The New Chapter: Navigating Maternity Leave in the Electronics Industry

The New Chapter: Navigating Maternity Leave in the Electronics Industry American Made Advocacy: There's No Substitute for American-made Microelectronics

American Made Advocacy: There's No Substitute for American-made Microelectronics It’s Only Common Sense: When Will Big Companies Start Paying Their Bills on Time?

It’s Only Common Sense: When Will Big Companies Start Paying Their Bills on Time?

DRAM Suppliers Must Carefully Plan Capacity to Maintain Profitability Amid Rising Bit Output in 2025

November 6, 2024 | TrendForceEstimated reading time: 1 minute

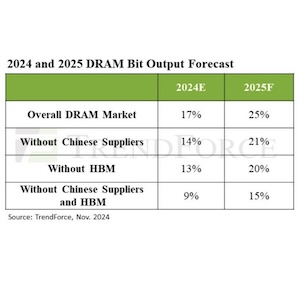

The DRAM industry experienced inventory reductions and price recovery in the first three quarters of 2024; however, pricing momentum is expected to weaken in the fourth quarter. TrendForce’s Senior Vice President of Research, Avril Wu, noted that some DRAM suppliers, after achieving profitability this year, have begun planning new capacity expansions. This could lead to a 25% YoY increase in total DRAM bit output in 2025—marking a more substantial growth compared to 2024.

TrendForce’s latest investigations reveal that the DRAM market structure is becoming increasingly complex. In addition to traditional categories such as PC, server, mobile, graphics, and consumer DRAM, HBM has been added to the product mix. Geopolitically, China’s rapid capacity expansion in recent years is expected to impact the global supply landscape. Wu indicated that among the three major DRAM manufacturers, SK hynix will have the largest capacity expansion in 2025, driven significantly by its highly profitable HBM products.

Overall, TrendForce projects a 25% increase in DRAM bit output industry-wide in 2025, or 21% when excluding Chinese suppliers. Notably, most of the output from Chinese companies primarily serves domestic customers, with minimal supply directed to overseas markets.

HBM has emerged as a critical growth engine for the DRAM industry thanks to burgeoning AI demand. Excluding HBM, conventional DRAM bit output is expected to increase by 20% in 2025. When further excluding HBM and supply from Chinese companies, the bit output from the three major DRAM manufacturers is forecast to grow by only 15%—a relatively low level compared to historical trends. Conventional DRAM includes products like DDR5, DDR4, LPDDR4/5, as well as graphics and consumer DRAM.

TrendForce warns that with an abundant supply of DRAM bits projected in 2025, any underperformance in demand could place downward pressure on prices. From a geopolitical perspective, China’s DRAM supply achievement rate is expected to surpass other regions, focusing primarily on older-process LPDDR4x and DDR4, which will face higher pricing pressure compared to other DRAM types. Additionally, the HBM supply—particularly HBM3e—is anticipated to remain tight throughout next year.

Share on:

Suggested Items

Sanmina Reports Q4 and Fiscal 2024 Financial Results

11/06/2024 | SanminaSanmina Corporation, a leading integrated manufacturing solutions company, reported financial results for the fourth quarter and fiscal year ended September 28, 2024 and outlook for its fiscal first quarter ending December 28, 2024.

Fabrinet Announces Q1 Fiscal Year 2025 Financial Results

11/06/2024 | FabrinetFabrinet, a leading provider of advanced optical packaging and precision optical, electro-mechanical and electronic manufacturing services to original equipment manufacturers of complex products, announced its financial results for its fiscal first quarter ended September 27, 2024.

iNEMI End-of-Project Webinar: Investigation of AI Enhancement to AOI for PCBA

11/06/2024 | iNEMIAutomated optical inspection (AOI) systems are essential in electronic manufacturing for ensuring the quality of printed circuit board assemblies (PCBAs).

Schweizer Electronic Lowers 2024 Financial Forecast Amid Challenging Market Conditions

11/06/2024 | Schweizer Electronic AGBased on the preliminary financial results for the first nine months of 2024 of the SCHWEIZER Group, the Executive Board has adjusted the forecast for the 2024 financial year.

Global Semiconductor Sales Increase 23.2% in Q3 2024 YoY; QoQ Sales Up 10.7%

11/06/2024 | SIAThe Semiconductor Industry Association (SIA) today announced global semiconductor sales were $166.0 billion for the third quarter of 2024, an increase of 23.2% compared to the third quarter of 2023 and 10.7% more than the second quarter of 2024.