Dan’s Biz Bookshelf: Four Important Books You Need to Read (Not Just Say You Have)

Dan’s Biz Bookshelf: Four Important Books You Need to Read (Not Just Say You Have) The Marketing Minute: Cracking the Code of Technical Marketing

The Marketing Minute: Cracking the Code of Technical Marketing

LCD TV Panel Suppliers Hurt by Weak Demand from Chinese TV Makers

October 13, 2015 | IHSEstimated reading time: 2 minutes

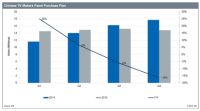

TV panel oversupply and falling prices are leading Chinese TV makers Hisense, TCL, Skyworth, Haier, Changhong and Konka to be more conservative in their panel purchasing plans, according to a new report from IHS Inc. (NYSE: IHS), the leading global source of critical information and insight.

The top six TV manufacturers in China plan to purchase just 14.8 million LCD TV panels, including open cell and modules, in the fourth quarter (Q4) of 2015, which is a 16 percent year-over-year decline from the 17.7 million displays shipped in Q4 2014, the report says.

As LG Display, Samsung Display, BOE, ChinaStar, AUO and Innolux are heavily invested in the Chinese market, the slowdown is expected to cause these panel manufacturers to adjust their capacity utilization still further this year.

“China is the largest global TV market, and this panel inventory adjustment and stagnant sell-through have caused TV makers in China to become more conservative in their panel purchases,” said Nick Jiang, senior display analyst for IHS. “This conservatism is a major shift from the aggressive market in 2014, which has caused display makers to face over-supply and may induce panel prices to drop further at the end of this year.”

In the first half of 2015, panel makers shipped 29.4 million TV panels to Chinese manufacturers, leading to a strong 15 percent year-over-year growth. However, in the third quarter (Q3), Chinese TV makers drastically reduced planned panel purchases. Manufacturers shipped 15 million TV panels to China in Q3 2015, which is a 6 percent year-over-year decline, with additional declines expected in Q4 2015. According to the latest TV Display Supply Chain Tracker - China from IHS Technology, the annual purchase of China’s top six leading TV makers will reach just 59.3 million this year, a year-over-year decline of less than 1 percent since 2014.

The leading panel suppliers for the Chinese market in Q3 2015 are: LG Display at 22 percent, ChinaStar at 20 percent, Innolux at 16 percent, Samsung Display at 15 percent, AUO at 13 percent and BOE at 10 percent. “These panel makers must now adjust their capacity and production strategy, which will make the market down-turn more severe by year’s end,” Jiang said.

At the end of August 2015, the average inventory level at the top six Chinese TV brands reached 6.5 weeks, a month-over-month increase of one inventory week. To prepare for National Day, China’s top six TV makers bought more panels in August; however, due to weakening demand in the Chinese domestic market, inventory levels remained high in September. Amid lingering concerns over a panel supply shortage, Chinese set makers’ inventory levels returned to normal at the end of 2014, and this strong appetite for TV panels lifted overall panel purchases in the first quarter (Q1) of 2015.

“China’s top six TV makers’ purchases in Q2 2015 exceeded our expectations,” Jiang said, “but with the advent of the off-season, inventory is also on the rise, so there is pressure for further panel price reductions in Q3 and Q4 of this year.”

About IHS

IHS is the leading source of insight, analytics and expertise in critical areas that shape today’s business landscape. Businesses and governments in more than 150 countries around the globe rely on the comprehensive content, expert independent analysis and flexible delivery methods of IHS to make high-impact decisions and develop strategies with speed and confidence. IHS has been in business since 1959 and became a publicly traded company on the New York Stock Exchange in 2005. Headquartered in Englewood, Colorado, USA, IHS is committed to sustainable, profitable growth and employs about 8,800 people in 32 countries around the world.

Share on:

Testimonial

"The I-Connect007 team is outstanding—kind, responsive, and a true marketing partner. Their design team created fresh, eye-catching ads, and their editorial support polished our content to let our brand shine. Thank you all! "

Sweeney Ng - CEE PCBSuggested Items

LPKF Strengthens Structural Resilience: 'North Star' Initiative Aims to Secure Long-term Profitability

09/16/2025 | LPKFLPKF Laser & Electronics SE has launched the "North Star" initiative, a far-reaching package of measures designed to strengthen the company's long-term profitability.

The Marketing Minute: Cracking the Code of Technical Marketing

09/17/2025 | Brittany Martin -- Column: The Marketing MinuteMarketing is never a one-size-fits-all endeavor, but the challenges are magnified for highly technical industries like electronics. Products and processes are complex, audiences are diverse, and the stakes are high, especially when your customers are engineers, decision-makers, and global partners who depend on your expertise.

Beyond the Board: What Companies Need to Know Before Entering the MilAero PCB Market

09/16/2025 | Jesse Vaughan -- Column: Beyond the BoardThe MilAero electronics supply chain offers opportunities for manufacturers that are both prestigious and strategically important. Serving prime contractors and Tier-1 suppliers can mean long-term program stability and the satisfaction of contributing to national security. At the same time, this sector is unlike commercial electronics in almost every respect. Success requires more than technical capabilities, it requires patience, preparation, attention to detail, and a clear understanding of how the business model differs.

Global Interposer Market to Surge Nearly Fivefold by 2034

09/15/2025 | I-Connect007 Editorial TeamRevenue for the global interposer market is projected to climb from $471 million in 2025 to more than $2.3 billion by 2034, according to a new report from Business Research Insights. The growth represents a CAGR of nearly 20 percent over the forecast period.

Indium Promotes Huang to Senior Manager, Marketing Communications

08/28/2025 | Indium CorporationWith its commitment to innovation and growth through employee development, Indium Corporation announces the promotion of Jingya Huang to Senior Manager, Marketing Communications, to continue to lead the company’s branding and promotional efforts.