Dan’s Biz Bookshelf: Four Important Books You Need to Read (Not Just Say You Have)

Dan’s Biz Bookshelf: Four Important Books You Need to Read (Not Just Say You Have) The Marketing Minute: Cracking the Code of Technical Marketing

The Marketing Minute: Cracking the Code of Technical Marketing

Flat Panel Display Revenues Forecast to Fall in 2015

July 28, 2015 | IHSEstimated reading time: 3 minutes

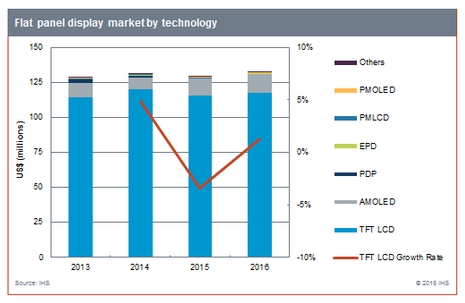

Led by declining thin-film-transistor liquid-crystal display (TFT LCD) revenues, global flat panel display (FPD) industry revenue is forecast to fall 2 percent, from $131.4 billion in 2014 to $129 billion in 2015. Dwindling TFT LCD display revenues, declining panel demand in the PC sector, along with ongoing panel-price erosion are the primary reasons for overall FPD revenue declines this year, according to IHS Inc. (NYSE: IHS), the leading global source of critical information and insight.

After growth last year, global TFT LCD display revenue is expected to decline 3 percent, from $120 billion in 2014 to $115.8 billion this year. However, IHS expects a return to TFT LCD market revenue growth in 2016. Plasma, cathode-ray tube (CRT), passive-matrix liquid crystal display (LCD) and electronic paper display (EPD) are also facing revenue declines, as some technologies become obsolete and others lack new applications. Organic light-emitting diode (OLED) is the only display technology expected to grow in 2015, according to the latest IHS Display Long-Term Demand Forecast Tracker.

TFT LCD display revenues grew 5 percent last year, from $114.4 billion to $120 billion, due mainly to strong growth in LCD TV panel shipments and higher panel prices. However this year the TFT LCD market is expected to decline for the following reasons:

- Falling demand for panels used in tablets, notebooks and desktop monitors

- Price erosion for smartphone panels in 2015, due to sharp increases in production for low-temperature polysilicon (LTPS) TFT LCD panels, which provide higher resolution and lower power consumption

- Declining open-cell LCD TV panel prices, including 4K UHD TV panels

Even as revenues decline in 2015, area demand for TFT LCD is still expected to grow nearly 4 percent, from 165.5 million square meters in 2014 to 172 million square meters in 2015. This shows that the revenue decline is being driven by average selling price (ASP) erosion.

“Panel prices are eroding for several reasons, including the swing in LCD TV panel inventory from limited supply to over-supply, which began in the second quarter of this year,” said David Hsieh, senior director of display research for IHS. “Other reasons include falling demand in the PC sector, and panel-capacity expansion pressure on smartphone displays, especially in LTPS panels. The entire FPD supply chain now must shift focus from growth to cost reduction, in order to maintain profitability.”

Active-matrix OLED (AMOLED) display revenues are projected to reach $11.8 billion in 2015, up 36 percent from 2014. Passive-matrix OLED (PMOLED) revenues are projected to reach $450 million this year, up 22 percent from last year.

“AMOLED growth is based on several factors, including soaring smartphone OLED display shipments, growth in OLED TV panel shipments, the expansion of OLED into tablet PCs and increased use in wearable devices, like Apple Watch. Flexible OLED is a key feature driving AMOLED revenues, especially given its higher ASP, attractive features and great value,” Hsieh said.

TFT LCD revenues in 2016 are expected to grow just over 1 percent, year over year, to reach $117.4 billion. The main reasons for the growth are further expansion of LCD TV features, such as larger display size, wider color gamut and further penetration of 4K UHD TV. These features will keep ASP rising; meanwhile, the emergence of the 4K displays for tablets, smartphones and desktop monitors will further increase ASP. Newer automotive displays, smart watches, public displays and other new applications will also add to TFT LCD revenue growth in 2016.

The IHS Display Long-Term Demand Forecast Tracker covers worldwide shipments and forecasts for all major FPD applications, including information from more than 140 FPD producers, covering more than ten countries. For information about purchasing this report, contact the sales department at IHS in the Americas at +1 844 301 7334 or AmericasLeads@ihs.com; in Europe, Middle East and Africa (EMEA) at +44 1344 328 300 or technology_emea@ihs.com; or Asia-Pacific (APAC) at +604 291 3600 or technology_APAC@ihs.com.

About IHS

IHS is the leading source of insight, analytics and expertise in critical areas that shape today’s business landscape. Businesses and governments in more than 150 countries around the globe rely on the comprehensive content, expert independent analysis and flexible delivery methods of IHS to make high-impact decisions and develop strategies with speed and confidence. IHS has been in business since 1959 and became a publicly traded company on the New York Stock Exchange in 2005. Headquartered in Englewood, Colorado, USA, IHS is committed to sustainable, profitable growth and employs about 8,800 people in 32 countries around the world.

Share on:

Testimonial

"We’re proud to call I-Connect007 a trusted partner. Their innovative approach and industry insight made our podcast collaboration a success by connecting us with the right audience and delivering real results."

Julia McCaffrey - NCAB GroupSuggested Items

Integrating Uniplate PLBCu6 With the Digital Factory Suite

09/12/2025 | Giovanni Obino and Andreas Schatz, MKS' AtotechPrinted circuit board manufacturing is rapidly changing, driven by miniaturization, stringent reliability requirements, and growing pressure for sustainable production. Meeting these challenges requires more than incremental improvements; it demands a combination of precise equipment and real-time process intelligence. The pairing of Uniplate® PLBCu6 with the Digital Factory Suite (DFS) demonstrates how hardware and software can work together to create more responsive, resource-efficient manufacturing.

Machvision Leads Shift to Automated Inline Final Inspection, AOI in North America

09/10/2025 | Ralph Jacobo, all4-PCBSchweitzer Engineering Laboratories (SEL) chose Machvision inspection equipment due to its capabilities and versatility. Machvision of Taiwan offers circuit inspection, hole inspection and measurement, IC Substrate and HDI inspection, and final visual inspection solutions. The best fit for SEL was the 4.0Pro Circuit Inspection for inner and outer layers, and the AFI6 for final visual inspection of finished panels.

Driving Innovation: Depth Routing Processes—Achieving Unparalleled Precision in Complex PCBs

09/08/2025 | Kurt Palmer -- Column: Driving InnovationIn PCB manufacturing, the demand for increasingly complex and miniaturized designs continually pushes the boundaries of traditional fabrication methods, including depth routing. Success in these applications demands not only on robust machinery but also sophisticated control functions. PCB manufacturers rely on advanced machine features and process methodologies to meet their precise depth routing goals. Here, I’ll explore some crucial functions that empower manufacturers to master complex depth routing challenges.

Securing the Future: The Battle for America's Flat Panel Display Industry

08/12/2025 | Marcy LaRont, I-Connect007The production and sourcing of flat panel displays have become a focal point of concern, particularly regarding national security. In this interview, Jim Will, executive director of the U.S. Partnership for Assured Electronics (USPAE), provides insights into the essential role of liquid crystal displays (LCDs) in both defense systems and everyday technology. Their conversation delves into the implications of America's dependence on Chinese manufacturers for these critical components, raising alarms about supply chain vulnerabilities amidst rising geopolitical tensions.

Omdia Forecasts Large-Area Display Shipments to Grow 2.9% YoY in 2025 Despite Economic Uncertainty

07/21/2025 | BUSINESS WIREAccording to the latest analysis from Omdia’s Large-area display market tracker – 2Q25 with 1Q25 results, large-area display (above 9-inch) unit shipments are forecast to increase by 2.9% year-over-year (YoY) in 2025.