Happy’s Tech Talk #28: The Power Mesh Architecture for PCBs

Happy’s Tech Talk #28: The Power Mesh Architecture for PCBs It’s Only Common Sense: Would You Join Your Own Company?

It’s Only Common Sense: Would You Join Your Own Company? The Chemical Connection: Reducing Etch System Water Usage, Part 2

The Chemical Connection: Reducing Etch System Water Usage, Part 2Global Notebook Shipments Forecast at Only 176 Million Units in 2023

November 3, 2022 | TrendForceEstimated reading time: 2 minutes

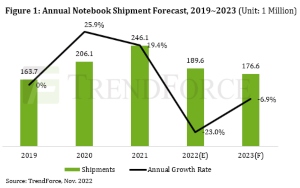

According to TrendForce, global notebook shipments in 4Q22 are likely to decline to 42.9 million units, down 7.2% QoQ and 32.3% YoY, lower than the same period before the pandemic. In addition, market demand is affected by negative factors such as inventory, the Russian-Ukrainian war, and rising inflation, leading to a downward revision of notebook market shipments in 2022 to 189 million units, a 23% decline YoY, with the proportion of shipments in the first and second half of the year at 53:47, the first top-heavy scenario in the past ten years.

According to research, the structural imbalance between notebook market supply and demand remains unresolved at present, leading this year's notebook shipments to present a downward movement trend quarter by quarter. TrendForce believes, after current inventory pressure gradually returns to a healthy level, Chromebooks may be the first wave of products that will see a recovery in demand by 2Q23 and traditional cyclical growth momentum is expected to return to the market, with shipments set to rebound slightly from 14.44 million in 2022 to 16.2 million units.

As mentioned above, pressure will continue in the consumer and commercial notebook market. Although demand for the former has been adjusting for five quarters, peak season momentum is still expected to play a major role. Coupled with assistance from the introduction of new CPUs, shipments of consumer notebooks will track closer to traditional peak season demand but declines will be inevitable throughout the year. Commercial demand faces dollar rate hikes leading to higher corporate borrowing rates and post-pandemic scenarios including capital expenditure adjustment, downsizing, and layoffs, which will cause an even greater decline than that of consumer notebooks.

In addition, although pandemic-induced demand has gradually weakening, hindering the growth of the high-end notebook market in 2022, TrendForce has observed that gaming and creator notebooks will remain cash cows. Facing the dilemma of the gradual decline in global notebook shipments, the high-margin nature of the segmented market has become more prominent. Major notebook manufacturers and processor brands such as Intel and Nvidia are all competing to expand, enhancing consumers’ user experience by means of high specifications and customization, while stimulating potential market demand to become a category of notebook computers capable of continual future growth.

However, inflationary pressure and geopolitics remain as variables in the general environment and the consumer electronics sector has borne the brunt of this uncertainty. The future shipment scale of the notebook computer market must still reference these relevant developments closely. In addition, considering that China continues to adopt a tough Zero-COVID policy after the 20th National Congress of the Communist Party of China and the adversarial relationship between it and the United States, supply chain strategies are also under scrutiny by major manufacturers. According to TrendForce research, due to the cumbersome and vast industrial settlement characteristics associated with notebook components, only major American manufacturers are currently promoting production development in Vietnam. Even though industrial chain reorganization to decouple from China has been in motion for some time, it still needs to be promoted by brands and ODMs in the short term.

As the global economy maintains course through battering headwinds, the International Monetary Fund (IMF) predicts that the 2023 economic growth rate will be approximately 2.7%, down 0.5 percentage points from 2022, which will be the most severe economic winter in 20 years. Overall, TrendForce estimates that there is no sign of obvious recovery in the global notebook market in 2023. Although the annual decline in shipments has abated to 6.9%, it will only reach 176 million units.

Share on:

Suggested Items

IDC Forecasts Slower Growth for Global Telecommunications Services Market: Could AI Help Telcos to Maintain Healthy Margins?

05/08/2024 | IDCWorldwide spending on Telecom Services and Pay TV Services reached $1,509 billion in 2023, an increase of 2.1% over 2022, according to the International Data Corporation (IDC) Worldwide Semiannual Telecom Services Tracker.

Simbe Partners with Plexus to Scale Manufacturing and Meet Global Retail Demand

05/08/2024 | Globe NewswireSimbe, the leading provider of Store Intelligence™ solutions that increase retailer performance through unprecedented visibility and insights, today announced a partnership with Plexus Corp. to bring its best-in-class retail robotics-as-a-service to market quickly and at global scale.

IDTechEx Discusses Low-Loss Materials: The Enabler of Future Connected Vehicles?

05/06/2024 | IDTechExFuture connected vehicles will offer future drivers a safer, smoother, and more convenient driving experience. Not only will drivers get access to more navigation and entertainment options, but they will also gain access to safety technologies that will potentially reduce accidents, improve congestion, and reduce emissions globally by allowing vehicle safety systems to communicate with each other and with city traffic infrastructure.

HBM Prices to Increase by 5–10% in 2025, Accounting for Over 30% of Total DRAM Value

05/06/2024 | TrendForceAvril Wu, TrendForce Senior Research Vice President, reports that the HBM market is poised for robust growth, driven by significant pricing premiums and increased capacity needs for AI chips.

Tablet Shipments Show Signs of Recovery in Q1 2024

05/06/2024 | IDCAfter more than two years of decline, worldwide tablet shipments posted modest year-over-year growth of 0.5% in the first quarter of 2024 (1Q24), totaling 30.8 million units, according to preliminary data from the International Data Corporation (IDC) Worldwide Quarterly Personal Computing Device Tracker.