Punching Out: Breaking Out of the Valuation Box

Punching Out: Breaking Out of the Valuation Box Happy’s Tech Talk #28: The Power Mesh Architecture for PCBs

Happy’s Tech Talk #28: The Power Mesh Architecture for PCBs It’s Only Common Sense: Would You Join Your Own Company?

It’s Only Common Sense: Would You Join Your Own Company?Strong Smartphone Growth in a Saturated Cellphone Market

November 23, 2015 | IC InsightsEstimated reading time: 3 minutes

Later this month, IC Insights will release its new 2016 IC Market Drivers Report. The report contains analyses on automotive electronics, the Internet of Things, tablet PCs, smartphones, medical and health systems, and several other mature and emerging electronic systems.

Figure 1 shows how important the replacement and multi-phone subscriber market has become to the cellphone industry.

Figure 1

As shown in Figure 1, 89% of the new cellphones sold worldwide in 2015 are forecast to be replacements or additional cellphones sold to existing subscribers. Moreover, this percentage is forecast to rise to 91% in 2016 and to 94% in 2019, which means that only about 6% of 2019 handset sales are expected to be to new customers. This very high replacement sales rate is similar to the situation that already exists in the U.S. automotive industry.

In the future, it will become increasingly critical for the cellphone supplier to convince the existing subscriber base that it needs, and is worth paying a premium for, the newest technology (usually a smartphone) or that it needs more than one cellular handset. If in the future a large portion of existing cellular users become "satisfied" with their cellphones (as happened in 2002 and 2009), it would serve to lengthen the replacement period and have the potential to significantly decrease annual cellphone unit shipment growth rates.

The vast majority of existing cellphone subscribers upgrade their phones to some version of a smartphone. Smartphones accounted for over 50% of total quarterly cellphone shipments for the first time ever in 1Q13 and are forecast to reach 410 million units in 4Q15 and represent 80% of total cellphones shipped that quarter. On an annual basis, smartphones first surpassed the 50% penetration level in 2013 (54%) and are forecast to represent 95% of total cellphone shipments in 2019.

In contrast to smartphones, total cellphone handset shipments are forecast to decline by 1% in 2015 and grow by only 2% in 2016 (Figure 2). As shown, non-smartphone cellphone sales dropped by 24% in 2014 and are expected to drop by another 30% this year. Moreover, IC Insights forecasts that the 2016 non-smartphone cellphone unit shipment decline will be similar to 2015’s drop with a decline of 28%.

Samsung and Apple dominated the smartphone market in 2014 and are expected to do so again this year. In total, these two companies shipped 504 million smartphones and held a combined 40% share of smartphone shipments last year. However, although these two companies are forecast to ship 560 million smartphones in 2015, their combined smartphone unit marketshare is expected to drop one percentage point to 39%.

Samsung’s total cellphone unit shipments are forecast to drop by 1% in 2015. Moreover, its 2015 smartphone shipments are expected to grow by only 5%, a weak showing in a market that is forecast to grow 13% this year. With a surge in orders for Apple’s new iPhone 6s, Apple’s smartphone shipments are expected to jump by 20% in 2015, much better than the total 13% growth rate for the worldwide smartphone market. It appears that Samsung is losing smartphone marketshare to the up-and-coming Chinese producers like Huawei and Xiaomi while Apple continues to dominate the high-end smartphone segment.

In contrast to the forecasted double-digit declines in smartphone sales of Microsoft/Nokia and Sony this year, 2015 smartphone sales from most of the top China-based suppliers are expected to surge. Combined, the seven top-12 smartphone suppliers that are based in China are forecast to ship 437 million smartphones this year, a 23% increase from the 355 million smartphones these seven companies shipped in 2014. As a result, the top seven Chinese smartphone suppliers together are expected to hold a 31% share of the worldwide smartphone market in 2015, up three points from the 28% share these companies held in 2014 and nine points better than the 22% combined share these companies held in 2013.

Page 1 of 2

Share on:

Suggested Items

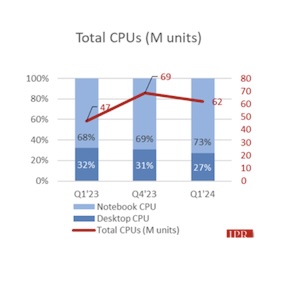

PC Client CPU Shipments in 1Q24 Up 33% YoY

05/10/2024 | Jon Peddie ResearchJon Peddie Research reports the growth of the global PC client-based CPU units market reached 62 million units in Q1’24, a decrease of -9.4% quarter to quarter and a 33% growth from Q1’23.

Omdia: OLED Monitor Display shipments to surge by 123% YoY as Top Brands Embrace its Technology in 2024

05/09/2024 | PRNewswireOLED monitor display shipments significantly increased in 2023, following an upsurge of 415% year-over-year (YoY), according to Omdia's Monitor Display & OEM Market Tracker. This trend is set to continue with Omdia forecasting a 123% YoY increase in 2024, reaching 1.84 million units, driven by industry leaders Samsung Display and LG Display.

IDTechEx Report: Illuminating the Future of Lidar in Automotive

05/09/2024 | PRNewswireIn the rapidly evolving landscape of Advanced Driver-Assistance Systems (ADAS) and autonomous driving, sensor technologies have emerged as a pivotal force driving innovations in the automotive industry.

Sondrel Awarded New Video Processor ASIC Design and Supply Contract

05/09/2024 | SondrelSondrel, a leading provider of ultra-complex custom chips for leading global technology brands, is pleased to announce that it has won a major ASIC design and supply contract for a next generation, video processing chip.

IDC Forecasts Slower Growth for Global Telecommunications Services Market: Could AI Help Telcos to Maintain Healthy Margins?

05/08/2024 | IDCWorldwide spending on Telecom Services and Pay TV Services reached $1,509 billion in 2023, an increase of 2.1% over 2022, according to the International Data Corporation (IDC) Worldwide Semiannual Telecom Services Tracker.