It’s Only Common Sense: Would You Join Your Own Company?

It’s Only Common Sense: Would You Join Your Own Company? The Chemical Connection: Reducing Etch System Water Usage, Part 2

The Chemical Connection: Reducing Etch System Water Usage, Part 2 The Right Approach: I Hear the Train A Comin'

The Right Approach: I Hear the Train A Comin'Oppo Overtakes Samsung in Thailand in 4Q18 as Market Shrinks 13.6%

February 13, 2019 | CanalysEstimated reading time: 2 minutes

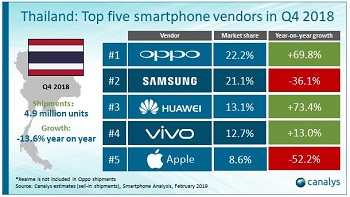

Thailand, the second largest smartphone market in Southeast Asia, suffered another fall in shipments in the fourth quarter of 2018, after a steep decline in Q3 2018. 4.9 million units shipped in Q4 2018, a 13.6% fall year on year, which caused full-year 2018 sell-in to decline 8.6% to 19.2 million units. Oppo overtook Samsung for the first time to become the top vendor, shipping nearly 1.1 million smartphones to take a 22.2% market share. Huawei and Vivo are closing in on the top two at 13.1% and 12.7%, while Apple, in fifth place, reported its lowest Q4 market share in the country.

Competition has been intense, as several new players, such as Xiaomi, Honor, Lava and Wiko, have aggressively entered the market in the past two years. Consumer demand for smartphones, however, is not growing as the Thai market matures. The smartphone replacement cycle is lengthening, despite mobile operators offering attractive discounts to stimulate demand. And millions of feature phone users remain in rural areas, not planning to upgrade to smartphones.

In 2019, Canalys forecasts 4.1% year-on-year growth for Thailand, with positive economic growth after its general election, which will improve major operators’ business outlook and prompt further investment from foreign mobile vendors. Though 5G is not expected to roll out until late 2020, operators will start to market the concept to build consumer interest in technology upgrades, which will be vital for consumer demand to rebound later in the year.

Vendor Highlights

Oppo leapfrogged Samsung, the long-term market leader, by growing nearly 70% year on year in Q4 2018. This was mainly thanks to its A3s, F7 and F9, which contributed nearly two thirds of its total shipments. Thailand has been one of Oppo’s most important markets in Southeast Asia and the vendor has invested heavily in local branding and services over the past five years. In 2018 the vendor has set its ambition to the flagship device segment. The biggest challenge Oppo faces in 2019 is to move upmarket and attract higher-spending users away from Samsung and Apple, to create enough differentiation between itself and strong competitors, such as Huawei and Vivo.

Samsung fell to second place, shipping just over 1.0 million units and falling 36.1% year on year. One of the main reasons for its disappointing Q4 was the product refresh of the J and A series, which are later than expected. But the J6+, J4+ and A7 2018 became top-shipping products in their launch quarters. As in other markets, Samsung is taking steps to respond to the price competition from the Chinese players by overhauling its mid-range strategy. The initial market response has been positive, but challenges remain in 2019 across all price bands for Samsung, especially at the high end, where it is still vulnerable.

Huawei produced a stellar performance in 2018. It displaced Vivo from third place in Q4 2018 by shipping 645,000 smartphones, representing 73.4% year-on-year growth. Huawei’s low-end Y series and Nova 3 were the key contributors to its growth in the past three quarters. Moreover, the rising popularity of its Honor-branded devices, which already tend to contribute over 100,000 units a quarter, will give Huawei more flexibility to work on more localized branding, which is vital for the vendor in the Thai smartphone market.

About Canalys

Canalys is an independent analyst company that strives to guide clients on the future of the technology industry and to think beyond the business models of the past. We deliver smart market insights to IT, channel and service provider professionals around the world. We stake our reputation on the quality of our data, our innovative use of technology and our high level of customer service.

Share on:

Suggested Items

IDTechEx Discusses Low-Loss Materials: The Enabler of Future Connected Vehicles?

05/06/2024 | IDTechExFuture connected vehicles will offer future drivers a safer, smoother, and more convenient driving experience. Not only will drivers get access to more navigation and entertainment options, but they will also gain access to safety technologies that will potentially reduce accidents, improve congestion, and reduce emissions globally by allowing vehicle safety systems to communicate with each other and with city traffic infrastructure.

HBM Prices to Increase by 5–10% in 2025, Accounting for Over 30% of Total DRAM Value

05/06/2024 | TrendForceAvril Wu, TrendForce Senior Research Vice President, reports that the HBM market is poised for robust growth, driven by significant pricing premiums and increased capacity needs for AI chips.

Tablet Shipments Show Signs of Recovery in Q1 2024

05/06/2024 | IDCAfter more than two years of decline, worldwide tablet shipments posted modest year-over-year growth of 0.5% in the first quarter of 2024 (1Q24), totaling 30.8 million units, according to preliminary data from the International Data Corporation (IDC) Worldwide Quarterly Personal Computing Device Tracker.

Industrial PC Market Size to Record $1.75 Billion Growth from 2023-2027

05/03/2024 | PRNewswireThe global industrial pc market size is estimated to grow by USD 1.75 billion from 2023 to 2027, according to Technavio. This growth is expected to occur at a Compound Annual Growth Rate (CAGR) of almost 6.29% during the forecast period.

Real Time with… IPC APEX EXPO 2024: Direct Imaging Equipment and Quad-wave DLP Light Engine Technology

05/03/2024 | Real Time with...IPC APEX EXPOGuest Editor Kelly Dack and MivaTek's Brendan Hogan delve into the company's innovative technologies, including direct imaging equipment and quad-wave DLP light engine technology. They highlight the benefits of direct imaging, compensation, and DART technology.