The Chemical Connection: Onshoring PCB Production—Daunting but Certainly Possible

The Chemical Connection: Onshoring PCB Production—Daunting but Certainly Possible It’s Only Common Sense: The Phone Is Still Mightier Than the Keyboard

It’s Only Common Sense: The Phone Is Still Mightier Than the Keyboard

India Smartphone Market Sees a Healthy Growth of 20% in Q2 2018

August 13, 2018 | IDCEstimated reading time: 5 minutes

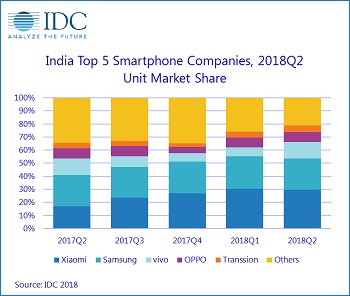

According to the IDC India’s Quarterly Mobile Phone Tracker, smartphone companies shipped a total of 33.5 million units to India during the second quarter of 2018 (2Q18), resulting in a healthy 20% year-over-year (YoY) growth. IDC believes that this is the result of a slew of online exclusive launches and strong shipments by offline heavy vendors on the back of high decibel promotional activities and channel schemes.

The market, however, is seeing rapid consolidation at the top end, as the top 5 vendors made up 79% of the smartphone market in 2Q18, marginalizing smaller brands” says Upasana Joshi, associate research manager, Client Devices, IDC India.

Xiaomi remains the leader in the smartphone market with growing offline presence while maintaining dominance in the online space. Xiaomi contributed more than 56% of the shipments in online space, while 33% of its shipments went through offline channels in 2Q18.

In the online segment, Huawei with strong shipments of its Honor branded phones, climbed to the second position with an all-time high of 8% share in online segment in 2Q18. “Huawei has had a stellar quarter worldwide moving into the second position, toppling Apple. In India, with a refreshed focus it has been able to grow its share in the online space in the last two quarters, on the back of several new launches across price segments. IDC believes Huawei should be seen as a serious long-term player in India market with all the ingredients to challenge Xiaomi and Samsung” adds Joshi.

Other online-focused vendors with online exclusive launches were OnePlus with its new launch OnePlus 6, Realme with Realme1 and Asus with Zenfone Max Pro series, all of which led to an annual growth of 44% in the online channel shipments and taking the online share to 36% of the smartphone market.

Offline segment growth was driven by vivo which had strong shipments during the quarter on the back of high decibel marketing campaigns around new launches like V9 including advertisement campaign featuring popular movie star Amir Khan, title sponsorship in Indian Premier League cricket tournament and attractive booster schemes available for channel partners.

“The growing popularity of financing schemes in the offline channel across model portfolios by almost all vendors is driving affordability and thus pushing the overall smartphone ASP’s to a record high of $167 in 2Q18 from $157 in 2Q17,” adds Joshi.

The premium end of the market ($500+) grew almost two times year-over-year (YoY) mainly due to continued strong shipments of Samsung Galaxy S9 series and OnePlus 6, with OnePlus surpassing Apple to be the second biggest player in the $500+ segment with a share of 21% in 2Q18.

The feature phone market remained resilient with shipments of 44.0 million units in 2Q18, seeing a growth of 29% over 2Q17. Reliance Jio, the telecom operator and the main driver of the 4G feature phone segment with its JioPhone range of phones, remained the top vendor in the overall feature phone market. However, the 4G feature phone market saw a slight decline of 10% QoQ with 19.0 million units. IDC believes that this drop is due to JioPhone inventory buildup from 1Q18.

Reliance Jio, as an attempt for clearing this inventory, recently introduced the "Monsoon Hungama" feature phone exchange offer and brought popular apps like WhatsApp, YouTube on JioPhone. The 2G feature phone segment continued to decline further as local players struggle for survival in this segment and segment is losing relevance due to the aggressive push in the 4G feature phone segment by Reliance Jio.

Top 5 Smartphone Vendor Highlights

Xiaomi maintained its leadership position with its highest ever shipments in a single quarter in 2Q18. The vendor’s shipments saw a growth of 10% sequentially and grew more than two-fold annually. Its four smartphone models captured the top four slots in top models ranking, namely Redmi 5A, Redmi Note 5 Pro, Redmi Note 5 and Redmi 5, together accounting for 26% of overall smartphone shipments.

Samsung remained at the second position in the smartphone market with an impressive 21% Year-over-year (YoY) growth at the back of its newly launched “infinity” series model namely Galaxy J6. The brand continues to see strong shipments of its successful low-end models – Galaxy J7 Nxt, Galaxy J2 (2017) and J2 (2018), thus driving overall volumes. The high-end segment ($500 and above) saw incremental demand with cash back offers and financing schemes across channels.

vivo reclaimed its 3rd position, as its shipments grew more than double from the previous quarter, registering a strong 18% year on year growth in 2018Q2. The hit models namely Y71, V9 and Y83 being the key volume drivers.

OPPO slipped to 4th position, however, its shipments grew by 15% Year-over-year (YoY) in 2Q18 due to fewer marketing initiatives and absence of attractive offline channel schemes.

Transsion continued to be at the 5th position, as its offline focused Tecno branded phones grew by 26% followed by itel with 14% QoQ growth in 2Q18. The online exclusive brand Infinix grew by 45%, registering an overall 53% Year-over-year (YoY) growth for the company. Transsion's stability in the market can be attributed to successful channel management, focus on the low-end segment and strong retailer connect.

IDC India Forecast

“India will be the fastest growing large smartphone market for the next few years, making it a must for any smartphone player to be here. However, with increasing consolidation, it will be difficult for any new brand to carve a space here. IDC estimates the India smartphone market to continue growing in low double digits for the next couple of years. 2H18, with multiple sale events in the run-up to the Diwali festival, will be even bigger with growing aggression by online players, the sustained relevance of offline channel and several new launches planned by key vendors across price segments.” says Navkendar Singh, associate research director, Client Devices, IDC India.

About IDC Trackers

IDC Tracker products provide accurate and timely market size, company share, and forecasts for hundreds of technology markets from more than 100 countries around the globe. Using proprietary tools and research processes, IDC's Trackers are updated on a semiannual, quarterly, and monthly basis. Tracker results are delivered to clients in user-friendly excel deliverables and on-line query tools. The IDC Tracker Charts app allows users to view data charts from the most recent IDC Tracker products on their iPhone and iPad.

About IDC

International Data Corporation (IDC) is the premier global provider of market intelligence, advisory services, and events for the information technology, telecommunications, and consumer technology markets. With more than 1,100 analysts worldwide, IDC offers global, regional, and local expertise on technology and industry opportunities and trends in over 110 countries. IDC's analysis and insight helps IT professionals, business executives, and the investment community to make fact-based technology decisions and to achieve their key business objectives. Founded in 1964, IDC is a subsidiary of IDG, the world's leading technology media, research, and events company.

Share on:

Testimonial

"Our marketing partnership with I-Connect007 is already delivering. Just a day after our press release went live, we received a direct inquiry about our updated products!"

Rachael Temple - AlltematedSuggested Items

The Marketing Minute: Marketing With Layers

10/15/2025 | Brittany Martin -- Column: The Marketing MinuteMarketing to a technical audience is like crafting a multilayer board: Each layer serves a purpose, from the surface story to the buried detail that keeps everything connected. At I-Connect007, we’ve learned that the best marketing campaigns aren’t built linearly; they’re layered. A campaign might start with a highly technical resource, such as an in-depth article, a white paper, or a podcast featuring an engineer delving into the details of a process. That’s the foundation, the substance that earns credibility.

ICT Symposium Review: Sustainability and the Circular Economy

10/09/2025 | Pete Starkey, I-Connect007It was pleasant autumnal weather as we made our way once again to Meriden, the nominal centre of England, for the 2025 Annual Symposium of the Institute of Circuit Technology. Delegates were welcomed by technical director Emma Hudson who introduced and moderated a skilfully coordinated programme, focused on the highly relevant theme of sustainability.

Circular Packaging Market to Reach $98.0 Billion by 2035

10/08/2025 | Fact.MRThe market's journey from USD 45.8 billion in 2025 to USD 98.0 billion by 2035 represents substantial growth, the market will rise at a CAGR of 7.9% demonstrating the accelerating adoption of sustainable packaging systems and circular economy solutions across food & beverage, personal care, and e-commerce sectors.

It’s Only Common Sense: Stop Whining About the Market—Outwork It

10/06/2025 | Dan Beaulieu -- Column: It's Only Common SenseWhenever the market hiccups or the industry cycle dips, I hear the same tired chorus: “The market is down. Customers aren’t buying. What can we do? We just have to wait it out.” Nonsense. If you think that by showing up, opening your doors, and waiting for the economy to smile kindly upon you, that success will follow, you are in the wrong business. Worse yet, you’re living in the wrong mindset. Most people don’t want to hear the truth that winners find business in down cycles. Losers blame the economy.

Schweizer Ends Staff Restructuring Measures and Short-Time Working at the Schramberg Site

10/01/2025 | Schweizer Electronic AGSchweizer Electronic AG has implemented comprehensive measures to adjust its cost and personnel structure at its Schramberg site due to strong market fluctuations in the automotive and industrial electronics sector. Thanks to the successful restructuring, short-time working can now be ended with immediate effect. A stable order situation is expected for the fourth quarter, with signs of growth momentum returning in 2026.