It’s Only Common Sense: The Phone Is Still Mightier Than the Keyboard

It’s Only Common Sense: The Phone Is Still Mightier Than the Keyboard The Marketing Minute: Marketing With Layers

The Marketing Minute: Marketing With Layers

DRAM Market Braces for Slower Growth

October 8, 2018 | IC InsightsEstimated reading time: 2 minutes

History suggests that DRAM ASP and market growth will soon trend downward; suppliers cautious and stand ready to adjust capex expansion plans.

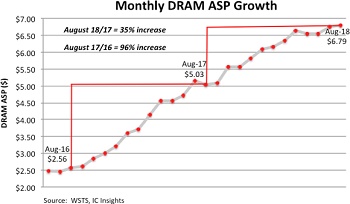

In its September Update to The 2018 McClean Report, IC Insights discloses that over the past two years, DRAM manufacturers have been operating their memory fabs at nearly full capacity, which has resulted in steadily increasing DRAM prices and sizable profits for suppliers along the way. The DRAM average selling price (ASP) reached $6.79 in August 2018, a 165% increase from two years earlier in August of 2016. Although the DRAM ASP growth rate has slowed this year compared to last, it has remained on a solid upward trajectory through the first eight months of 2018.

The DRAM market is known for being very cyclical and after experiencing strong gains for two years, historical precedence now strongly suggests that the DRAM ASP (and market) will soon begin trending downward. One indicator suggesting that the DRAM ASP is on the verge of decline is back-to-back years of huge increases in DRAM capital spending to expand or add new fab capacity. DRAM capital spending jumped 81% to $16.3 billion in 2017 and is expected to climb another 40% to $22.9 billion this year. Capex spending at these levels would normally lead to an overwhelming flood of new capacity and a subsequent rapid decline in prices.

However, what is slightly different this time around is that big productivity gains normally associated with significant spending upgrades are much less at the sub-20nm process node now being used by the top DRAM suppliers as compared to the gains seen in previous generations.

At its Analyst Day event held earlier this year, Micron presented figures showing that manufacturing DRAM at the sub-20nm node requires a 35% increase in the number of mask levels, a 110% increase in the number of non-lithography steps per critical mask level, and 80% more cleanroom space per wafer out since more equipment—each piece with a larger footprint than its previous generation—is required to fabricate ≤20nm devices. Bit volume increases that previously averaged around 50% following the transition to a smaller technology node, are a fraction of that amount at the ≤20nm node. The net result is suppliers must invest much more money for a smaller increase in bit volume output. So, the recent uptick in capital spending, while extraordinary, may not result in a similar amount of excess capacity, as has been the case in the past.

The DRAM ASP is forecast to rise 38% in 2018 to $6.65, but IC Insights forecasts that DRAM market growth will cool as additional capacity is brought online and supply constraints begin to ease. (It is worth mentioning that Samsung and SK Hynix in 3Q18 reportedly deferred some of their expansion plans in light of expected softening in customer demand.)

Of course, a wildcard in the DRAM market is the role and impact that the startup Chinese companies will have over the next few years. It is estimated that China accounts for approximately 40% of the DRAM market and approximately 35% of the flash memory market.

At least two Chinese IC suppliers, Innotron and JHICC, are set to participate in this year’s DRAM market. Although China’s capacity and manufacturing processes will not initially rival those from Samsung, SK Hynix, or Micron, it will be interesting to see how well the country’s startup companies perform and whether they will exist to serve China’s national interests only or if they will expand to serve global needs.

Share on:

Testimonial

"Our marketing partnership with I-Connect007 is already delivering. Just a day after our press release went live, we received a direct inquiry about our updated products!"

Rachael Temple - AlltematedSuggested Items

The Marketing Minute: Marketing With Layers

10/15/2025 | Brittany Martin -- Column: The Marketing MinuteMarketing to a technical audience is like crafting a multilayer board: Each layer serves a purpose, from the surface story to the buried detail that keeps everything connected. At I-Connect007, we’ve learned that the best marketing campaigns aren’t built linearly; they’re layered. A campaign might start with a highly technical resource, such as an in-depth article, a white paper, or a podcast featuring an engineer delving into the details of a process. That’s the foundation, the substance that earns credibility.

ICT Symposium Review: Sustainability and the Circular Economy

10/09/2025 | Pete Starkey, I-Connect007It was pleasant autumnal weather as we made our way once again to Meriden, the nominal centre of England, for the 2025 Annual Symposium of the Institute of Circuit Technology. Delegates were welcomed by technical director Emma Hudson who introduced and moderated a skilfully coordinated programme, focused on the highly relevant theme of sustainability.

Circular Packaging Market to Reach $98.0 Billion by 2035

10/08/2025 | Fact.MRThe market's journey from USD 45.8 billion in 2025 to USD 98.0 billion by 2035 represents substantial growth, the market will rise at a CAGR of 7.9% demonstrating the accelerating adoption of sustainable packaging systems and circular economy solutions across food & beverage, personal care, and e-commerce sectors.

It’s Only Common Sense: Stop Whining About the Market—Outwork It

10/06/2025 | Dan Beaulieu -- Column: It's Only Common SenseWhenever the market hiccups or the industry cycle dips, I hear the same tired chorus: “The market is down. Customers aren’t buying. What can we do? We just have to wait it out.” Nonsense. If you think that by showing up, opening your doors, and waiting for the economy to smile kindly upon you, that success will follow, you are in the wrong business. Worse yet, you’re living in the wrong mindset. Most people don’t want to hear the truth that winners find business in down cycles. Losers blame the economy.

Schweizer Ends Staff Restructuring Measures and Short-Time Working at the Schramberg Site

10/01/2025 | Schweizer Electronic AGSchweizer Electronic AG has implemented comprehensive measures to adjust its cost and personnel structure at its Schramberg site due to strong market fluctuations in the automotive and industrial electronics sector. Thanks to the successful restructuring, short-time working can now be ended with immediate effect. A stable order situation is expected for the fourth quarter, with signs of growth momentum returning in 2026.