The Chemical Connection: When History Repeats Itself on Diversification

The Chemical Connection: When History Repeats Itself on Diversification It’s Only Common Sense: AI Is Accelerating the Electronics Industry

It’s Only Common Sense: AI Is Accelerating the Electronics Industry Punching Out: M&A Deals in North American PCB and EMS Sectors for the First Half of 2026

Punching Out: M&A Deals in North American PCB and EMS Sectors for the First Half of 2026

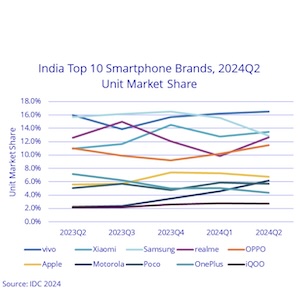

According to the International Data Corporation ’s (IDC) Worldwide Quarterly Mobile Phone Tracker, the Indian smartphone market shipped 69 million smartphones in 1H24, with 7.2% growth YoY (year-over-year). In 2Q24, the market shipped 35 million smartphones, with growth of 3.2% YoY. Although it is the fourth consecutive quarter of YoY shipment growth, muted consumer demand and rising ASPs continue to restrict swift annual recovery.

“The latter half of the second quarter is a prelude to the crucial second half of the year with festive sale period going up till November. Apart from old inventory clearance in the first half of the quarter, vendors also started to launch new smartphones, especially in the mid-premium/premium segment (mostly China-based vendors) from mid-quarter onwards, for monsoon sales in July and August,” said Upasana Joshi, Senior Research Manager, Devices Research, IDC India.

Key Highlights for 2Q24:

• Smartphone ASPs (average selling price) grew by 2.8% YoY; however, they declined QoQ by 5.6%, at US$248.

- The entry-level (sub-US$100) segment witnessed a strong decline of 36% YoY to 14% share, down from 22% a year ago. Xiaomi continued to lead this space, followed by Poco and realme.

- Shipments to the mass budget (US$100<US$200) segment grew by 8% YoY, with a marginal increase in share to 44% from 42%. The top 3 brands were Xiaomi, realme and vivo, making up 60% of this segment.

- The share of entry-premium (US$200<US$400) segment reached 30%, up from 22% and registered highest growth of 42% YoY. OPPO, vivo and Samsung gained a significant share compared to the previous quarter, making up almost 60% of this segment.

- The mid-premium segment (US$400<US$600) segment declined by 25% in unit terms to a 4% share, down from 5% a year ago. vivo the major gainer, led with a 25% share, followed by OnePlus and OPPO.

- The premium segment (US$600<US$800) held 2% share and declined by 37% in unit terms. Key models were the iPhone 13, Galaxy S23FE, iPhone 12 and OnePlus12. Apple’s share increased YoY to 61%, while Samsung’s share increased to 24%, from 21% a year ago.

- The super-premium segment (US$800+) momentum continued with 22% growth and its share up from 6% to 7%. The iPhone15/15 Plus/14/14 Plus together accounted for 77% of shipments, followed by the Galaxy S24/S24 Ultra with an 11% share. Overall, Apple led the segment with a share of 83%, followed by Samsung at 16%.

- 27 million 5G smartphones were shipped in the quarter, the share of 5G smartphone shipments increased to 77%, up from 49% in 2Q23, while 5G smartphone ASPs declined by 22% YoY to US$293. Within 5G, shipments of the mass budget (US$100<US200) segment grew by 2.5x to reach 45% share. Xiaomi’s Redmi 13C, OPPO’s F25 Pro, realme’ s 12x, Xiaomi’s Redmi 12 and realme’ s C65, were the highest shipped 5G models in 2Q24,

• Shipments to online channels grew by 8% YoY, and its share increased to 50% in 2Q24 compared to 47% in 2Q23. Motorola entered the top five vendor list in the online channel, at the fourth slot, while vivo climbed to the second slot, led by its T series models. Due to severe heatwave conditions in major parts of India, offline channel shipments declined by 2% YoY in 2Q24.

• Overall, vivo continued to lead for the second consecutive quarter, with multiple launches across price segments through the Y series, mid-premium V series and flagship X Fold 3 Pro. Motorola registered the highest growth backed by product portfolio across price segments, while Nothing witnessed the second-highest growth amongst all other brands.

“The premiumization trend in the smartphone market, led by Apple and Samsung, coupled with rising device costs is motivating China-based brands to expand beyond the mass segment. The entry-premium segment (US$200<US$400) is expected to see healthy growth, while the entry-level (sub-US$100) will remain challenged at least this year despite efforts around launching affordable 5G smartphones. Also, the marketing around GenAI smartphones will be more pronounced, amid heavy promotional activities around it," says Navkendar Singh, Associate Vice President, Devices Research, IDC.