It’s Only Common Sense: Nice Guys Really Can Finish First

It’s Only Common Sense: Nice Guys Really Can Finish First The Right Approach: I Hear the Train A Comin'

The Right Approach: I Hear the Train A Comin' Marcy's Musings: The Growing Industry

Marcy's Musings: The Growing IndustryStrong Demand for Larger Sizes Will Expand This Year’s TV Panel Shipment Area by 7.3%

March 30, 2017 | TrendForceEstimated reading time: 2 minutes

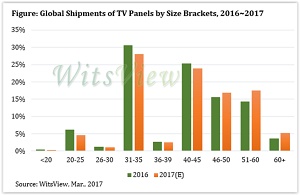

WitsView estimates that worldwide shipments of LCD TV panels for 2017 will total 255.6 million units, down 1.8% in unit volume from 2016. This year’s increase in the average size of TV panels, however, will lead to an annual growth of 7.3% in total shipment area.

WitsView points out that panel makers have shifted towards larger sizes for the TV market because of two major factors. First, the market supply of 55-inch TV panels are plentiful, so panel makers need to move up the size brackets to differentiate themselves. Second, high panel prices are squeezing margins of TV sets. International TV brands therefore switched to promoting larger and high-end models (e.g. 65- and 75-inch TV sets) that can generate more profits.

Due to the above factors, TV panels sized larger than 60 inches are projected to account for 5.2% of the total TV panel shipments for 2017, an increase from last year’s share of 3.6%. Moreover, the average size of TV panels will expand by 2 inches this year to 45.5 inches.

South Korean manufacturers will account for over 70% of the global shipments of 75-inch panels this year, while Taiwanese counterparts will have a share of less than 30%

WitsView estimates that 75-inch TV panels will reach 1.5 million units in 2017, more than doubling last year’s volume of 0.7 million units with the annual growth rate reaching 114%. Currently, there are just four suppliers of 75-inch panels from South Korea and Taiwan. Major South Korean panel makers have the advantage of being supported by their respective group companies are expected to take more than 70% of the global shipment share for this year. Taiwanese panel industry is trying to catch up in the production of 75-inch panels but its share in the total shipments is projected to be under 30%.

Nearly 60% of the total 65-inch panel shipments will come from South Korea manufacturers this year, while Taiwanese counterparts will have a share of almost 40%

South Korean and Taiwanese panel makers are also increasing the share of the 65-inch segment in their product mixes due to the general upswing in prices. WitsView estimates that total shipments of 65-inch TV panels for this first quarter will enjoy a leaping year-on-year growth rate of 104%, from 1.1 million to 2.2 million units. The panel industry is expected to take on additional production capacity for the 65-inch segment, and annual shipments are projected to reach 11 million units, up 45% from last year’s total of 7.6 million units.

WitsView notes that 65-inch panel shipments from Samsung Display (SDC) during this year will be mainly going to its group company Samsung for strategic reasons. On the whole, South Korean panel makers are expected to expand their global shipment share of 65-inch panels to nearly 60% this year, whereas Taiwanese competitors are going to account for almost 40%. Around just 2% of the total 65-inch panel shipments for 2017 will come from Chinese manufacturers. Chinese panel companies will not begin to significantly raise their 65-inch panel production and catch up to South Korean and Taiwanese competitors until 2018, when their Gen-10.5 fabs are ready to operate.

Share on:

Suggested Items

SCHWEIZER Confirms Group Figures and Outlook for 2024

04/29/2024 | SCHWEIZERSCHWEIZER announces the publication of the annual report for 2023 and confirms the preliminary figures. The SCHWEIZER-Group (according to IFRS) generated sales of EUR 139.4 million in 2023 (previous year: EUR 131.0 million).

NCAB Group Posts Interim Report Q1 2024

04/26/2024 | NCAB GroupNet sales decreased by 17% to SEK 950.6 million (1,146.4). Compared with the year-earlier period, sales were affected bylower prices and continued inventory adjustments by customers. In USD, net sales decreased 17%. For comparable units, net sales decreased 24% in both SEK and USD.

Rogers Corporation Reports Q1 2024 Results

04/26/2024 | Rogers CorporationNet sales of $213.4 million increased 4.3% versus the prior quarter resulting from higher sales in the AES and EMS business units. AES net sales increased by 4.1% primarily related to higher aerospace and defense (A&D), wireless infrastructure, industrial and renewable energy sales, partially offset by lower EV/HEV and ADAS sales. EMS net sales increased by 2.8% primarily from higher general industrial, A&D and EV/HEV sales, partially offset by seasonally lower portable electronics sales.

NOTE Releases Interim Report for January-March 2024.

04/23/2024 | NOTENOTE has announced its interim report for January-March 2024.

Mycronic Releases Interim Report January–March 2024

04/18/2024 | MycronicNet sales increased 39 percent to SEK 1,692 (1,219) million. Based on constant exchange rates, net sales increased 42 percent.