Dan’s Biz Bookshelf: ‘Abundance: How We Build a Better Future’

Dan’s Biz Bookshelf: ‘Abundance: How We Build a Better Future’ Trouble in Your Tank: In Complex Systems, Design Rules Aren’t Optional

Trouble in Your Tank: In Complex Systems, Design Rules Aren’t Optional It’s Only Common Sense: The Phone Is Still Your Competitive Advantage

It’s Only Common Sense: The Phone Is Still Your Competitive Advantage

U.S. Companies Continue to Represent Largest Share of Fabless IC Sales

March 27, 2019 | IC InsightsEstimated reading time: 3 minutes

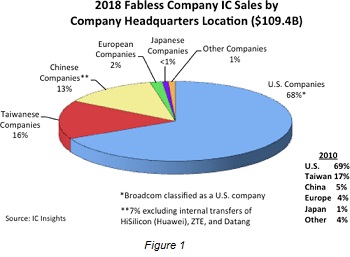

The 2018 fabless company share of IC sales by company headquarters location. With 68%, the U.S. companies continued to hold the dominant share of fabless IC sales last year, just one percentage point less than in 2010.

Since 2010, the largest fabless IC marketshare increase has come from the Chinese suppliers, which held a 13% share last year as compared to only 5% in 2010. In 2018, four of the top five fastest growing fabless IC companies (with greater than $200 million in sales) were Chinese companies (BitMain, ISSI, Allwinner, and HiSilicon). However, when excluding the internal transfers of HiSilicon (over 90% of its sales go to its parent company Huawei), ZTE, and Datang, the Chinese share of the fabless company IC sales drops by about half to 7%.

European companies held only 2% of the fabless IC company marketshare in 2018 as compared to 4% in 2010. This loss of share was partly due to the acquisition of U.K.-based CSR, the second-largest European fabless IC supplier, by U.S.-based Qualcomm in 1Q15 and the purchase of Germany-based Lantiq, the third-largest European fabless IC supplier, by U.S.-based Intel in 2Q15. These acquisitions left U.K.-based Dialog ($1.44 billion in sales in 2018) and Norway-based Nordic ($271 million in sales in 2018) as the only Europe-headquartered fabless IC suppliers in the top 50-company ranking last year.

There was only one Japanese firm in the 2018 top-50 fabless supplier ranking—Megachips, which saw its sales jump by 19% in 2018 to $760 million. The lone South Korean company—Silicon Works, had a 17% increase in sales last year to $718 million.

Worldwide fabless IC sales increased by $8.3 billion in 2018, which represented an 8% increase from 2017. In total, 16 of the top 50-fabless IC suppliers had better results than the global 2018 IC market increase of 14%. Overall, 21 of the top 50 fabless IC suppliers registered double-digit growth rates last year while five companies logged double-digit declines. Five fabless companies—China-based BitMain, ISSI, Allwinner, and HiSilicon, and U.S.-based Nvidia—registered ≥25% growth in 2018.

The fastest growing fabless IC supplier in 2018, at 197%, was China-based BitMain, which has had a very interesting past couple of years. It should be noted that labeling BitMain an IC supplier is a bit misleading. BitMain is an electronic system supplier of cryptocurrency mining equipment. Since the company does not sell individual ICs on the open market, its IC “sales” are similar to those IC Insights lists for Apple, with BitMain’s IC sales essentially being the value of ICs it purchases from its sole-source foundry—TSMC.

It is estimated that BitMain held an 84% share of the $5.0 billion worldwide cryptocurrency mining equipment market in 2018. The company had a meteoric rise in its sales over the past three years. BitMain’s total sales were $278 million in 2016, $2.5 billion in 2017, and an estimated $4.4 billion in 2018. The company’s equipment sales are very closely tied to the price of cryptocurrencies, especially Bitcoin. With the crash of Bitcoin prices from $18,000 in January 2018 to $3,500 in December 2018, IC Insights estimates BitMain’s total sales went from a company-published $2.8 billion in 1H18 to $1.6 billion in 2H18.

IC Insights believes that BitMain’s steep rise and fall in cryptocurrency mining equipment sales since 2016 is responsible for the majority of the volatility of TSMC’s China-based foundry sales over the past two years (Figure 2).

Overall, IC Insights believes that most of the large fabless IC suppliers will continue to do well and will help drive significant sales gains by the major IC foundries (e.g., TSMC, GlobalFoundries, Samsung, UMC, etc.). Moreover, as the barriers to entry (i.e., high design costs, increasingly difficult access to venture capital money, etc.) rise, and fewer fabless companies are founded, IC Insights believes that the total fabless IC supplier listing will continue to grow increasingly “top-heavy” in the future.

Share on:

Subscribe

Stay ahead of the technologies shaping the future of electronics with our latest newsletter, Advanced Electronics Packaging Digest. Get expert insights on advanced packaging, materials, and system-level innovation, delivered straight to your inbox.

Subscribe now to stay informed, competitive, and connected.

Suggested Items

A Necessary Shift From Gerber to IPC-2581

05/07/2026 | Tracy Riggan, Global Electronics AssociationIPC-2581 is an open, vendor-neutral data exchange standard developed by the Global Electronics Association to streamline the exchange of PCB design information across fabrication, assembly, and test. It replaces multiple legacy formats—including industry standards, Gerber, and ODB++—with a single, comprehensive, XML-based dataset that captures all manufacturing details.

How Are You Vetting Your Supply Chain?

04/28/2026 | Didrik Bech, CONFIDEEFor many years, supplier management was largely focused on standard commercial priorities: cost, quality, lead time, and delivery performance. If a supplier met specifications, shipped on time, and remained price competitive, the relationship was often considered healthy. However, the world has changed.

Global Sourcing Spotlight: Building a Supply Chain That Bends, Not Breaks

04/29/2026 | Bob Duke -- Column: Global Sourcing SpotlightThe global supply chain is a complex, interdependent, and shifting organism. In the past few years, pandemics, tariffs, wars, natural disasters, and transportation chaos have tested it like never before, revealing that fragility is expensive. The companies that survive do so not through luck but through resiliency. For decades, companies built sourcing strategies around the illusion of stability—one supplier, region, and price. It worked until a port closed, a single supplier went down, or a production line froze.

TTC-LLC and TTCI: Smarter Training, Stronger Test at PCB East 2026

04/27/2026 | The Test Connection Inc.The Training Connection LLC (TTC-LLC) and The Test Connection, Inc. (TTCI) will be exhibiting together at PCB East 2026, taking place April 28–May 1 at the DCU Convention Center in Worcester, Massachusetts. Attendees can find both teams at Booth #103 during the main exhibition day on Wednesday, April 29.

New Guidance Targets Scope 3.1 Emissions Gap in Electronics Supply Chains

04/22/2026 | I-Connect007 Editorial TeamA new industry guidance document aimed at improving how electronics companies account for Scope 3 Category 1 (Scope 3.1) emissions marks a significant step toward more consistent and effective supply chain decarbonization. A recent webinar hosted by the Global Electronics Association and the Responsible Business Alliance (RBA) addressed a persistent challenge: Despite the material impact of Scope 3.1 emissions, fewer than half of electronics companies currently report them.