It’s Only Common Sense: The Phone Is Still Mightier Than the Keyboard

It’s Only Common Sense: The Phone Is Still Mightier Than the Keyboard The Marketing Minute: Marketing With Layers

The Marketing Minute: Marketing With Layers

Consolidation and Capacity Cut in Solar Industry Expected Due to Gradual Phase-Out of Subsidies Worldwide

October 9, 2018 | TrendForceEstimated reading time: 3 minutes

EnergyTrend, a division of TrendForce, reports that some countries are planning or have started phasing out their solar subsidy programs as the global solar photovoltaic (PV) industry and market show stability in their development. During 2013-2017, the average annual growth rate of total PV demand was above 20%. However, this strong growth scenario will unlikely to happen in the future. As the market enters a stagnant phase, manufacturers across the PV supply chain have to be more cautious when planning capacity expansion so that they do not risk incurring losses.

In the latest Gold Member Solar Report by EnergyTrend (3Q18), the grid-connected PV generation capacity worldwide is estimated to increase by around 95GW in 2018. However, the actual PV demand for the entire 2018 is estimated to reach just 86GW. During 2017, numerous developers of PV power plants in China had to move their installation target dates forward. At the same time, the US solar companies also stocked up in advance due to their government’s investigation on PV imports under Section 201 of the 1974 Trade Act. Consequently, a part of demand originally reserved for 2018 had been spent in 2017.

The global production capacity for PV cells is estimated to increase to nearly 150GW in 2018. The global production capacity for PV modules is also estimated to increase to about the same amount in 2018. On the whole, the oversupply problem has become more acute. Additionally, there have been geographical shifts in the global supply and demand. India officially imposed its 25% safeguard duty on PV cells in 3Q18, just as the EU lifted the minimum import price and the anti-dumping and countervailing duty on Chinese PV imports. As a result, China-made PV modules are again flowing into regional markets that they were previously barred from.

Lions Shih, research manager of EnergyTrend, expects consolidation to occur among product manufacturers and among power plant developers. Smaller solar companies will face serious challenges as they are being squeezed out of the market by larger and growing competitors. In the case of Taiwan’s solar industry, three domestic solar enterprises – Gintech, Neo Solar Power, and Solartech – have merged in order to increase in scale and create vertical integration. Several PV manufacturers in Taiwan have also downsized their workforces and cut their production capacity. These are the necessary steps that have to be taken because of the market situation. Manufacturers in China, too, are expected to adopt similar measures, including merger deals, capacity reduction, and even factory closure.

Shih points out that demand drives growth and advances of the solar industry as a whole since it influences the mood of the market and price trends. Demand growth, however, continues to be mainly driven by government policies. Going forward, manufacturers across the supply chain will assess trajectories of prices based on various country-specific (or region-specific) indicators. The rates of a country’s feed-in tariff scheme and electricity prices set under tenders for PV power plants, for example, are important policy-related indicators. Another significant indicator is the grid parity targets that are being seriously discussed within the industry during the recent period.

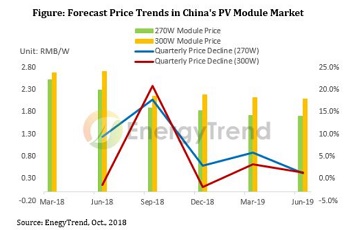

Quarterly observations of module prices in China during 2018 find that prices of conventional mono-Si products and conventional multi-Si products dropped by 19.8% and 25.5% on average, respectively, from 1Q18 to 3Q18. If solar PV generation is to come very close to grid parity in China at the start of 3Q19, then prices of conventional mono-Si and conventional multi-Si modules will have to drop by another 2.8% and 9.8%, respectively, during the nine-month period from the start of 4Q18 to the end of 2Q19. To the meet expectation that the price PV electricity has to reach the grid parity level, manufacturers in different sections of the supply chain will be under pressure to keep pushing down their costs.

About TrendForce

TrendForce is a global provider of the latest development, insight, and analysis of the technology industry. Having served businesses for over a decade, the company has built up a strong membership base of 435,000 subscribers. TrendForce has established a reputation as an organization that offers insightful and accurate analysis of the technology industry through five major research divisions: DRAMeXchange, WitsView, LEDinside, EnergyTrend and Topology. Founded in Taipei, Taiwan in 2000, TrendForce has extended its presence in China since 2004 with offices in Shenzhen and Beijing.

Share on:

Testimonial

"The I-Connect007 team is outstanding—kind, responsive, and a true marketing partner. Their design team created fresh, eye-catching ads, and their editorial support polished our content to let our brand shine. Thank you all! "

Sweeney Ng - CEE PCBSuggested Items

MES Software Tools Need Thoughtful Integration

10/21/2025 | Nolan Johnson, SMT007 MagazineThe Global Electronics Association recently published a survey report on the state of EMS production software. This project, led by Thiago Guimaraes, director of industry intelligence, connects the dots across the global electronics value chain to uncover practical insights that individual companies might not have seen on their own. In this interview, Thiago discusses the whys and hows of this report.

SEMICON West: The Path to a $1 Trillion Future

10/14/2025 | Marcy LaRont, I-Connect007After more than 50 years in San Francisco, SEMICON West moved its 2025 show to Phoenix, which is significant because it highlights the importance of Arizona as a semiconductor and tech hub. Though the show will be back in San Francisco in 2026, the overwhelmingly warm welcome SEMI received from Arizona Governor Katie Hobbs, Phoenix Mayor Kate Gallego, and ASU President Michael Crowe—who has been responsible for ASU repeatedly achieving the U.S. News and World Reports most innovative university ranking—was remarked upon repeatedly. All indications are that SEMICON West may well be back in Phoenix after that 2026 season.

Technica USA Named Exclusive U.S. Distributor for DCT Cleaning Products

10/14/2025 | Technica USATechnica USA is pleased to announce a strategic partnership with DCT USA, LLC, becoming the exclusive master distributor of DCT cleaning products in the United States, effective November 1, 2025.

Is Glass Finally Coming of Age?

10/13/2025 | Nolan Johnson, I-Connect007Substrates, by definition, form the base of all electronic devices. Whether discussing silicon wafers for semiconductors, glass-and-epoxy materials in printed circuits, or the base of choice for interposers, all these materials function as substrates. While other substrates have come and gone, silicon and FR-4 have remained the de facto standards for the industry.

Amplifying Innovation: New Podcast Series Spotlights Electronics Industry Leaders

10/08/2025 | I-Connect007In the debut episode, “Building Reliability: KOKI’s Approach to Solder Joint Challenges,” host Marcy LaRont speaks with Shantanu Joshi, Head of Customer Solutions and Operational Excellence at KOKI Solder America. They explore how advanced materials, such as crack-free fluxes and zero-flux-residue solder pastes, are addressing issues like voiding, heat dissipation, and solder joint reliability in demanding applications, where failure can result in costly repairs or even catastrophic loss.