The Chemical Connection: Onshoring PCB Production—Daunting but Certainly Possible

The Chemical Connection: Onshoring PCB Production—Daunting but Certainly Possible It’s Only Common Sense: The Phone Is Still Mightier Than the Keyboard

It’s Only Common Sense: The Phone Is Still Mightier Than the Keyboard

Asia/Pacific Semiconductor Fabless Market Size Decline 6.5% YoY in 2022, Expected Steady Growth in 2024

May 17, 2023 | IDCEstimated reading time: 2 minutes

According to the IDC Worldwide Semiconductor Technology Supply Chain Intelligence: IDMs, Fabless, Foundry, OSAT and Materials, factors including the Ukraine-Russia war, Chinese lockdowns, high inflationary pressures, and demand fluctuations resulted in the Asia/Pacific region’s semiconductor fabless market losing growth momentum in 2022 and an end to the trend of rising Integrated Circuit (IC) prices. The region’s semiconductor fabless market size in 2022 was US$78.5 billion, a decline of 6.5% compared to 2021 which marks the first year-on-year negative growth performance since the onset of the pandemic.

The global semiconductor industry experienced a sharp decline in 2022 after seeing growth in 2020 and 2021. Demand for consumer electronics including smartphones, laptops, tablets, TVs, and monitors plummeted while supply chain inventory levels increased. Short-term supply began exceeding demand, forcing companies to slow down the pace of expansion.

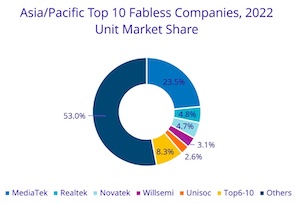

“The annual growth rate of the top 10 companies in Asia/Pacific was -5.1%, which was better than the overall market performance. From the perspective of regional momentum, Taiwan leads with 73% market share, while China and South Korea holds 22% and 5% market share respectively. Having the highest market share, Taiwan is considered to have a wide and deep influence on the region’s fabless market,” said Galen Zeng, Senior Research Manager, Semiconductor Research, IDC Asia/Pacific.

Among the top 10 semiconductor technology vendors are Taiwan’s MediaTek, Realtek, Novatek, and Himax; China’s Willsemi, Unisoc, HiSilicon, GigaDevice, and Bitmain; and South Korea’s LX Semicon. MediaTek plays an influential role with a market share of nearly 50% among the top 10 companies. The growth of MediaTek played a leading role by helping make up for the shortfalls of other Taiwanese firms, resulting in a 2% increase in Taiwan’s semiconductor fabless market share in the region compared to 2021. Chinese companies were affected by the overall unfavorable environment in China and saw their market share decline by 2%, while South Korea’s market share did not experience any major changes.

As for the outlook for 2023, although products such as display driver ICs and touch and display driver ICs were the first to enter a down cycle, these are now seeing the light of day with several products starting to see urgent orders and the need for inventory replenishment. The market demand for most semiconductor ICs remains depressed and the market size outlook remains sluggish. During the high base period in the first half of 2022, it was anticipated that the region’s fabless market size in the first half of 2023 would decrease by over 20% year-on-year, supply chains would continue to actively control inventory, and fabless companies would maintain low wafer production volumes at foundries. During the second half of 2023, it is expected that inventory will return to a healthy level, and that demand will also slowly recover. IDC forecasts that the Asia/Pacific region’s semiconductor fabless market size will decline by 19.1% year-on-year in 2023. It also predicts that it will progressively show stable and steady growth in 2024 as companies gradually shift products to applications including AI, high-performance computing, servers, data centers, automotive electronics, and industrial electronics to diversify operational risks.

This IDC research, Worldwide Semiconductor Technology Supply Chain Intelligence: IDMs, Fabless, Foundry, OSAT and Materials, provides holistic analysis of the worldwide semiconductor supply chain industry. The program delivers comprehensive insights across supply chain including materials, Fabless, OSAT, and semiconductor equipment. It covers the analysis of market dynamics, market competition, and key vendors' activities and the strategy plans to understand the key trends and factors impacting the market as it transitions to the new world of digital competition under geopolitical impact across countries and companies.

Share on:

Testimonial

"Our marketing partnership with I-Connect007 is already delivering. Just a day after our press release went live, we received a direct inquiry about our updated products!"

Rachael Temple - AlltematedSuggested Items

The Marketing Minute: Marketing With Layers

10/15/2025 | Brittany Martin -- Column: The Marketing MinuteMarketing to a technical audience is like crafting a multilayer board: Each layer serves a purpose, from the surface story to the buried detail that keeps everything connected. At I-Connect007, we’ve learned that the best marketing campaigns aren’t built linearly; they’re layered. A campaign might start with a highly technical resource, such as an in-depth article, a white paper, or a podcast featuring an engineer delving into the details of a process. That’s the foundation, the substance that earns credibility.

ICT Symposium Review: Sustainability and the Circular Economy

10/09/2025 | Pete Starkey, I-Connect007It was pleasant autumnal weather as we made our way once again to Meriden, the nominal centre of England, for the 2025 Annual Symposium of the Institute of Circuit Technology. Delegates were welcomed by technical director Emma Hudson who introduced and moderated a skilfully coordinated programme, focused on the highly relevant theme of sustainability.

Circular Packaging Market to Reach $98.0 Billion by 2035

10/08/2025 | Fact.MRThe market's journey from USD 45.8 billion in 2025 to USD 98.0 billion by 2035 represents substantial growth, the market will rise at a CAGR of 7.9% demonstrating the accelerating adoption of sustainable packaging systems and circular economy solutions across food & beverage, personal care, and e-commerce sectors.

It’s Only Common Sense: Stop Whining About the Market—Outwork It

10/06/2025 | Dan Beaulieu -- Column: It's Only Common SenseWhenever the market hiccups or the industry cycle dips, I hear the same tired chorus: “The market is down. Customers aren’t buying. What can we do? We just have to wait it out.” Nonsense. If you think that by showing up, opening your doors, and waiting for the economy to smile kindly upon you, that success will follow, you are in the wrong business. Worse yet, you’re living in the wrong mindset. Most people don’t want to hear the truth that winners find business in down cycles. Losers blame the economy.

Schweizer Ends Staff Restructuring Measures and Short-Time Working at the Schramberg Site

10/01/2025 | Schweizer Electronic AGSchweizer Electronic AG has implemented comprehensive measures to adjust its cost and personnel structure at its Schramberg site due to strong market fluctuations in the automotive and industrial electronics sector. Thanks to the successful restructuring, short-time working can now be ended with immediate effect. A stable order situation is expected for the fourth quarter, with signs of growth momentum returning in 2026.