The Right Approach: Get Ready for ISO 9001 Version 6

The Right Approach: Get Ready for ISO 9001 Version 6 Dan’s Biz Bookshelf: ‘Still Broke: Walmart’s Remarkable Transformation'

Dan’s Biz Bookshelf: ‘Still Broke: Walmart’s Remarkable Transformation' Driving Innovation: Depth Routing Processes—Achieving Unparalleled Precision in Complex PCBs

Driving Innovation: Depth Routing Processes—Achieving Unparalleled Precision in Complex PCBs

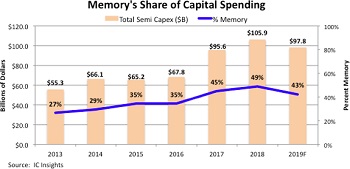

Memory Forecast to Account for 43% of Total 2019 Semi Spending

September 11, 2019 | IC InsightsEstimated reading time: 1 minute

Capex spending for memory ICs was the driving factor behind very strong increases in industry-wide capex spending over the past two years. Most of those upgrades and expansion plans are now completed or have entered their final building phases. As a result, memory capex is forecast to account for 43% of total semi industry capital spending this year, down from 49% in 2018. Total semiconductor capital expenditures are forecast to slip 8% in 2019 to $97.8 billion following the record high spending level of $105.9 billion set in 2018.

The share of capital spending for memory devices has increased substantially in seven years, growing from 27% ($14.7 billion) in 2013 to a record high level of 49% ($52.0 billion) in 2018 to a forecast of 43% ($41.6 billion) of total industry capex in 2019, which equates to a 2013-2019 CAGR of 18.9%.

The IC product segment receiving the most spending in 2017 and 2018 was the Flash/Non-Volatile memory category. However, with Samsung, SK Hynix, and Micron adding capacity for both DRAM and NAND flash and Intel, Toshiba Memory/Western Digital/SanDisk, and XMC/Yangtze River Storage Technology all significantly ramping up 3D NAND flash capacity over the past 18 months, the DRAM and NAND flash memory markets have entered a period of overcapacity and pricing weakness. This is evident by the steep decline in the price per bit of both DRAM and NAND flash and the steep cutback in capex spending forecast for 2019.

In 2019, capital spending in the DRAM and Flash memory segments is expected to drop by 19% and 21%, respectively. Total memory capital spending is expected to be $41.6 billion in 2019, a decline of $10.4 billion from last year. The big cutbacks in spending in the DRAM and flash market segments this year are an attempt by the major memory suppliers to prevent further price erosion in the second half of 2019 and into 2020. How far memory prices continue to fall will be determined in large part by how much memory suppliers trim their capital spending for these devices this year and next and if lower price per bit triggers additional bit volume demand.

Share on:

Testimonial

"Our marketing partnership with I-Connect007 is already delivering. Just a day after our press release went live, we received a direct inquiry about our updated products!"

Rachael Temple - AlltematedSuggested Items

Alphabet Boosted by AI, Cloud Demand as Spending Needs Jump

07/24/2025 | I-Connect007 Editorial TeamGoogle’s parent company, Alphabet Inc., said that demand for artificial intelligence products boosted its quarterly sales, and now requires an extreme increase in capital spending to keep up in the AI race, Bloomberg reported. For 2025, the company stated its capital expenditure will be $85 billion—$10 billion more than previously forecast.

Report: Broadcom Scraps $1 Billion Chip Investment in Spain

07/15/2025 | I-Connect007 Editorial TeamAmerican chipmaker Broadcom has pulled out of plans to invest in a microchip plant in Spain. According to a July 14 Reuters report, Europa Press, quoting anonymous sources, stated the action followed collapsed government talks but gave no further information.

Wolfspeed Stock Soars After Filing for Chapter 11 Bankruptcy

07/01/2025 | I-Connect007 Editorial TeamOn July 1, Wolfspeed shares doubled following the company’s announcement on June 30 that it had filed for Chapter 11 bankruptcy protection.

Takeaways from the Keynotes at the Edinburgh EIPC Summer Conference

06/16/2025 | Pete Starkey, I-Connect007It was seasonably wet and windy in Edinburgh, Scotland, June 3-4, where delegates from 17 countries convened for the 2025 EIPC Summer Conference to enjoy a superlative program of 18 technical presentations over two days, plus an excursion to a whisky distillery. EIPC President Alun Morgan welcomed everyone to the Delta Hotel, reminding us that in its previous iteration, it was the Royal Scot, traditionally the annual venue of the Institute of Circuit Technology Northern Symposium.

Tariff Effects and China Subsidies Soften 1Q25 Downturn; Foundry Revenue Decline Narrows to 5.4%

06/09/2025 | TrendForceTrendForce’s latest investigations find that the global foundry industry recorded 1Q25 revenue of US$36.4 billion—a 5.4% QoQ decline. The downturn was softened by last-minute rush orders from clients ahead of the U.S. reciprocal tariff exemption deadline, as well as continued momentum from China’s 2024 consumer subsidy program.