It’s Only Common Sense: Would You Work at Your Own Company?

It’s Only Common Sense: Would You Work at Your Own Company? The Chemical Connection: Reducing Etch System Water Usage, Part 2

The Chemical Connection: Reducing Etch System Water Usage, Part 2 The Right Approach: I Hear the Train A Comin'

The Right Approach: I Hear the Train A Comin'Growth of AMOLED Display Manufacturing Capacity Slowing in South Korea While Accelerating in China

March 12, 2018 | IHS MarkitEstimated reading time: 3 minutes

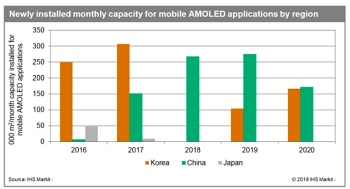

After two years of unprecedented capacity expansion, South Korean flat panel display (FPD) manufacturers will essentially halt new active-matrix organic light-emitting diode (AMOLED) panel factory construction for mobile applications in 2018. At the same time, their Chinese rivals are continuing to build new factories as fast as they can, according to IHS Markit.

Since the third quarter of 2017, South Korean FPD makers have been reevaluating the pace of their AMOLED expansion strategies. By the end of January 2018, with demand falling short of expectations and suffering from low factory utilization rates, they delayed all major capacity expansion plans, including several cases of deferring the ramp of equipment already installed.

As the market matures, concern is cumulating that smartphone sales may not continue to increase at rates as high as previously hoped for. With display and smartphone performance specifications already excellent, the replacement cycle is lengthening. Furthermore, adoption of high-end flexible AMOLED panels in a wider range of models is being restricted by high prices that are still about two times those of equivalently specified liquid crystal displays (LCDs).

“After doubling AMOLED capacity for mobile applications in the past two years, a slowdown in facility investment in South Korea is not surprising,” said Charles Annis, senior director at IHS Markit. “Even so, the freezing of all new investments and multiple mass production schedules suggests recognition that continued capacity additions will outpace the market’s ability to absorb them.”

Despite market concerns and changing investment plans in South Korea, Chinese FPD makers are still pushing ahead with their own aggressive new AMOLED factory plans, at least for now. According to the AMOLED and LCD Supply Demand & Equipment Tracker by IHS Markit, ramped Chinese AMOLED capacity will rise from just 228,000 square meters per year in 2016 to 8.3 million square meters in 2020, at a compound annual growth rate of 145%.

Chinese makers are not immune to challenges in the smartphone and flexible AMOLED market, and in most cases, they have not yet proven their ability to manufacture premium flexible AMOLED panels at high volume. Regardless, with strong financial backing from local governments, most projects are still moving forward as planned, and will likely continue until credit begins to tighten.

South Korean panel makers are carefully watching how fast the market for AMOLED displays is increasing and are prudently adjusting capacity plans. Chinese makers have less flexibility and less motivation to change strategies due to contracts with local governments in multiple locations across the country.

“The rationalization of how fast the mobile AMOLED display market can grow does raise questions,” Annis said. “What will drive a renewal of investment in South Korea and how will Chinese FPD makers fill their new fabs?”

“Reduced panel prices will enable AMOLEDs to compete more on performance and form factor advantages over LCDs, while new applications, particularly foldable displays, will increase average panel size. Both of these trends have the potential to significantly drive future demand; however, in the shorter term, they remain elusive targets due to high costs and remaining technical barriers,” Annis said.

The AMOLED and LCD Supply Demand & Equipment Tracker by IHS Markit covers all key metrics used to evaluate supply, demand and capital spending for all major flat panel display technologies and applications.

About IHS Markit

IHS Markit is a world leader in critical information, analytics and solutions for the major industries and markets that drive economies worldwide. The company delivers next-generation information, analytics and solutions to customers in business, finance and government, improving their operational efficiency and providing deep insights that lead to well-informed, confident decisions. IHS Markit has more than 50,000 business and government customers, including 80 percent of the Fortune Global 500 and the world’s leading financial institutions. Headquartered in London, IHS Markit is committed to sustainable, profitable growth.

Share on:

Suggested Items

IDTechEx Discusses Low-Loss Materials: The Enabler of Future Connected Vehicles?

05/06/2024 | IDTechExFuture connected vehicles will offer future drivers a safer, smoother, and more convenient driving experience. Not only will drivers get access to more navigation and entertainment options, but they will also gain access to safety technologies that will potentially reduce accidents, improve congestion, and reduce emissions globally by allowing vehicle safety systems to communicate with each other and with city traffic infrastructure.

HBM Prices to Increase by 5–10% in 2025, Accounting for Over 30% of Total DRAM Value

05/06/2024 | TrendForceAvril Wu, TrendForce Senior Research Vice President, reports that the HBM market is poised for robust growth, driven by significant pricing premiums and increased capacity needs for AI chips.

Tablet Shipments Show Signs of Recovery in Q1 2024

05/06/2024 | IDCAfter more than two years of decline, worldwide tablet shipments posted modest year-over-year growth of 0.5% in the first quarter of 2024 (1Q24), totaling 30.8 million units, according to preliminary data from the International Data Corporation (IDC) Worldwide Quarterly Personal Computing Device Tracker.

Industrial PC Market Size to Record $1.75 Billion Growth from 2023-2027

05/03/2024 | PRNewswireThe global industrial pc market size is estimated to grow by USD 1.75 billion from 2023 to 2027, according to Technavio. This growth is expected to occur at a Compound Annual Growth Rate (CAGR) of almost 6.29% during the forecast period.

Real Time with… IPC APEX EXPO 2024: Direct Imaging Equipment and Quad-wave DLP Light Engine Technology

05/03/2024 | Real Time with...IPC APEX EXPOGuest Editor Kelly Dack and MivaTek's Brendan Hogan delve into the company's innovative technologies, including direct imaging equipment and quad-wave DLP light engine technology. They highlight the benefits of direct imaging, compensation, and DART technology.