The Chemical Connection: Reducing Etch System Water Usage, Part 2

The Chemical Connection: Reducing Etch System Water Usage, Part 2 It’s Only Common Sense: Nice Guys Really Can Finish First

It’s Only Common Sense: Nice Guys Really Can Finish First The Right Approach: I Hear the Train A Comin'

The Right Approach: I Hear the Train A Comin'Adversarial Relationship of the DRAM User and Producer Continues

September 14, 2017 | IC InsightsEstimated reading time: 2 minutes

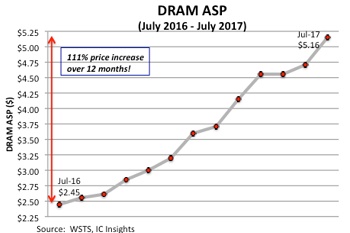

Historically, the DRAM market has been the most volatile of the major IC product segments. Figure 1 reinforces that statement by showing that the average selling price (ASP) for DRAM has more than doubled in just one year. In fact, the September Update to The McClean Report will discuss IC Insights’ forecast that the 2017 price per bit of DRAM will register a greater than 40% jump, its largest annual increase ever.

Just one year ago, DRAM buyers took full advantage of the oversupply (excess capacity) portion of the cycle and negotiated the lowest price possible with the DRAM manufacturers, regardless of whether the DRAM suppliers lost money on the deal. Now, with tight capacity in the market, DRAM suppliers are getting their “payback” and charging whatever the market will bear, regardless of whether the price increases hurt the users’ electronic system sales or causes it to lose money.

The three remaining major DRAM suppliers—Samsung, SK Hynix, and Micron—are each currently enjoying record profits from their memory sales. For example, Micron reported net income of $1.65 billion on $5.57 billion in sales—a 30% profit margin—in its fiscal 3Q17 (ending in May 2017). In contrast, the company lost $170 million in its fiscal 4Q16 (ending August 2016). A similar turnaround has occurred at SK Hynix. In 2Q17, SK Hynix had a net profit of $2.19 billion on sales of $5.94 billion—a 37% profit margin. In contrast, SK Hynix had a net profit of only $246 million on $3.39 billion in sales one year ago in 2Q16.

Previously, when DRAM capacity was tight and suppliers were enjoying record profits, one or more suppliers eventually would break rank and begin adding additional DRAM capacity to capture additional sales and marketshare. At that time, there were six, eight, or a dozen DRAM suppliers. If the supplier was equipping an existing fab shell, new capacity could be brought on-line relatively quickly (i.e., six months). A greenfield wafer fab—one constructed on a new site—took about two years to reach high-volume production. Will the same situation play out with only three DRAM suppliers left to serve the market?

Recently, Micron stated that it does not intend to add DRAM wafer capacity in the foreseeable future. Instead, it will attempt to increase its DRAM output by reducing feature size that, in turn, reduces die size. Eventually, as the company moves down the learning curve, it will be able to ship an increasing number of good die per wafer. However, SK Hynix, in its 2Q17 financial analyst conference call, stated that it plans to begin adding DRAM wafer capacity since it is not able to meet increasing demand by technology advancements alone. Samsung has been less forthcoming in its plans for future DRAM production capacity.

Although Samsung and Micron may tolerate SK Hynix’s DRAM expansion efforts for a short while, IC Insights believes that both companies will eventually step up and add DRAM wafer start capacity to protect their marketshare—and DRAM ASPs will begin to fall. As the old saying goes, it only takes two companies to engage in a price war—and there are still three major DRAM suppliers left.

Share on:

Suggested Items

IMI Welcomes New CEO

05/03/2024 | IMIIntegrated Micro-Electronics, Inc. (IMI),The IMI Board of Directors announced, in a disclosure dated April 25, 2024, the appointment of Louis Sylvester Hughes, Chief Executive Officer (CEO).

Benchmark Reports Q1 2024 Results

05/03/2024 | PRNewswireRevenue decreased quarter over quarter and year over year primarily due to decreases in Medical, Advanced Computing and Next-Generation Communication sales, which were partially offset by an increase in Complex Industrials sales quarter-over-quarter and increases in Semi-Cap and A&D sales year-over-year.

LQDX Divests Aluminum Soldering Business - Mina™ - to Taiyo America Inc.

05/02/2024 | PRNewswireLQDX, formerly known as Averatek Corp., developer of high-performance materials for advanced semiconductor manufacturing, today announced that it has divested its aluminum soldering business – known as MinaTM – to Taiyo America Inc., a global market leader in advanced electronic materials.

TTM Technologies Reports First Quarter 2024 Results

05/02/2024 | TTM TechnologiesTTM Technologies, Inc., a leading global manufacturer of technology solutions including mission systems, radio frequency components and RF microwave/microelectronic assemblies, quick-turn and technologically advanced printed circuit boards , reported results for the first quarter 2024, which ended on April 1, 2024.

GPV’s Q1 2024 Interim Financial Report Shows Strong Navigation in Uncertain Times

05/01/2024 | GPVDanish-based GPV recorded an expected drop in sales to DKK 2.3 billion for the first quarter of 2024. The decline also affected the operating profit, which was DKK 155 million compared to DKK 179 million in the same quarter last year, although the EBITDA margin was maintained. In general, demand has been softer in 2024, but GPV continues to invest for the long-term and expects the trend to turn in the second half of 2024.