The Marketing Minute: Marketing With Layers

The Marketing Minute: Marketing With Layers The Right Approach: Electro-Tek—A Williams Family Legacy, Part 1

The Right Approach: Electro-Tek—A Williams Family Legacy, Part 1 It’s Only Common Sense: If You’re Not Differentiated, You’re Dead

It’s Only Common Sense: If You’re Not Differentiated, You’re Dead

Production Capacity for Power Management ICs Will Grow by 4.7% YoY for 1H23

January 6, 2023 | TrendForceEstimated reading time: 3 minutes

The effect of the low season, the planned scale-back of capital expenditure on the part of enterprises, and the ongoing slump in the wider consumer electronics market are going to constrain the demand for power management ICs during 1H23. On the supply side, Texas Instruments (TI) as the leading supplier for power management ICs will be activating the newly added production capacity at its production sites RFAB2 and LFAB in the same period. Given this circumstance, TrendForce projects that the global production capacity for power management ICs will increase by 4.7% YoY for 1H23. In the market for power management ICs, falling demand for products belonging to consumer electronics, networking devices, and industrial equipment continues to generate downward pressure on prices. Consequently, quotes for power management IC orders are projected to register a sequential drop of 5~10% during 1H23. Conversely, demand remains stable for automotive products thanks to the trend of vehicle electrification. Even though the weakening of the wider economy is causing uncertainties across the whole automotive market, prices are not expected to fluctuate significantly because of buyers and sellers of automotive products have mostly established long-term partnerships. Therefore, the demand coming from the automotive market is going to emerge as the only major driving force behind sales of power management ICs.

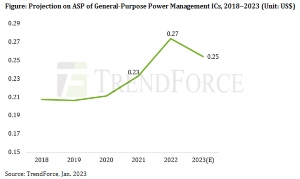

Major IDMs Control 63% of Power Management IC Market

Suppliers for power management ICs are diverse and include the major international IDMs as well as fabless IC design companies. Suppliers that are IDMs include TI, ADI, Infineon, Renesas, Onsemi (onsemi), STMicroelectronics (ST), and NXP. Suppliers that are fabless IC design companies include Qualcomm, MPS, MediaTek, Anpec, GMT, Leadtrend, Weltrend, Silergy, BPS, and SG Micro. By shipment market share, IDMs collectively control 63% of the global market for power management ICs; and among them, TI is the leader with a 22% global market share. TI has the advantages of having a diverse range of offerings, a consistently high product quality, and an ample amount of production capacity. Thus, it exerts an enormous influence over the global power management IC market. Looking at the general price trend of power management ICs in 2022, IDMs were able to further push up the ASP in response to rising inflation. Conversely, quotes from fabless IC design companies were first to show a weakening trend.

Suppliers Are Cutting Prices to Drive Sales of Power Management ICs for Consumer Electronics; Automotive Products and Industrial Equipment Are the Only Applications That Exhibit Stable Demand

TrendForce points out that prices of power management ICs for consumer electronics (e.g., laptop computers, tablets, TVs, and smartphones) began to drop in 3Q22, with the QoQ decline coming to 3~10%. In 4Q22, prices fell by another 5~10% QoQ for a wide range of consumer power management ICs (e.g., those related to AC-DC, DC-DC, LDO, buck, boost, PWM, and battery charger). Besides this development, demand also began to weaken for power management ICs used in networking devices and most kinds of industrial equipment. The only applications that still exhibited stable demand were a very few specific kinds of industrial equipment (e.g., military hardware) and automotive products. At that time, order visibility for these application was already extended to 2Q23. And there were no notable attempts to drive sales of related power management ICs through price cutting.

However, TrendForce also notes that IDMs together hold a market share of more than 83% for power management ICs embedded in industrial equipment and automotive products. Fabless IC design companies for the most part still have difficulties in penetrating into these particular market segments, but their efforts have been aggressive as the overall demand for consumer electronics remains depressed. Currently, fabless IC design houses are working hard to get their new automotive and industrial power management ICs qualified as soon as possible.

Regarding the lead time for power management IC orders, TrendForce’s latest investigation finds that fabless IC design houses now have an average lead time of 12~28 weeks. Moreover, existing stock is so large for some models of power management ICs that fabless IC design houses can begin shipments right after receiving the incoming order. Turning to IDMs, they still mostly have a longer lead time. For power management ICs belonging to non-automotive applications, IDMs have a lead time of 20~40 weeks. For power management ICs belonging to automotive applications, IDMs have a lead time of more than 32 weeks. On the whole, orders are still in the allocation status for automotive power management ICs that come from very few suppliers and have a drawn-out process for chip manufacturing, module assembly, and qualification.

Share on:

Testimonial

"Our marketing partnership with I-Connect007 is already delivering. Just a day after our press release went live, we received a direct inquiry about our updated products!"

Rachael Temple - AlltematedSuggested Items

Keysight Completes Acquisition of Synopsys’ Optical Solutions Group and Ansys’ PowerArtist

10/17/2025 | Keysight Technologies, Inc.Keysight Technologies, Inc., announced the completion of its acquisitions of the Optical Solutions Group from Synopsys, Inc., and PowerArtist from Ansys, Inc.

RT-Labs Joins STMicroelectronics Partner Program to Accelerate Industrial Communication

10/16/2025 | RT-LabsRT-Labs, a leading provider of real-time software solutions for industrial automation, announces that it has joined the STMicroelectronics Partner Program to integrate its Ethernet-based industrial communication stacks into ST’s development environments and microcontroller platforms.

ASC Sunstone Circuits Adds New Options to OneQuote While Maintaining Real-Time Pricing on Core PCB Features

10/16/2025 | ASC Sunstone CircuitsASC Sunstone Circuits, a leading U.S. PCB manufacturer, today announced a significant expansion of its OneQuote online quoting tool, giving design engineers more control over complex PCB configurations — making it easier for the quote team to quickly clarify and verify specifications, reducing delays from manual quote reviews.

Analog Devices Launches ADI Power Studio™ and New Web-Based Tools

10/14/2025 | Analog Devices, Inc.Analog Devices, Inc., a global semiconductor leader, announced the launch of ADI Power Studio, a comprehensive family of products that offers advanced modeling, component recommendations and efficiency analysis with simulation. In addition, ADI is introducing early versions of two new web-based tools with a modernized user experience under the Power Studio umbrella:

Cadence Giving Foundation Announces Multi-Year Commitment to Expand the AI Hub at San José State University

10/13/2025 | Cadence Design Systems, Inc.The Cadence Giving Foundation today announced a multi-year commitment to expand the AI Hub at San José State University (SJSU) to equip students with the skills, hands-on training and experience needed to excel in careers in artificial intelligence (AI).