The Chemical Connection: Reducing Etch System Water Usage, Part 2

The Chemical Connection: Reducing Etch System Water Usage, Part 2 It’s Only Common Sense: Nice Guys Really Can Finish First

It’s Only Common Sense: Nice Guys Really Can Finish First The Right Approach: I Hear the Train A Comin'

The Right Approach: I Hear the Train A Comin'Can We Believe The Hype About China’s Domestic IC Production Plans?

June 17, 2019 | IC InsightsEstimated reading time: 3 minutes

Tariffs and trade issues are forcing China to scale its domestic IC production plans, but do its claims line up with reality? IC Insights believes they do not.

In the wake of tariffs and trade tension between China and the United States, government officials and company representatives throughout China have doubled down on their resolve to quickly and meaningfully grow the nation’s domestic IC business in order to reduce its dependence on critical IC components currently supplied by companies based in the U.S. and other countries.

In the memory IC market specifically, some recent headlines and reports have proclaimed that China is “unstoppable” and will soon match the output and technology level of Samsung, SK Hynix, and Micron. When those types of claims emerge, a reality check is in order.

Consider that China’s first indigenous DRAM supplier, Changxin Memory Technologies (CXMT), is due to sample its first DRAM products by the end of this year. This company has a few thousand employees and a capital spending budget of about $1.5 billion per year. In contrast, Micron and SK Hynix each have over 30,000 employees and Samsung’s memory division is estimated to have over 40,000. Moreover, in 2018, the combined capital spending from Samsung, SK Hynix, and Micron was $46.2 billion.

Overall, DRAM and flash memory accounted for 41% of China’s $155.1 billion IC market last year. Although some reports would have us believe that China’s wafer fab output is quickly increasing and that technology advances (particularly in memory) will catch up with those from the leading suppliers (within 3-5 years in some cases!), IC Insights completely disagrees.

While China continues to make large investments in its memory manufacturing infrastructure and has developed some clever design innovations in an attempt to avoid potential patent disputes, IC Insights remains extremely skeptical whether the country can develop a competitive indigenous memory industry even over the next 10 years and come anywhere close to meeting its memory IC needs.

One major issue, among many, that most observers overlook with regard to China becoming more self-reliant for its IC needs is its lack of indigenous non-memory IC technology. Currently, there are no major Chinese analog, mixed-signal, server MPU, MCU, or specialty logic IC manufacturers.

Moreover, these IC product segments, which represented over half of China’s IC market last year, are dominated by well-entrenched foreign IC producers with decades of experience and thousands of employees.

In IC Insights’ opinion, it will take decades for Chinese companies to become competitive in the non-memory IC product segments. While everyone is focused on China’s moves in the memory market, becoming self-reliant in non-memory IC segments poses an even more difficult problem for China.

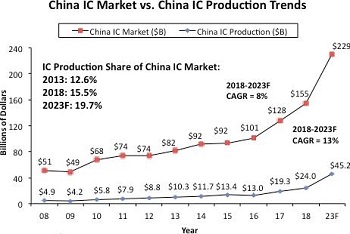

The figure shows China’s IC market versus China’s IC production. As seen, China’s IC market (IC sales into China) amounted to $155 billion in 2018.

Of the $155 billion worth of ICs sold in China last year, only $24.0 billion (15.5%) was manufactured in China. However, of the $24.0 billion worth of ICs manufactured in China last year, China-headquartered companies produced only $6.5 billion (27.0%), accounting for only 4.2% of the country’s $155 billion IC market. TSMC, SK Hynix, Samsung, Intel, and other foreign companies that have IC wafer fabs located in China produced the rest. IC Insights estimates that of the $6.5 billion in ICs manufactured by China-based companies, about $1.0 billion was from IDMs and $5.5 billion was from foundries like SMIC.

If China-based IC manufacturing rises to $45.2 billion in 2023 as IC Insights forecasts, China-based IC production would still represent only 8.4% of the total forecasted 2023 worldwide IC market of $538.8 billion. Even after adding a significant markup to some of the Chinese producers’ IC sales (many Chinese IC producers are foundries that sell their ICs to companies that re-sell these products to the electronic system producers), China-based IC production would still likely represent only about 10% of the global IC market in 2023.

Share on:

Suggested Items

IDTechEx Report on Quantum Technology: Nano-scale Physics for Massive Market Impact

04/30/2024 | PRNewswireThe quantum technology market leverages nano-scale physics to create revolutionary new devices for computing, sensing, and communications. Across the industry, quantum technology offers a paradigm shift in performance compared with incumbent solutions.

Guerrilla RF Completes Strategic Acquisition of GaN Device Portfolio from Gallium Semiconductor

04/29/2024 | BUSINESS WIREGuerrilla RF, Inc. has finalized the acquisition of Gallium Semiconductor's entire portfolio of GaN power amplifiers and front-end modules. Effective April 26th, 2024, GUER acquired all previously released components as well as new cores under development at Gallium Semiconductor.

Amphenol Reports Q1 2024 Results, Announces New Stock Repurchase Program

04/26/2024 | BUSINESS WIREAmphenol Corporation reported first quarter 2024 results. In addition, the Company is announcing a new three-year, $2 billion stock repurchase program.

Chinese Smartphone Market Maintains its Recovery Momentum at 6.5% Growth in 1Q24,

04/26/2024 | IDCAccording to preliminary data from the International Data Corporation (IDC) Worldwide Quarterly Mobile Phone Tracker, China smartphone shipments grew 6.5% year over year (YoY) to 69.3 million units in 1Q24.

Nanotechnology Market to Surpass $53.51 Billion by 2031

04/25/2024 | PRNewswireSkyQuest projects that the nanotechnology market will attain a value of USD 53.51 billion by 2031, with a CAGR of 36.4% over the forecast period (2024-2031).