Material Insight: The Dielectric Constant of PCB Materials

Material Insight: The Dielectric Constant of PCB Materials American Made Advocacy: What About the Rest of the Technology Stack?

American Made Advocacy: What About the Rest of the Technology Stack? It’s Only Common Sense: Great Ideas From John Mitchell’s Book on Hiring Habits

It’s Only Common Sense: Great Ideas From John Mitchell’s Book on Hiring HabitsGlobal Smartphone Volume Reached New High with Sequential Growth at 10.4% in Q3

October 19, 2016 | TrendForceEstimated reading time: 4 minutes

Global market research firm TrendForce reports the production volume of smartphones worldwide totaled around 350 million units in the third quarter of 2016. This figure represents a sequential quarterly increase of 10.4%, which is a new high for the year.

Global smartphone shipments has steadily picked up since the second quarter. Chinese brands in particular has maintained strong shipment growth and provided the growth momentum for the overall smartphone production volume in the third quarter.

“The combined production volume from Chinese brands reached 168 million units in the third quarter, translating to a sequential quarterly increase of 18%,” said TrendForce smartphone analyst Avril Wu. “As in the previous quarter, the combined production volume of Chinese brands exceeded the combined production volume of leading brands Apple and Samsung. The role of Chinese brands as the main driving force of global smartphone shipments is therefore firmly established.”

Apple rests its hopes on the expansion of iPhone 7 shipments in the fourth quarter while Samsung deals with the fallout from Note 7’s battery defect.

Apple’s iPhone production volume in the third quarter totaled 45 million units, down 5.3% from the second quarter. Though Apple began shipping iPhone 7 during this period, shipments were limited in amount and not enough to turn around the brand’s performance.

“Much of the iPhone 7 production for 2016 will be taking place during the fourth quarter,” Wu noted. “Furthermore, TrendForce has revised upward the production volume of iPhone 7 Plus on account of Samsung discontinuing Galaxy Note 7. Hence, iPhone production volume is expected to jump significantly towards the end of 2016.”

Samsung’s smartphone production volume in the third quarter was around 78 million units, registering a minor growth of 1.3% versus the second quarter. Samsung’s production volume figure was at a similarly high level as a year ago mainly due to the popularity of its Galaxy J series. Having impressive features while being economically priced, the models in the J series have helped sustain Samsung’s overall shipments. In addition to the J series, Samsung also posted strong sales of Galaxy S7 and S7 Edge.

On the other hand, the discontinuation of Galaxy Note 7 will impact Samsung’s performances going into the fourth quarter. The self-combusting battery problem forced Samsung to halt the production of its latest flagship smartphone almost immediately after the device hit the market. Though the event has tarnished Samsung’s reputation among consumers, how much effect it will have on the brand’s smartphone shipments remains to be seen.

LG finds that the sales of its G5 smartphone, which was heavily promoted in the first half of 2016, have been below expectations. However, the brand’s other flagship device V20 has done fairly well in the market. The production volume of LG smartphones came to around 20 million units in the third quarter, growing by 17.6% sequentially. Furthermore, LG has received additional orders for the large-size V20 from telecom companies since the Note 7 incident, thus making the brand another beneficiary of Samsung’s misfortune. By securing good relations with the clients in the telecom industry, LG can anticipate a significant increase in its fourth-quarter smartphone shipments.

Huawei, OPPO and Vivo posted strong sequential growth rates of above 10% for their third-quarter smartphone production

In the third quarter, Huawei’s smartphone production volume grew about 10.3% sequentially to 32 million units. The sales of Huawei’s dual-camera flagship device P9 were weaker than expected because of increasing competition from other Chinese brands, but Huawei’s production volume kept climbing on the back of peak season demand.

Both OPPO and Vivo again significantly raised their production volumes in the third quarter and managed to post sequential quarterly growths surpassing 20%, at 20.3% and 23% respectively. These two Chinese brands are considered to have made the most gains in the 2016 smartphone market.

“OPPO and Vivo mainly focus on their domestic market and are especially good at developing sales channels in the more remote urban communities within the country,” said Wu. “They have already established themselves in China’s third- and fourth-tier cities and are expanding into fifth- and sixth-tier cities in the second half of 2016. OPPO and Vivo will maintain strong growth this year as their strategies have paid off.”

OPPO has followed up the success of its flagship smartphone R9 with the release of R9s, which features an upgraded camera. Vivo also has a new flagship device in the offering for the second half of the year in order to continue capturing consumers’ attention.

Lenovo’s smartphone production volume for the third quarter also posted a sequential increase of over 20%, which is the best quarterly result for the brand this year. However, Lenovo can expect fierce price competition in mid-range and low-end segments of the smartphone market in the fourth quarter. Additionally, Lenovo has not been successful in boosting the sales of its Phab 2 Pro, a smartphone that features Google’s augmented reality platform Tango. Hence, the brand may see its production volume drop in the fourth quarter.

Xiaomi’s smartphone production volume was on a decline in the third quarter despite the influence of the peak season demand, falling by around 7% compared with the prior quarter. Xiaomi has not come up with a standout product this year and is being overwhelmed by its domestic competitors.

Many branded Android phone makers are seeking fill the demand gap created by the discontinuation of Galaxy Note 7, and there are speculations as to whether Google can now make a strong push into the smartphone market with its Pixel series. However, Wu pointed out that Google is unable to significantly expand the production of Pixel and Pixel XL because of the current supply shortage in the AMOLED panel market. TrendForce estimates the production volume of Pixel smartphones for 2016 to be less than 2 million units.

Share on:

Suggested Items

SPEA Expands in Southeast Asia with New Subsidiary in Thailand

05/17/2024 | SPEASPEA, a global leader in automatic test equipment for the manufacturing of semiconductor, microelectronic and electronic devices, today announced the opening of its new subsidiary in Thailand. This expansion marks a significant step forward in SPEA's commitment to serving the growing Southeast Asian microchip and electronics market with leading-edge manufacturing machinery and equipment.

PCB Market Size to Grow by $29.06B from 2024-2028

05/17/2024 | PRNewswireThe global printed circuit board (PCB) market size is estimated to grow by USD 29.06 bn from 2024-2028, according to Technavio. The market is estimated to grow at a CAGR of over 6.6% during the forecast period.

AT&S 2024/25 on Growth Course Again

05/17/2024 | AT&SAT&S operated in a challenging market environment in the financial year 2023/24. After a strong second quarter, demand was relatively weak again in some market segments in the second half of the financial year.

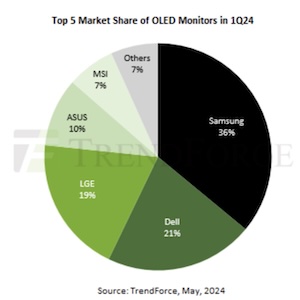

Shipments of OLED Monitors Hit 200,000 Units in 1Q24, Annual Forecast to Reach 1.34 Million

05/17/2024 | TrendForceTrendForce’s latest report reveals a robust start to 2024 for OLED monitors, with shipments reaching approximately 200,000 units in the first quarter—marking a YoY growth of 121%.

Magnachip Celebrates the Grand Opening of Magnachip Technology Company in China

05/16/2024 | MagnachipMagnachip Semiconductor Corporation celebrated the opening ceremony of Magnachip Technology Company, Ltd. (MTC) yesterday at its headquarters located in Hefei, China. MTC is a subsidiary of Magnachip, established on December 20, 2023, to expand the Company’s display driver IC and power IC businesses in China.