It’s Only Common Sense: The Phone Is Still Mightier Than the Keyboard

It’s Only Common Sense: The Phone Is Still Mightier Than the Keyboard The Marketing Minute: Marketing With Layers

The Marketing Minute: Marketing With Layers

Chinese Services Activity Rises Solidly, But Manufacturing Sector Loses Momentum

October 8, 2018 | IHS MarkitEstimated reading time: 6 minutes

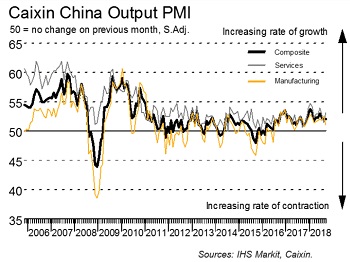

The latest Caixin China Composite PMI data (which covers both manufacturing and services) showed that Chinese business activity expanded modestly at the end of the third quarter. At 52.1 in September, the Composite Output Index was little-changed from August’s reading of 52.0, to signal that the rate of activity growth remained lacklustre compared to that seen earlier in 2018.

Analysis

Latest data indicated that an improved service sector performance was broadly offset by softer manufacturing growth. Notably, the seasonally adjusted Caixin China General Services Business Activity Index picked up from 51.5 in August to 53.1, to signal the strongest increase in activity for three months. In contrast, manufacturing production rose at a marginal pace that was the weakest since October 2017.

New business followed a similar trend, with services companies registering a stronger rise in new orders. Though modest, the latest increase in service sector sales was the quickest recorded since June, with some firms linking growth to new product offerings and increased client bases. Meanwhile, new business broadly stagnated at manufacturing companies after a marginal rise in August. As a result, composite new order inflows continued to expand at a relatively subdued pace, with growth picking up only slightly from August’s 26-month low.

Staffing levels fell across both the manufacturing and service sectors in September. Although the decline in services employment was only slight, it marked the first reduction in the sector for over two years. At manufacturers, workforce numbers fell at a pace that, though modest, was the quickest for 14 months. Companies across both monitored sectors indicated that company restructuring plans and the non-replacement of voluntary leavers had contributed to lower employment. At the composite level, headcounts fell at the fastest rate since August 2016.

Outstanding workloads fell at services companies in September, as has been the case in four of the past five months. That said, the rate of backlog depletion was only slight. Conversely, the level of work-in-hand (but not yet completed) rose further at manufacturers, albeit to the weakest extent in 12 months. Unfinished business at the composite level therefore rose only slightly at the end of the third quarter.

Average input costs faced by Chinese businesses rose further in September. In the service sector, the rate of input price inflation accelerated to the second-steepest since May 2012 (behind January 2018). According to panellists, higher prices for fuel, raw materials and greater staffing costs all underpinned the latest increase in operating expenses. Input costs also rose solidly at manufacturing companies, despite the rate of increase softening since August. Measured on a composite basis, input price inflation accelerated to a three-month high in September.

Despite the faster increase in input costs, services companies signalled broadly no change to their output charges, with some firms mentioning greater efforts to remain competitive. Factory gate prices meanwhile rose further in September, albeit at a modest pace. Overall, prices charged for Chinese goods and services increased at a marginal pace that was the slowest recorded since June 2017.

Chinese companies are generally optimistic that output will increase over the next year. However, the degree of positive sentiment fell to a nine-month low at manufacturers amid concerns of ongoing global trade tensions and more restrictive environmental policies, while confidence also slipped across the service sector. Measured across both sectors, expectations fell to their second-lowest in ten months.

Comment

Commenting on the China General Services PMI data, Dr. Zhengsheng Zhong, director of Macroeconomic Analysis at CEBM Group said:

“The Caixin China General Services Business Activity Index rebounded to 53.1 in September from 51.5 in August. New business increased at a faster rate last month than in August, pointing to some improvement in demand. However, employment in the service industry contracted abruptly and that sub-index fell to its lowest level since March 2016. Prices charged by service providers declined for the first time in 13 months, while input costs rose at their quickest pace since January, which could squeeze company profit margins. Reflecting that, the sub-index of business expectations, which gauges service companies' confidence toward the prospects of their operations over the next 12 months, edged down in September from the previous month.

“The Caixin China Composite Output Index inched up to 52.1 last month from 52.0 in August, indicating the performance of the Chinese economy was stable for the month. However, demand remained subdued as the growth rate for new orders, although marginally higher than the previous month, lingered at a low level. The increase in output prices slowed while the gain in input prices accelerated slightly. That meant companies were still under relatively large cost pressures, which contributed to a fall in the sub-index of future output.

“What we should be wary of is that overall employment contracted in September, with the sub-index hitting its lowest level since August 2016. The deterioration in employment will test policymakers' determination in pressing ahead with reforms.”

About The Caixin China General Services PMI

The Caixin China General Services PMI is based on data compiled from monthly replies to questionnaires sent to purchasing executives in over 400 companies. The panel has been carefully selected to accurately replicate the true structure of the services economy.

Survey responses reflect the change, if any, in the current month compared to the previous month based on data collected mid-month. For each of the indicators the ‘Report’ shows the percentage reporting each response, the net difference between the number of higher/better responses and lower/worse responses, and the ‘diffusion’ index. This index is the sum of the positive responses plus a half of those responding ‘the same’.

Diffusion indexes have the properties of leading indicators and are convenient summary measures showing the prevailing direction of change. An index reading above 50 indicates an overall increase in that variable, below 50 an overall decrease.

The Purchasing Managers’ Index (PMI) survey methodology has developed an outstanding reputation for providing the most up-to-date possible indication of what is really happening in the private sector economy by tracking variables such as sales, employment, inventories and prices. The indices are widely used by businesses, governments and economic analysts in financial institutions to help better understand business conditions and guide corporate and investment strategy. In particular, central banks in many countries use the data to help make interest rate decisions. PMI surveys are the first indicators of economic conditions published each month and are therefore available well ahead of comparable data produced by government bodies.

About Caixin

Caixin Media isChina's leading media group dedicated to providing financial and business news through periodicals, online content, mobile applications, conferences, books and TV/video programs.

Caixin Insight Group is a high-end financial data and analysis platform. The group encompasses the monthly Caixin China Purchasing Managers' Index, components of which include the Caixin China General Manufacturing PMI™ and CaixinChinaGeneral Services PMI™. These indexes are closely watched worldwide as reliable snapshots ofChina's economic health.

About IHS Markit

IHS Markit is a world leader in critical information, analytics and solutions for the major industries and markets that drive economies worldwide. The company delivers next-generation information, analytics and solutions to customers in business, finance and government, improving their operational efficiency and providing deep insights that lead to well-informed, confident decisions. IHS Markit has more than 50,000 business and government customers, including 80 percent of the Fortune Global 500 and the world’s leading financial institutions.

About PMI

Purchasing Managers’ Index (PMI) surveys are now available for over 40 countries and also for key regions including the eurozone. They are the most closely-watched business surveys in the world, favoured by central banks, financial markets and business decision makers for their ability to provide up-to-date, accurate and often unique monthly indicators of economic trends.

Share on:

Testimonial

"In a year when every marketing dollar mattered, I chose to keep I-Connect007 in our 2025 plan. Their commitment to high-quality, insightful content aligns with Koh Young’s values and helps readers navigate a changing industry. "

Brent Fischthal - Koh YoungSuggested Items

Marcy’s Musings: The Legislative Outlook—Helping or Hurting?

10/20/2025 | Marcy LaRont -- Column: Marcy's MusingsJust before we were ready to publish our October issue of PCB007 Magazine, some breaking news from the White House, unfortunately (but perfectly) parlayed into why the topic of this month’s issue has been so important to cover in great depth.

China Expands Rare Earth Export Restrictions, Tightening Grip on Global Supply Chains

10/16/2025 | I-Connect007 Editorial TeamChina sharply expanded its rare earth export restrictions on Oct. 9, adding additional elements and refining technologies to its control list while imposing stricter rules on foreign users in the defense and semiconductor industries.

Critical Minerals: The New Power Play in Global Trade

10/13/2025 | Marcy LaRont, I-Connect007Access to critical minerals essential for electronics manufacturing, and China’s monopoly of them, is increasingly under scrutiny, with gallium (Ga) and germanium (Ge)at the forefront of this discourse. However, all critical minerals imported from China share a similar narrative, and understanding the implications of this dependency and the risks to both U.S. commercial and defense sectors has created an urgent need for a comprehensive electronics strategy to secure and diversify access to these vital minerals. In this candid interview, USPAE Executive Director Jim Will discusses the issues and the mitigation steps that must be taken to adequately address them.

I-Connect007 Editor’s Choice: Five Must-Reads for the Week

09/26/2025 | Marcy LaRont, I-Connect007Though the news cycle felt a little less exclamatory this week, there were many global business news headlines worth revisiting. Among them, China announced a bold carbon emissions goal of 10% over the next decade to double its solar and wind power capacity. The Wall Street Journal published an article, “Global Port Leaders See Trade Shifting, Not Slowing,” a nod to businesses’ risk mitigation strategies and execution around overreliance on China coming into play in a bigger way.

Global Citizenship: Together for a Perfect PCB Solution

09/10/2025 | Tom Yang -- Column: Global CitizenshipIf there’s one thing we’ve learned in the past few decades of electronics evolution, it’s that no region has a monopoly on excellence. Whether it’s materials science breakthroughs in Europe, manufacturing efficiencies in China, or design innovations in Silicon Valley, the PCB industry thrives on collaboration.