Global PCB Connections: Rigid-flex and Flexible PCBs—The Backbone of Modern Electronics

Global PCB Connections: Rigid-flex and Flexible PCBs—The Backbone of Modern Electronics Flexible Thinking: The Key to a Successful Flex Circuit Design Transfer

Flexible Thinking: The Key to a Successful Flex Circuit Design Transfer Happy’s Tech Talk #29: Bend-to-Install Semi-flex FR-4

Happy’s Tech Talk #29: Bend-to-Install Semi-flex FR-4

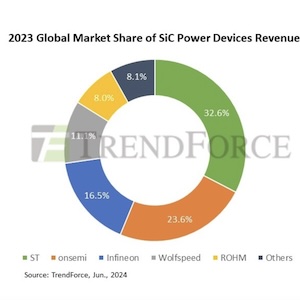

ST Maintains Top Spot with 32.6% Market, onsemi Rises to Second Place in 2023 Revenue Ranking for SiC Power Devices

June 21, 2024 | TrendForceEstimated reading time: 3 minutes

TrendForce reports that the SiC power devices industry maintained strong growth in 2023, driven by the application of BEVs. The top five suppliers accounted for approximately 91.9% of total revenue; ST lead the pack with a 32.6% market share while onsemi rose from fourth place in 2022 to second place.

TrendForce’s analysis indicates that demand from AI servers and other fields will significantly increase in 2024. However, the noticeable slowdown in the sales growth of BEVs and weakening industrial demand are affecting the SiC supply chain. It is expected that the annual growth rate of industry revenue for SiC power devices will significantly decelerate in 2024 compared to previous years.

ST, as a key supplier of automotive SiC MOSFETs, is building a full-process SiC factory in Catania, Italy that is expected to be operational by 2026. Additionally, the 8-inch SiC joint venture factory established by ST and Sanan Optoelectronics in China is anticipated to be up and running by the end of this year. This will enable ST to achieve vertical integration by combining local post-processing production lines and supporting substrate material factories provided by Sanan Optoelectronics.

onsemi’s SiC business has progressed rapidly in recent years, mainly due to its automotive EliteSiC series. The company’s SiC wafer factory in Bucheon, South Korea, completed its expansion in 2023 and plans to transition from 8-inch production after completing relevant technical verification in 2025. Since acquiring GTAT, Onsemi’s self-sufficiency rate for SiC substrate materials has exceeded 50%. With the increase in internal material production capacity, the company is moving toward achieving a gross profit margin of 50%.

Infineon’s SiC revenue is nearly half derived from the industrial market, but its main customer at the Kulim, Malaysia plant, SolarEdge, is facing difficulties, which has impacted Infineon’s operations. In contrast, Infineon’s automotive business is developing more robustly, as evidenced by the recent design win with Xiaomi SU7. Interestingly, Infineon’s previously lagging capacity expansion progress now positions it favorably amid market headwinds. Unlike other leading SiC IDM manufacturers, Infineon lacks internal production capabilities for SiC crystal materials and is actively promoting a diversified supplier system to ensure supply chain stability.

Wolfspeed’s operational strategy missteps have caused it to miss market opportunities over the past two years, leading to setbacks in its power device business. However, Wolfspeed remains the world’s largest supplier of SiC materials—particularly for automotive-grade MOSFET substrates—and has a first-mover advantage in the 8-inch domain.

With Wolfspeed’s JP plant about to start production, it is expected to significantly increase material capacity and advance the progress of the Mohawk Valley Fab (MVF) plant’s commissioning. Despite this, Wolfspeed still faces enormous idle capacity and startup costs, which is putting significant pressure on its financial situation. The operational progress of the MVF and JP plans will determine whether Wolfspeed can smoothly navigate this challenging period.

ROHM recently acquired Solar Frontier’s Kunitomi plant as its fourth SiC plant and plans to begin production of 8-inch SiC substrates this year, followed by the manufacturing of power devices. The company has established long-term partnerships with automotive companies and Tier 1 suppliers, such as Vitesco Technologies, Mazda, and Geely, accelerating the development of the next generation of power modules to boost its market share.

TrendForce believes that overall, the SiC industry is in a phase of rapid growth and intense competition, where economies of scale are more critical than any other factor. Leading IDM manufacturers have shifted from their previous conservative and steady strategies to actively investing in SiC expansion plans, aiming to establish a leadership position. Currently, more than 10 companies worldwide are investing in the construction of 8-inch SiC wafer plants. As the market continues to expand, competition in the SiC field is expected to become even more intense.

Share on:

Testimonial

"Your magazines are a great platform for people to exchange knowledge. Thank you for the work that you do."

Simon Khesin - Schmoll MaschinenSuggested Items

Elementary, Mr. Watson: High Power: When Physics Becomes Real

10/15/2025 | John Watson -- Column: Elementary, Mr. WatsonHave you ever noticed how high-speed design and signal integrity classes are always packed to standing room only, but just down the hall, the session on power electronics has plenty of empty chairs? It's not just a coincidence; it's a trend I've observed over the years as both an attendee and instructor.

Trio Wins Nobel Prize for Groundbreaking Quantum Physics Experiments

10/08/2025 | I-Connect007 Editorial TeamU.S.-based scientists John Clarke, Michel Devoret, and John Martinis have won the 2025 Nobel Prize in Physics for “experiments that revealed quantum physics in action.” Reuters reported. Their work laid the foundation for the next generation of digital technologies, the Royal Swedish Academy of Sciences announced on Oct. 7.

Infineon, ROHM Collaborate on Silicon Carbide Power Electronics Packages to Enhance Flexibility for Customers

09/25/2025 | InfineonInfineon Technologies AG and ROHM Co., Ltd. have signed a Memorandum of Understanding to collaborate on packages for silicon carbide (SiC) power semiconductors used in applications such as on-board chargers, photovoltaics, energy storage systems and AI data centers.

Global Traction Inverter Installations Up 19% YoY in 2Q25, Range-Extended EVs Driving Wider SiC Adoption

09/10/2025 | TrendForceTrendForce’s latest report, “Global EV Inverter Market Data,” reveals that global installations of EV traction inverters reached 7.66 million units in 2Q25, up 19% YoY, buoyed by strong BEV sales.

UHDI Fundamentals: UHDI Technology and Industry 4.0

09/03/2025 | Anaya Vardya, American Standard CircuitsUltra high density interconnect (UHDI) technology is rapidly transforming how smart systems are designed and deployed in the context of Industry 4.0. With its capacity to support highly miniaturized, high-performance, and densely packed electronics, UHDI is a critical enabler of the smart, connected, and automated industrial future. Here, I’ll explore the synergy between UHDI and Industry 4.0 technologies, highlighting applications, benefits, and future directions.