The Chemical Connection: Reducing Etch System Water Usage, Part 2

The Chemical Connection: Reducing Etch System Water Usage, Part 2 It’s Only Common Sense: Nice Guys Really Can Finish First

It’s Only Common Sense: Nice Guys Really Can Finish First The Right Approach: I Hear the Train A Comin'

The Right Approach: I Hear the Train A Comin'Thin Film Electronics and PV Cells Manufacture Rates on the Rise

April 24, 2017 | Transparency Market ResearchEstimated reading time: 2 minutes

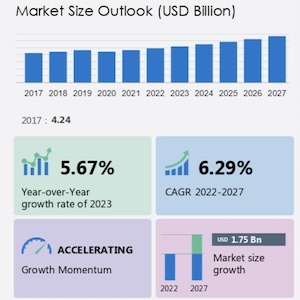

The global thin and ultra-thin films market is a relatively consolidated market, as per the observations of market intelligence firm Transparency Market Research. The players that led the market in 2015 – E.I. du Pont, Kaneka Corporation, and Corning Incorporated – held a collective share of 35.5%. The leading players in the global thin and ultra-thin films market are expected to continue in their positions, owing to their already enriched product offerings.

According to the recently released research report, the global thin and ultra-thin films market was valued at $32.78 billion in 2015. The market is expected to expand at a CAGR of 15.1% within a forecast period from 2016 to 2024, and is eventually expected to reach $115.41 billion at the end of 2024.

Defense and Aerospace Industries to Accelerate Demand for Thin and Ultra-thin Films

The global thin and ultra-thin films market is currently being driven by the rising favor gained by semiconductor miniaturization in the electronics industry. The growing usage of thin and ultra-thin films in electronics and semiconductors, due to the various advantages that they hold, is likely to push the growth of the global thin and ultra-thin films market. Simultaneously, the global thin and ultra-thin films market is being driven by the thriving aerospace and defense sectors through their increased interest in using the films as they offer enhanced efficiency, power, speed, while making an electronic device lighter in weight.

The demand generated by the global thin and ultra-thin films market is expected to receive a further shot in the arm through the increasing adoption of solar energy, as thin and ultra-thin films are widely used for the manufacture of photovoltaic cells. The stringent rules implemented by environmental organizations such as Greenpeace, EPA, and Department of Energy Resources to reduce carbon footprint are expected to fuel the demand for thin-film PVs in the coming years, thereby enhancing the scope of growth for players in the global thin and ultra-thin films market.

Asia Pacific Thin and Ultra-Thin Films Market to Rise at a Leading Rate

In terms of geography, the global thin and ultra-thin films market can be divided into North America, Asia Pacific, Europe, the MEA, and Latin America. Asia Pacific is expected to remain the leader in the global market over the coming years. The thriving activities in semiconductor manufacturing and the improving industrial infrastructure are expected to drive the thin and ultra-thin films market for this region. By the end of 2024, Asia Pacific is poised to account for a share of 24.1% in the global thin and ultra-thin films market.

The end users for the global thin and ultra-thin films market include the manufacturers of thin-film devices, such as electronics, batteries, and PV. The segment for thin-film electronics was leading the global thin and ultra-thin films market till 2015 and is expected to continue leading it in the coming years. By the end of 2024, this segment is expected to acquire a share of 64.9% in the global thin and ultra-thin films market.

Complicated Installation Discourages Users from Using Thin and Ultra-thin Films

The global thin and ultra-thin films market faces a tough restraint that is likely to act as a hurdle in the coming years. The current challenge for the global thin and ultra-thin films market is the poor conversion efficiency of thin film solar cells. Furthermore, their complex construction structure is also dissuading users from investing in these films over the long run. The sophisticated installation skills required for flexible thin film solar cells make are not easily available and thus not viable.

Share on:

Suggested Items

I-Connect007 Editor’s Choice: Five Must-Reads for the Week

05/03/2024 | Nolan Johnson, I-Connect007This week’s most important news is strategic—and telling. When one puts together the IPC industry reports, alongside reports from SEMI, USPAE, and EIPC, we simply had to include the recent conversation with Shawn DuBravac and Tom Kastner. On the design side, check out the latest “On The Line With…” podcast featuring Brad Griffin from Cadence Design Systems, discussing SI and PI in the realm of intelligent system design.

IMI Welcomes New CEO

05/03/2024 | IMIIntegrated Micro-Electronics, Inc. (IMI),The IMI Board of Directors announced, in a disclosure dated April 25, 2024, the appointment of Louis Sylvester Hughes, Chief Executive Officer (CEO).

Electronics Industry Sentiment Rose in April, Hitting New High

05/02/2024 | IPCApril 2024 marked the third consecutive month of sentiment growth among electronics manufacturers. When asked if they expected labor costs for hourly workers to rise over the next month, manufacturers in the United States, Mexico, and Europe predicted a five percent increase, while manufacturers in Asia predicted a slightly lower four percent increase.

iNEMI Names Grace O'Malley CTO

05/02/2024 | iNEMIThe Board of Directors of the International Electronics Manufacturing Initiative (iNEMI) has named Grace O'Malley Chief Technical Officer (CTO).

ZESTRON Academy Launches 2024 Advanced Packaging & Power Electronics Webinar Series

05/01/2024 | ZESTRONZESTRON, the leading global provider of high-precision cleaning products, services, and training solutions in the electronics manufacturing and semiconductor industries, proudly announces the launch of its highly anticipated webinar series on Advanced Packaging & Power Electronics, a webinar series on the latest innovations, cleaning, and corrosion challenges.