Driving Innovation: Mechanical and Optical Processes During Rigid-flex Production

Driving Innovation: Mechanical and Optical Processes During Rigid-flex Production It’s Only Common Sense: Your Biggest Competitor Is Complacency

It’s Only Common Sense: Your Biggest Competitor Is Complacency The Chemical Connection: Onshoring PCB Production—Daunting but Certainly Possible

The Chemical Connection: Onshoring PCB Production—Daunting but Certainly Possible

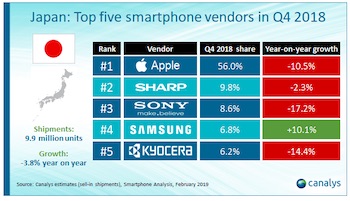

Apple Dominates in Japan with 56% Share as Market Falls 3.8% in 4Q18

February 19, 2019 | CanalysEstimated reading time: 3 minutes

Smartphone shipments fell 3.8% year on year in Japan to 9.9 million in Q4 2018, marking a fourth consecutive quarter of shipment decline. In terms of shipment numbers, Japan came fourth worldwide, behind China, the US and India. 32.5 million smartphones shipped in Japan in the whole of 2018, 1.9% fewer than in 2017.

The performance of the Japanese market has been adversely affected by the notoriously high mobile tariff costs and increasing device costs, especially for iPhones, given mobile operators are given lower subsidies, capped by the MIC and JFTC. This has slowed the replacement cycle, especially as 48-month contracts have been introduced by the major operators. On the other hand, this has given a boost to lower-cost SIM-only contracts and the secondhand smartphone market.

Despite a sharp 10.5% decline in Q4, Apple still enjoys a dominant position in Japan, its full-year market share exceeding 50% for the first time in 2018, up from 48.0% in 2017 and 48.2% in 2016. Sharp, in a distant second place, only accounted for 11% of shipments in 2018. Competition is becoming more intense for Android vendors. Local names, such as Sharp, Sony and Kyocera, which used to account for a sizeable share of the market, are being increasingly challenged by Samsung, Huawei and Google, which have pushed in with aggressive spending on marketing.

Canalys forecasts a modest 2.7% year-on-year decline for Japan in 2019, as it is further affected by the lengthening refresh cycle. A changing market dynamic is forthcoming in 2019 – a price cut in mobile subscription costs of up to 40% is imminent due to pressure from the regulators. Premium handset and local vendors, such as Sharp and Kyocera, whose sales rely on subsidies and operator promotions, are expected to be dealt an even heavier blow. There will be growth opportunities for mid-to-low-end handsets via MVNOs and open channels. Moreover, Rakuten, which is due to launch its own network in October 2019, will become Japan’s fourth operator, further adding to channel competition. As Japan aims to be 5G-ready in 2020 for the Tokyo Summer Olympics, operators have rushed to launch the first commercial 5G network. But the big three operators may find it hard to fund investment amid the impact of further mobile cost regulation on their revenue.

Vendor Highlights:

Apple dominated in Japan with a 56.0% market share in Q4 2018, down from 60% in Q4 2017 as shipments fell sharply by 10.5% year on year, more than the overall market. The iPhone XR contributed 39.8% of Apple’s shipments in Q4, helped by aggressive subsidies from major operators to offset the lower demand for its XS series due to the high prices. The flagship XS and XS Max performed poorly compared to the earlier iPhone X during their launch quarters, shipping only 1.4 million units in aggregate, which inevitably dragged down Apple’s overall ASP to US$744 from US$794 last year. At the lower end, the iPhone 6S increased shipments due to Docomo’s “Docomo with” plan, which comes with much lower subscription costs aimed to attract lower-income users. The biggest challenge for Apple in 2019 is to retain its dominance amid downward pressure on operator subsidies, the rising secondhand market and increasing competition from vendors such as Huawei.

It has been tough for the Japanese vendors on their home turf. Sharp, Sony, Kyocera and Fujitsu continued to struggle in Japan, suffering declines of varying degrees in Q4 2018 due to a lack of competitive products. Despite being constantly challenged by foreign vendors, the four local vendors retained a combined market share of 25.2% this quarter due to traditional strong ties with the major operators. But the outlook remains bleak for local vendors in 2019.

Being the only top five vendor that achieved positive year-on-year growth of 10.1%, with nearly 680,000 units shipped, Samsung owes much of its success to the strong performance of the S9 and S9 Note compared to their predecessors. Samsung also grew 168% quarter on quarter due to a boost from its Galaxy Feel 2, which is specially designed for Japanese consumers. Being Samsung’s only mid-range device in Japan, the Galaxy Feel series has been instrumental in creating volume growth for the vendor. But Samsung will start to feel the pressure as Chinese vendors, such as Huawei and Oppo, continue to grow in Japan.

About Canalys

Canalys is an independent analyst company that strives to guide clients on the future of the technology industry and to think beyond the business models of the past. We deliver smart market insights to IT, channel and service provider professionals around the world. We stake our reputation on the quality of our data, our innovative use of technology and our high level of customer service.

Share on:

Testimonial

"We’re proud to call I-Connect007 a trusted partner. Their innovative approach and industry insight made our podcast collaboration a success by connecting us with the right audience and delivering real results."

Julia McCaffrey - NCAB GroupSuggested Items

Aircraft Wire and Cable Market to surpass USD 3.2 Billion by 2034

10/30/2025 | Global Market Insights Inc.The global aircraft wire and cable market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 3.2 billion by 2034, according to recent report by Global Market Insights Inc.

The Marketing Minute: Marketing With Layers

10/15/2025 | Brittany Martin -- Column: The Marketing MinuteMarketing to a technical audience is like crafting a multilayer board: Each layer serves a purpose, from the surface story to the buried detail that keeps everything connected. At I-Connect007, we’ve learned that the best marketing campaigns aren’t built linearly; they’re layered. A campaign might start with a highly technical resource, such as an in-depth article, a white paper, or a podcast featuring an engineer delving into the details of a process. That’s the foundation, the substance that earns credibility.

ICT Symposium Review: Sustainability and the Circular Economy

10/09/2025 | Pete Starkey, I-Connect007It was pleasant autumnal weather as we made our way once again to Meriden, the nominal centre of England, for the 2025 Annual Symposium of the Institute of Circuit Technology. Delegates were welcomed by technical director Emma Hudson who introduced and moderated a skilfully coordinated programme, focused on the highly relevant theme of sustainability.

Circular Packaging Market to Reach $98.0 Billion by 2035

10/08/2025 | Fact.MRThe market's journey from USD 45.8 billion in 2025 to USD 98.0 billion by 2035 represents substantial growth, the market will rise at a CAGR of 7.9% demonstrating the accelerating adoption of sustainable packaging systems and circular economy solutions across food & beverage, personal care, and e-commerce sectors.

It’s Only Common Sense: Stop Whining About the Market—Outwork It

10/06/2025 | Dan Beaulieu -- Column: It's Only Common SenseWhenever the market hiccups or the industry cycle dips, I hear the same tired chorus: “The market is down. Customers aren’t buying. What can we do? We just have to wait it out.” Nonsense. If you think that by showing up, opening your doors, and waiting for the economy to smile kindly upon you, that success will follow, you are in the wrong business. Worse yet, you’re living in the wrong mindset. Most people don’t want to hear the truth that winners find business in down cycles. Losers blame the economy.