Dan’s Biz Bookshelf: Four Important Books You Need to Read (Not Just Say You Have)

Dan’s Biz Bookshelf: Four Important Books You Need to Read (Not Just Say You Have) The Marketing Minute: Cracking the Code of Technical Marketing

The Marketing Minute: Cracking the Code of Technical Marketing

Basic Wearables Soar and Smart Wearables Stall as Worldwide Wearables Market Climbs 26.1% in Q2

September 6, 2016 | IDCEstimated reading time: 2 minutes

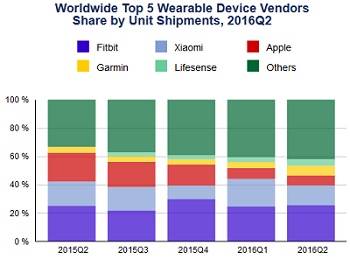

Shipments of wearable devices reached 22.5 million in the second quarter of 2016 (2Q16) according to the International Data Corporation (IDC) Worldwide Quarterly Wearable Device Tracker. Despite a decline in shipments for one of the largest vendors, the overall market for wearable devices grew 26.1% year over year as new use cases are slowly starting to emerge.

"Fitness is the low-hanging fruit for wearables," said Jitesh Ubrani, senior research analyst for IDC Mobile Device Trackers. "However, the market is evolving and we're starting to see consumers adopt new functionality, such as communication and mobile payments, while enterprises warm to wearables' productivity potential."

While the overall wearables market grew during 2Q16, its two categories traveled at different speeds and directions. Basic wearables (devices that do not support third party applications) grew 48.8% from 2Q15 levels while smart wearables (devices that support third party applications) declined 27.2% year over year.

"Basic wearables, which include most fitness trackers, have benefited from a combination of factors: a clear value proposition for end-users, an abundant selection of devices from multiple vendors, and affordable price points," said Ramon Llamas, research manager, Wearables. "Consequently, basic wearables accounted for 82.8% of all wearable devices shipped during the quarter, and more vendors continue to enter this space. The danger, however, is that most devices end up being copycats of others, making it increasingly difficult to differentiate themselves in a crowded market.

"Smart wearables, meanwhile, are still struggling to find their place in the market," added Llamas. "There is plenty of curiosity about what smart wearables – particularly smartwatches – can do, but they have yet to convince users that they are a must-have item. The good news is that smart wearables are still in their initial stages and vendors are slowly making strides to improve them. But this also means that it will be a slow transition from basic wearables to smart wearables."

Vendor Highlights:

Fitbit's dominance remains unchallenged for now as the company's name is synonymous with fitness bands. The latest Charge 2 and Flex 2 are indicative that the company is growing up, giving form and function equal importance. Fitbit's recent accquistition in the mobile payments arena should also help ensure success in the longer term.

Xiaomi Mi Bands remain extremely popular in China. In every technology market, Xiaomi has focused on the value conscious consumers, and that trend continues. The recent launch of the Mi Band 2 includes heart rate tracking and still maintains a price below $20 USD. The challenge for Xiaomi, however, is growing beyond China's borders and onto the global stage.

Apple was the only vendor among the market leaders to post a year-over-year decrease in shipment volumes, primarily because it did not launch a new model on the anniversary of its first generation Watch. 2Q16 was the first full quarter of Apple's reduced price strategy on the Sport model, which slightly helped the company rebound from its post-holiday slump.

Garmin's vertical integration and constant expansion of the ConnectIQ app store have allowed the company to slowly expand its channel presence and gain consumer mindshare. While it remains focused on fitness enthusiasts and athletes, the latest design of the Fenix Chronos will certainly help broaden its appeal to the masses.

This is the first time Lifesense has broken into the top five on the strength of by its low-cost Mambo fitness trackers shipping into China. It also connects with WeChat, an immensely popular messaging service in China, to share data with others without having to log into a separate application.

Share on:

Testimonial

"Advertising in PCB007 Magazine has been a great way to showcase our bare board testers to the right audience. The I-Connect007 team makes the process smooth and professional. We’re proud to be featured in such a trusted publication."

Klaus Koziol - atgSuggested Items

LPKF Strengthens Structural Resilience: 'North Star' Initiative Aims to Secure Long-term Profitability

09/16/2025 | LPKFLPKF Laser & Electronics SE has launched the "North Star" initiative, a far-reaching package of measures designed to strengthen the company's long-term profitability.

The Marketing Minute: Cracking the Code of Technical Marketing

09/17/2025 | Brittany Martin -- Column: The Marketing MinuteMarketing is never a one-size-fits-all endeavor, but the challenges are magnified for highly technical industries like electronics. Products and processes are complex, audiences are diverse, and the stakes are high, especially when your customers are engineers, decision-makers, and global partners who depend on your expertise.

Beyond the Board: What Companies Need to Know Before Entering the MilAero PCB Market

09/16/2025 | Jesse Vaughan -- Column: Beyond the BoardThe MilAero electronics supply chain offers opportunities for manufacturers that are both prestigious and strategically important. Serving prime contractors and Tier-1 suppliers can mean long-term program stability and the satisfaction of contributing to national security. At the same time, this sector is unlike commercial electronics in almost every respect. Success requires more than technical capabilities, it requires patience, preparation, attention to detail, and a clear understanding of how the business model differs.

Global Interposer Market to Surge Nearly Fivefold by 2034

09/15/2025 | I-Connect007 Editorial TeamRevenue for the global interposer market is projected to climb from $471 million in 2025 to more than $2.3 billion by 2034, according to a new report from Business Research Insights. The growth represents a CAGR of nearly 20 percent over the forecast period.

Indium Promotes Huang to Senior Manager, Marketing Communications

08/28/2025 | Indium CorporationWith its commitment to innovation and growth through employee development, Indium Corporation announces the promotion of Jingya Huang to Senior Manager, Marketing Communications, to continue to lead the company’s branding and promotional efforts.