single digit range, based on data in IC Insights’ 2016 O-S-D Report—A Market Analysis and Forecast for Optoelectronics, Sensors/Actuators, and Discretes.

The 2016 O-S-D Report shows worldwide dollar-volume revenues for sensors rising by a compound annual growth rate (CAGR) of 5.3% between 2015 and 2020 compared to an 8.9% annual rate in the last five years. In contrast, total sensor unit shipments are expected to climb by a CAGR of 12.4% in the five-year forecast period compared to a blistering 20.5% rate of increase in the 2010-2015 period, when new sensing, navigation, and automated embedded control functions in smartphones drove up strong growth along with steady increases in automotive and industrial applications.

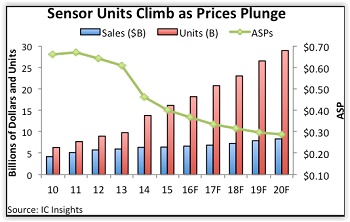

Despite recent years of weak sales growth—just 1% in 2015 to $6.4 billion—the sensor market is expected to end this decade with 10 consecutive years of record-high revenues and reach $8.3 billion in 2020 (Figure 1). Unit shipments of sensors have reached record high levels each year since the beginning of the last decade—even in the 2009 downturn year, when worldwide unit volume grew 9% while sensor revenues dropped 3%. Record sensor shipments are expected to continue for another five years, reaching 28.9 billion units in 2020, according to the 360-page 2016 O-S-D Report, which contains a detailed five-year forecast of sales, unit volume, and ASPs for more than 30 individual product types and device categories in optoelectronics, sensors/actuators, and discretes.

Competition between suppliers and requirements for low-cost sensors in new high-volume applications drove down ASPs from about $0.66 in 2010 to $0.40 in 2015. The need to squeeze more sensing solutions into wearable systems, far-flung IoT-connected applications, and multi-sensor packages for increased accuracy and multi-dimensional measurements is exerting more pricing pressure in the market, concludes the 2016 O-S-D Report. The report’s forecast shows sensor ASPs dropping by a CAGR of 6.3% in the next five years to only $0.29.

Total sensor sales are expected to grow by about 3% in 2016 to $6.6 billion with worldwide shipments rising 13% to nearly 18.2 billion units this year. Sales of sensors made with microelectromechanical systems (MEMS) technology (i.e., accelerometers, gyroscope devices, and pressure sensors, including microphone chips)—are expected to grow by 4% in 2016 to $4.8 billion with unit shipments increasing 10% to 7.6 billion. The 2016 O-S-D Report projects MEMS-based sensor sales rising by a CAGR of 5.5% in the next five years to $6.1 billion in 2020 with unit shipments growing by an annual rate of 11.9% to nearly 13.4 billion. ASPs for MEMS-based sensors are expected to decline by a CAGR of -5.7% to $0.45 in 2020 from $0.61 in 2015, according to the annual O-S-D Report.

Share on:

Testimonial

"Advertising in PCB007 Magazine has been a great way to showcase our bare board testers to the right audience. The I-Connect007 team makes the process smooth and professional. We’re proud to be featured in such a trusted publication."

Klaus Koziol - atgSuggested Items

It’s Only Common Sense: Storytelling That Sells—Stop Pitching, Start Painting Pictures

09/15/2025 | Dan Beaulieu -- Column: It's Only Common SenseLet me tell you something that most salespeople — even the ones flashing Rolexes and bragging about crushing their quotas—still haven’t figured out: Facts don’t close deals, stories do. People file away facts while they feel stories. Facts tickle the brain, but stories punch the heart, and it’s the heart that signs the check every time.

It's Only Common Sense: Leveraging AI in Your Sales Strategy

09/01/2025 | Dan Beaulieu -- Column: It's Only Common SenseLet’s get one thing straight: AI isn’t here to replace you; it’s here to make you smarter and faster. Every time a new tool shows up, half the sales floor panics: “They’re going to automate us out of a job!” This is shouted while doomscrolling LinkedIn. Relax. Sales is still, and will always be, about human connection, trust, and delivering value. However, if you’re not using AI to your advantage, you’re handing your competitors a loaded gun and asking them to shoot first.

Lessons From a Thousand Columns: Dan Beaulieu on Writing, Selling, and Staying the Course

08/21/2025 | Michelle Te, I-Connect007For 20 years, Dan Beaulieu has been a steady voice in sales and marketing, offering weekly columns that challenge, inspire, and guide professionals in the electronics industry and beyond. Soon, he will reach a remarkable milestone—his 1,000th It’s Only Common Sense weekly column. In this Q&A, we look behind the scenes of Dan’s writing journey, exploring what has kept him motivated, the lessons he’s learned along the way, and how two decades of weekly columns have shaped his career and the industry conversation.

COVID, Tough Sales, and What Made Me a Better Salesperson

08/12/2025 | Daniel Beauvois, The Component StoreBefore 2020, we approached sales differently. A persistent, gritty salesperson could approach businesses daily without an appointment. They would often be turned away, but sometimes, they would be given a shot. Then, in March 2020, the COVID-19 pandemic became official, and things started to shut down. When we finally came back, everything had changed, creating an impenetrable barrier for outside salespeople.

Indium Corporation Promotes Two Leaders in EMEA (Europe, Middle East, and Africa) Markets

08/05/2025 | Indium CorporationWith its commitment to innovation and growth through employee development, Indium Corporation today announced the promotions of Andy Seager to Associate Director, Continental Sales (EMEA), and Karthik Vijay to Senior Technical Manager (EMEA). These advancements reflect their contributions to the company’s continued innovative efforts with customers across Europe, the Middle East, and Africa (EMEA).