The Marketing Minute: Marketing With Layers

The Marketing Minute: Marketing With Layers The Right Approach: Electro-Tek—A Williams Family Legacy, Part 1

The Right Approach: Electro-Tek—A Williams Family Legacy, Part 1 It’s Only Common Sense: If You’re Not Differentiated, You’re Dead

It’s Only Common Sense: If You’re Not Differentiated, You’re Dead

Cloud IT Infrastructure Revenues Surpassed Traditional IT Infrastructure Revenues

January 11, 2019 | IDCEstimated reading time: 2 minutes

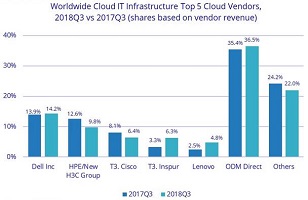

According to the International Data Corporation (IDC) Worldwide Quarterly Cloud IT Infrastructure Tracker, vendor revenue from sales of IT infrastructure products (server, enterprise storage, and Ethernet switch) for cloud environments, including public and private cloud, grew 47.2% year over year in the third quarter of 2018 (3Q18), reaching $16.8 billion. IDC also raised its forecast for total spending (vendor revenue plus channel mark-up) on cloud IT infrastructure in 2018 to $65.2 billion with year-over-year growth of 37.2%.

Quarterly spending on public cloud IT infrastructure has more than doubled in the past two years reaching $12.1 billion in 3Q18 and growing 56.1% year over year, while spending on private cloud infrastructure grew at half of this rate, 28.3%, reaching $4.7 billion. Since 2013, when IDC started tracking IT infrastructure deployments in different environments, public cloud has represented the majority of spending on cloud IT infrastructure and in 2018 IDC expects this share will peak at 68.8% with spending on public cloud infrastructure growing at an annual rate of 44.7%. Spending on private cloud will grow 23.3% year over year in 2018.

In 3Q18, for the first time, quarterly vendor revenues from IT infrastructure product sales into cloud environments surpassed revenues from sales into traditional IT environments, accounting for 50.9% of the total worldwide IT infrastructure vendor revenues, up from 43.6% a year ago. However, for the full year 2018, spending on cloud IT infrastructure will remain below the 50% mark at 47.4%. Spending on all three technology segments in cloud IT environments is forecast to deliver double-digit growth in 2018. Compute platforms will be the fastest growing at 59.1%, while spending on Ethernet switches and storage platforms will grow 18.5% and 20.4%, respectively.

The rate of growth for the traditional (non-cloud) IT infrastructure segment slowed down from the first half of the year to 14.8%, which is still exceptional for this market segment. For the full year, worldwide spending on traditional non-cloud IT infrastructure is expected to grow by 12.3% as the market goes through a technology refresh cycle, which will wind down by 2019. By 2022, we expect that traditional non-cloud IT infrastructure will only represent 42.4% of total worldwide IT infrastructure spending (down from 52.6% in 2018). This share loss and the growing share of cloud environments in overall spending on IT infrastructure is common across all regions.

"The first three quarters of 2018 were exceptional for the IT Infrastructure market across all deployment environments and the increase in IT infrastructure investments by public cloud datacenters was especially strong driven by the opening of new datacenters and infrastructure refresh in existing datacenters," said Natalya Yezhkova, research director, IT Infrastructure and Platforms. "After such a strong year we expect some slowdown in 2019 as the overall market cools down and some cloud providers work through adjustments in their supply chain. However, IDC expects the shift in IT infrastructure spending toward cloud environments will continue."

All regions grew their cloud IT Infrastructure revenues by double digits in 3Q18. Revenue growth was the fastest in Asia/Pacific (excluding Japan) (APeJ) at 62.6% year over year, with China growing at an even higher rate of 88.7%. Other regions among the fastest growing in 3Q18 included Japan (48.2%), USA (44.2%), and Canada (43.4%).

Long-term, IDC expects spending on cloud IT infrastructure to grow at a five-year compound annual growth rate (CAGR) of 13.3%, reaching $88.6 billion in 2022 and accounting for 57.6% of total IT infrastructure spend. Public cloud datacenters will account for 66.3% of this amount, growing at an 13.6% CAGR. Spending on private cloud infrastructure will grow at a CAGR of 12.6%.

Share on:

Testimonial

"Your magazines are a great platform for people to exchange knowledge. Thank you for the work that you do."

Simon Khesin - Schmoll MaschinenSuggested Items

Nvidia, Microsoft, and BlackRock Lead $40 Billion Deal to Acquire Aligned Data Centers

10/16/2025 | I-Connect007 Editorial TeamA consortium including Nvidia, Microsoft, BlackRock, and Elon Musk’s xAI has agreed to buy Aligned Data Centers in a deal valued at about $40 billion, marking one of the largest-ever data infrastructure acquisitions as tech giants race to expand capacity for artificial intelligence, the Associated Press reported on Oct. 14

India’s Aerospace and Defence Engineered for Power, Driven by Electronics

09/16/2025 | Gaurab Majumdar, Global Electronics AssociationWith a defence budget of $82.05 billion (2025–26) and a massive $223 billion earmarked for aerospace and defence spending over the next decade, India is rapidly positioning itself as a major player in the global defence and aerospace market.

Alphabet Boosted by AI, Cloud Demand as Spending Needs Jump

07/24/2025 | I-Connect007 Editorial TeamGoogle’s parent company, Alphabet Inc., said that demand for artificial intelligence products boosted its quarterly sales, and now requires an extreme increase in capital spending to keep up in the AI race, Bloomberg reported. For 2025, the company stated its capital expenditure will be $85 billion—$10 billion more than previously forecast.

Report: Broadcom Scraps $1 Billion Chip Investment in Spain

07/15/2025 | I-Connect007 Editorial TeamAmerican chipmaker Broadcom has pulled out of plans to invest in a microchip plant in Spain. According to a July 14 Reuters report, Europa Press, quoting anonymous sources, stated the action followed collapsed government talks but gave no further information.

Wolfspeed Stock Soars After Filing for Chapter 11 Bankruptcy

07/01/2025 | I-Connect007 Editorial TeamOn July 1, Wolfspeed shares doubled following the company’s announcement on June 30 that it had filed for Chapter 11 bankruptcy protection.