Global PCB Connections: Rigid-flex and Flexible PCBs—The Backbone of Modern Electronics

Global PCB Connections: Rigid-flex and Flexible PCBs—The Backbone of Modern Electronics Flexible Thinking: The Key to a Successful Flex Circuit Design Transfer

Flexible Thinking: The Key to a Successful Flex Circuit Design Transfer Happy’s Tech Talk #29: Bend-to-Install Semi-flex FR-4

Happy’s Tech Talk #29: Bend-to-Install Semi-flex FR-4

LiDAR Market Projected to Reach US$5.352 Billion by 2029 Thanks to Advanced Autonomous Driving and Logistics Demand

January 20, 2025 | TrendForceEstimated reading time: 1 minute

TrendForce’s latest report, “2025 Infrared Sensing Application Market and Branding Strategies,” reveals that LiDAR is gaining traction in automotive markets—including passenger vehicles and robo-taxis—as well as in industrial applications such as robotics, factory automation, and logistics. Propelled by advancements in Level 3 and higher autonomous driving systems and logistics solutions, the global LiDAR market is forecast to grow from US$1.181 billion in 2024 to $5.352 billion in 2029, achieving a robust CAGR of 35%.

Under increasing market pressure, automakers are adopting cutting-edge technologies such as adaptive headlights and full-width taillights to enhance vehicle appeal and functionality. At the same time, they are integrating LiDAR into passenger vehicles to enable advanced driver assistance systems and Level 3 autonomous driving capabilities. Leading brands, including Volvo, General Motors, Audi, Volkswagen, BMW, Hyundai, Hongqi, Changan, Li Auto, AITO, NIO, Toyota, and Nissan, are at the forefront of this transition.

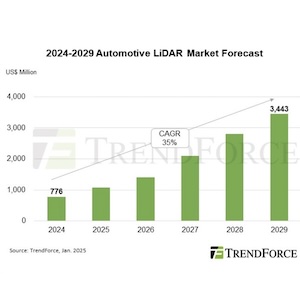

In the commercial vehicle segment, LiDAR is playing a critical role in autonomous buses, robo-taxis, and autonomous trucks supporting Level 4 functionalities. These applications include road shuttling and point-to-point transport, addressing labor shortages while reducing personnel and logistics costs. TrendForce predicts that as Level 3 and more advanced autonomous driving technologies mature and hit the road, the automotive LiDAR market will grow significantly, reaching $3.443 billion by 2029, with a CAGR of 35% from 2024 to 2029.

TrendForce highlights the growing adoption of industrial LiDAR in fields such as robotics, manufacturing processes, logistics, and security. The rapid expansion of e-commerce and increasing consumer reliance on fast delivery services have driven demand for logistics delivery vehicles. To reduce last-mile delivery costs and enhance efficiency, e-commerce and courier companies are increasingly turning to autonomous solutions.

For example, Serve Robotics and Uber have reached an agreement to deploy 2,000 delivery robots in 2025, primarily operating in the Los Angeles area. These robots are manufactured by Magna and equipped with NVIDIA-powered chips and Ouster’s LiDAR technology.

In smart cities, LiDAR supports traffic detection systems, providing real-time, accurate lane usage data to help authorities improve traffic flow and enhance road safety. Consumer applications, such as robotic vacuums and companion robots, are also adopting LiDAR to enable simultaneous localization and mapping technology. TrendForce estimates that the industrial and logistics LiDAR market will reach $1.909 billion by 2029, with a CAGR of 36% from 2024 to 2029.

Share on:

Testimonial

"We’re proud to call I-Connect007 a trusted partner. Their innovative approach and industry insight made our podcast collaboration a success by connecting us with the right audience and delivering real results."

Julia McCaffrey - NCAB GroupSuggested Items

Curtiss-Wright to Supply Turret Drive Stabilization Systems for U.S. Army XM30 Combat Vehicle Prototypes

10/16/2025 | BUSINESS WIRECurtiss-Wright Corporation announced that it has been selected by American Rheinmetall to provide its Turret Drive Stabilization System (TDSS) for the prototype phase of the U.S. Army’s XM30 Combat Vehicle (CV) program, which was recently approved to advance to Milestone B, the Engineering and Manufacturing Development (EMD) phase.

Episode 6 of Ultra HDI Podcast Series Explores Copper-filled Microvias in Advanced PCB Design and Fabrication

10/15/2025 | I-Connect007I-Connect007 has released Episode 6 of its acclaimed On the Line with... American Standard Circuits: Ultra High Density Interconnect (UHDI) podcast series. In this episode, “Copper Filling of Vias,” host Nolan Johnson once again welcomes John Johnson, Director of Quality and Advanced Technology at American Standard Circuits, for a deep dive into the pros and cons of copper plating microvias—from both the fabricator’s and designer’s perspectives.

American Standard Circuits Achieves Successful AS9100 Recertification

10/14/2025 | American Standard CircuitsAmerican Standard Circuits (ASC), a leading manufacturer of advanced printed circuit boards, proudly announces the successful completion of its AS9100 recertification audit. This milestone reaffirms ASC’s ongoing commitment to the highest levels of quality, reliability, and process control required to serve aerospace, defense, space, and other mission-critical industries.

Imec Launches 300mm GaN Program to Develop Advanced Power Devices and Reduce Manufacturing Costs

10/13/2025 | ImecImec, a world-leading research and innovation hub in nanoelectronics and digital technologies, welcomes AIXTRON, GlobalFoundries, KLA Corporation, Synopsys, and Veeco as first partners in its 300mm gallium-nitride (GaN) open innovation program track for low- and high-voltage power electronics applications.

Renesas Powers 800 Volt Direct Current AI Data Center Architecture with Next-Generation Power Semiconductors

10/13/2025 | RenesasRenesas Electronics Corporation, a premier supplier of advanced semiconductor solutions, announced that it is supporting efficient power conversion and distribution for the 800 Volt Direct Current power architecture announced by NVIDIA, helping fuel the next wave of smarter, faster AI infrastructure.