Standard of Excellence: The Future of Fabrication—From Art to Automation

Standard of Excellence: The Future of Fabrication—From Art to Automation Knocking Down the Bone Pile: The Business Case for Component Reclamation

Knocking Down the Bone Pile: The Business Case for Component Reclamation Global Sourcing Spotlight: The Hidden Power of the Rep Network

Global Sourcing Spotlight: The Hidden Power of the Rep Network

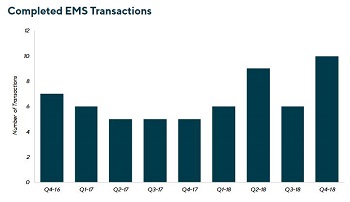

According to Lincoln International's Q4 2018 EMS Quarterly Report, there were 31 EMS transactions recorded in 2018, up significantly from the 21 recorded in 2017. The primary driver of the increase in transaction activity was due to the favorable M&A market conditions in 2018. In addition, M&A opportunities were stronger as companies are performing well due to the electronics "supercycle". EMS consolidations were the most common type of transaction with 16 transactions in 2018, or 52% of total activity, compared to seven transactions in 2017, which represented 33% of activity last year.

In 2018, there were five vertical/horizontal convergences, down from the seven recorded in 2017, which represented 16% of the total, compared to 33% last year. Private equity investments accounted for six transactions in 2018, reflecting a slight increase in the number of investments compared to the five transactions recorded in 2017. This type of transaction represented approximately 19% of the total transactions for 2018, slightly lower than the 24% mix of the total for 2017.

There were no EMS divestitures during 2018, down from only one transaction recorded (5% of the total) in 2017. There was one transaction categorized as diversification into EMS (3% of the total) during 2018, which is equivalent to the one transaction (5% of total activity) in this category for 2017. One of the most significant changes was the completion of three OEM divestitures in 2018, representing approximately 10% of total transaction activity. There were no OEM divestitures in 2017 and this is the first year since 2010 that we have seen this level of activity in this category. The expertise that EMS companies have in managing the supply chain were especially beneficial during this recent history of component shortages, making OEM divestitures a more attractive proposition in certain cases.

In terms of geography, 12 of the transactions were completed in North America. This represented 39% of total transaction activity in 2018. Almost equivalent in terms of transaction volume was Europe with 11 transactions in 2018, representing 35% of total activity. There were also 6 cross-border transactions in 2018 (19% of the total), with only one between a high-cost region and a low-cost region and 5 transactions between different high-cost regions. There were also two transactions recorded within Asia representing approximately 6% of total transaction activity.

In terms of transaction size, Small Tier EMS providers accounted for 74% of the 2018 transaction volume with 23 acquisitions. Mid Tier and Large Tier EMS providers each accounted for four acquisitions, representing approximately 13% of total activity, respectively. For the Mid Tier this represents a slight decrease compared to the five transactions recorded in 2017 but is a slight increase for the Large Tier having completed only three transaction last year.