It’s Only Common Sense: Hire for Hunger, Train for Skill

It’s Only Common Sense: Hire for Hunger, Train for Skill Dan’s Biz Bookshelf: ‘The 'NVIDIA Way: Jensen Huang and the Making of a Tech Giant’

Dan’s Biz Bookshelf: ‘The 'NVIDIA Way: Jensen Huang and the Making of a Tech Giant’

Domestic Supply Chain Shuffle: Increasing the Value of Local Content in Semiconductor Equipment

November 6, 2017 | SEMIEstimated reading time: 2 minutes

“Quality first, cost second.” This was the clear “take home” message for Chinese materials, subsystems and components suppliers attending an invitational event organised by ICMTIA in Ningbo on October 23. In the first meeting of its kind, almost 300 delegates from across the Chinese semiconductor equipment supply chain gathered to discuss the challenges and opportunities for Chinese suppliers to become innovators and leaders in global semiconductor manufacturing.

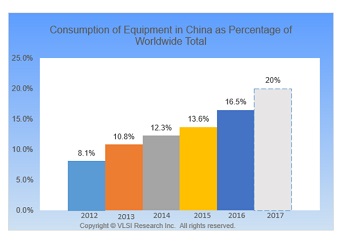

Over 20% of all semiconductor equipment will be shipped to China in 2017, yet Chinese OEMs account for only 2% of worldwide fab equipment. This percentage is even lower for Chinese subsystems and components suppliers. At the current rate of growth, China is soon expected to eclipse even Taiwan and Korea as the largest regional consumer of semiconductor equipment. The gap between Chinese equipment consumption and the value of locally supplied parts will continue to increase unless something changes.

Rapid growth in Chinese equipment consumption is set to continue, however, only a very small amount of equipment worldwide is actually supplied by Chinese OEMs.

The disparity between equipment consumption and production presents a clear opportunity for Chinese suppliers to increase their share of market within China. The question “Does it make sense to go head-to-head against the large U.S., European, and Japanese players or to take a softer approach by encouraging foreign suppliers to source more of their subcomponents and assembly services from Chinese suppliers?” The softer approach appears to be gaining favour as it carries lower risk of failure and allows Chinese suppliers to learn the quality processes required to develop advanced technology products and improve workforce skills and talent needed to compete at the cutting-edge of semiconductor chip manufacturing.

Foreign subsystems and components suppliers such as Advanced Energy, MKS and others have been manufacturing their products in China for many years proving that the infrastructure already exists to make high-quality subsystems. Foreign OEMS are now following their lead by actively seeking Chinese subcontract partners. Applied Materials is spearheading this move by making large investments and developing programs to help Chinese suppliers qualify. As a consequence, Chinese subcontract manufacturers are already learning and quickly developing their own IP

A significant portion of total global subsystems and components are manufactured in China demonstrating that it is already possible to manufacture high-quality products for semiconductor manufacturing in China.

In the short term, however, it is unlikely that a large Chinese OEM or subsystems supplier could rival the well-established incumbents – even with generous governmental policy and support. The significant barriers to entry are still present, including: large R&D costs; finding and retaining talented industry professionals and most importantly building the long-term trust and reputation with chip makers to displace the established equipment suppliers.

Nevertheless, with the backing of the Chinese government, semiconductor subsystems and component manufacturing in China is set to make a step change in strategy moving forwards. A major focus on improving quality and collaboration across the Chinese supply chain will both improve the reputation of Chinese suppliers and facilitate the development of innovative IP within China. Full domestication of the supply chain will in turn force foreign companies to increase the Chinese content of their equipment made in China. It is clear that China is organising to become one of the leading players of semiconductor manufacturing technology – the only question is “when,” not “if.”

Share on:

Testimonial

"In a year when every marketing dollar mattered, I chose to keep I-Connect007 in our 2025 plan. Their commitment to high-quality, insightful content aligns with Koh Young’s values and helps readers navigate a changing industry. "

Brent Fischthal - Koh YoungSuggested Items

MEIKO Electronics Expands ASEAN Footprint with New Vietnam Subsidiary to Support Growing Demand

04/16/2026 | MeikoMEIKO ELECTRONICS CO., LTD. has announced that, at its Board of Directors meeting held on April 8, 2026, the company resolved to establish a wholly owned subsidiary, MEIKO ELECTRONICS YEN QUANG CO., LTD. (MKYQ), in Phu Tho Province, Vietnam.

Alpha and Omega Semiconductor Begins IPM5 Production at Kaynes Semicon Launch in Gujarat

04/16/2026 | Alpha and Omega Semiconductor LimitedAlpha and Omega Semiconductor Limited, a designer, developer, and global supplier of a broad range of discrete power devices, wide bandgap power devices, power management ICs, and modules, marks a historic expansion of its global manufacturing footprint with the official inauguration of Kaynes Semicon’s state-of-the-art OSAT facility in Sanand, Gujarat.

Podcast Hits the Mark in a Materials Market

04/15/2026 | Marcy LaRont, I-Connect007The base material of a printed circuit board is its literal and functional foundation. Isola, founded in 1912 in Düren, Germany, is one of the longest-standing manufacturers of glass-reinforced laminates in the electronics industry. Originally focused on insulation and fiberglass materials, the company played an early role in supplying the foundational substrates that enabled the growth of PCB technology. As electronics advanced, Isola evolved alongside the industry, expanding from basic glass-epoxy laminates into high-performance copper-clad materials and engineered prepregs.

Inside Eastek Malaysia: Scalable Manufacturing Built on Trust, Stability, and Technical Expertise

04/14/2026 | Eastek International CorporationEastek International Corporation continues to strengthen its global manufacturing platform through the sustained performance and expanding capabilities of its Malaysia operation.

SMTA Ultra HDI Symposium, Day 1: AI at the Core or Out of the Game

04/13/2026 | Marcy LaRont, I-Connect007It was a beautiful 81°F morning in Arizona last Wednesday as I headed to the third annual SMTA Ultra HDI Symposium, focused on AI and ultra high density interconnect technology. Strategically held as part of Arizona’s Tech Week, this year’s conference took place in Avondale in Phoenix's West Valley. The event moved from the cozy offices of the Peoria Sports Complex (which paid homage to baseball’s spring training world) to the larger Avondale Conference Center, highlighting the importance of this area for electronics manufacturing investment.