Driving Innovation: Mechanical and Optical Processes During Rigid-flex Production

Driving Innovation: Mechanical and Optical Processes During Rigid-flex Production It’s Only Common Sense: Your Biggest Competitor Is Complacency

It’s Only Common Sense: Your Biggest Competitor Is Complacency The Chemical Connection: Onshoring PCB Production—Daunting but Certainly Possible

The Chemical Connection: Onshoring PCB Production—Daunting but Certainly Possible

DRAM Revenue Took a Turn for the Worse in 4Q18;

February 25, 2019 | TrendForceEstimated reading time: 4 minutes

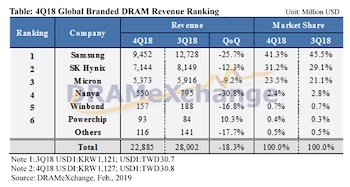

Investigations by DRAMeXchange, a division of TrendForce, show that DRAM quotes have taken a turn for the worse in 4Q18, causing the total revenue in the DRAM industry to fall. Due to high inventory levels on the demand end, purchases have become few and little, in turn causing a sales bit decline QoQ for most DRAM vendors. Under this double decline of both quantity and price, the global DRAM revenue fell by 18.3% QoQ in 4Q18.

DRAMeXchange pointed out that contract prices continued to fall in January 2019. In view of the pricings by first-tier PC-OEMs, the average prices of mainstream 8GB modules have descended to US$50 for January, and will continue their descent through the monthly deals of February and March, with an estimated decline of 20-25% for the first quarter overall. Additionally, the production bit levels of DRAM suppliers in 4Q18 were far above sales bit levels, intensifying inventory pressure. Thus suppliers will redouble their efforts on pricing strategies to accelerate inventory closeouts.

From a revenue standpoint, most suppliers are fated to meet the inescapable quarterly decline. Taking the brunt of the sharp decline of server DRAM shipments, industry giant Samsung has seen the steepest sales bit decline in the fourth quarter among the top three vendors, with its revenue falling by 25.7% QoQ to US$9.45 billion, and its revenue market share retreating to 41.3%. SK Hynix sales bit, however, only saw a drop of around 2%, thus taking a softer fall in revenue compared to Samsung: 12.3% QoQ to US$7.14 billion. Its revenue market share rose above the 30% mark, landing at 31.2%.

Micron still held on to third place, with its revenue coming to US$5.37 billion, thanks to its adoption of more flexible shipment strategies. Although this was a drop of 9.2% QoQ, Micron still performed the best out of the top three suppliers, its revenue market share rising to 23.5%.

DRAMeXchange estimates that Samsung, faced with the double pressure of its quickly eroding revenue share and rather high inventory levels, will be more proactive in its pricing strategies to avoid continual share shrinkage.

Looking at supplier profitability, the global price drop in 4Q18 form the beginning of the end for peaking revenues, and OPMs everywhere exhibited a decline. The supplier giant Samsung made the least effort to lower prices and drive sales, which, along with the steadily increasing allocation of 1Ynms, caused only a slight OPM drop from 70% to 66%. However, though pricings took a turn for the worse in the fourth quarter, DRAM production still enjoyed a gross margin of around 80%, which demonstrates that Samsung still has an arrow in its quiver to carry out more flexible pricing strategies.

SK Hynix completed a large number of shipments in the fourth quarter, sacrificing their profitability in the process. SK Hynix’s OPM fell from 66% in 3Q18 to 58% in 4Q18. Micron, however, released a fiscal report spanning from September to November—and thus did not show a price fall to the extent of those calculated by Korean suppliers, which spanned from October to December—showing a mere drop of OPM from 62% to 58%. Looking towards 1Q19, suppliers will expect a further shrinkage in potential profits from the increasingly dramatic drop in prices.

On the technological front, with Samsung’s expansion of its wafer production capacity on Line 17 and the raising of the DRAM production on the second floor of the Pyeongtaek plant, they have achieved their 2018 year-end target of a combined 1X+1Ynm production allocation of 70%. Although there are no plans on wafer production increase for the Pyeongtaek plant, Line 17 and the second floor Pyeongtaek plant will still continue their transition into 1Ynm, albeit one slowed by the current market. As for SK Hynix, 1Xnm yield rates have gotten on track, and the newly constructed second 12-inch wafer fab in Wuxi has begun contributing to output for the first half of this year. However, they won’t get too active on increasing wafer production in the Wuxi fab due to the US-China trade dispute. Regarding Micron, its subsidiary Micron Memory Taiwan (formerly Rexchip) has already completed the transition to 1Xnm production, and will be directly transitioning into 1Znm production, but substantial contributions will have to wait until 2020. Micron Technology Taiwan (formerly Inotera) has already begun the switch from 20nm to 1Xnm in the second quarter last year, and will begin to move on to 1Ynm in the first half of this year and gradually increase its percentage.

With respect to Taiwan-based suppliers, due to the weakening PC DRAM market, Nanya recorded a 20% fall in sales bit performance along with a huge drop of 30.8% QoQ in revenue for the fourth quarter. DDR4, which had a better gross margin, took up a smaller fraction in shipments – this, along with the global decline in quotes, caused OPM to shrink from 51.0% to 41.8%. It is feared that profitability will continue to shrink amidst rising depreciation and amortization expenses and the decreasing cost benefit of the 20nm process.

Powerchip’s DRAM revenue rose by 10.3% QoQ if the calculation excludes its DRAM foundry business. If this part of the revenue were included, then the result would actually be a nearly double-digit decline from the previous quarter. As for Winbond, its DRAM revenue fell by 16.8% QoQ. The price cuts that Winbond made were relatively modest within the industry, averaging less than 5% QoQ. However, the weak overall demand dragged down the company’s sales bit, which decreased by more than 10% QoQ.

About TrendForce

TrendForce is a global provider of the latest development, insight, and analysis of the technology industry. Having served businesses for over a decade, the company has built up a strong membership base of 435,000 subscribers. TrendForce has established a reputation as an organization that offers insightful and accurate analysis of the technology industry through five major research divisions: DRAMeXchange, WitsView, LEDinside, EnergyTrend and Topology. Founded in Taipei, Taiwan in 2000, TrendForce has extended its presence in China since 2004 with offices in Shenzhen and Beijing.

Share on:

Testimonial

"Advertising in PCB007 Magazine has been a great way to showcase our bare board testers to the right audience. The I-Connect007 team makes the process smooth and professional. We’re proud to be featured in such a trusted publication."

Klaus Koziol - atgSuggested Items

Aircraft Wire and Cable Market to surpass USD 3.2 Billion by 2034

10/30/2025 | Global Market Insights Inc.The global aircraft wire and cable market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 3.2 billion by 2034, according to recent report by Global Market Insights Inc.

The Marketing Minute: Marketing With Layers

10/15/2025 | Brittany Martin -- Column: The Marketing MinuteMarketing to a technical audience is like crafting a multilayer board: Each layer serves a purpose, from the surface story to the buried detail that keeps everything connected. At I-Connect007, we’ve learned that the best marketing campaigns aren’t built linearly; they’re layered. A campaign might start with a highly technical resource, such as an in-depth article, a white paper, or a podcast featuring an engineer delving into the details of a process. That’s the foundation, the substance that earns credibility.

ICT Symposium Review: Sustainability and the Circular Economy

10/09/2025 | Pete Starkey, I-Connect007It was pleasant autumnal weather as we made our way once again to Meriden, the nominal centre of England, for the 2025 Annual Symposium of the Institute of Circuit Technology. Delegates were welcomed by technical director Emma Hudson who introduced and moderated a skilfully coordinated programme, focused on the highly relevant theme of sustainability.

Circular Packaging Market to Reach $98.0 Billion by 2035

10/08/2025 | Fact.MRThe market's journey from USD 45.8 billion in 2025 to USD 98.0 billion by 2035 represents substantial growth, the market will rise at a CAGR of 7.9% demonstrating the accelerating adoption of sustainable packaging systems and circular economy solutions across food & beverage, personal care, and e-commerce sectors.

It’s Only Common Sense: Stop Whining About the Market—Outwork It

10/06/2025 | Dan Beaulieu -- Column: It's Only Common SenseWhenever the market hiccups or the industry cycle dips, I hear the same tired chorus: “The market is down. Customers aren’t buying. What can we do? We just have to wait it out.” Nonsense. If you think that by showing up, opening your doors, and waiting for the economy to smile kindly upon you, that success will follow, you are in the wrong business. Worse yet, you’re living in the wrong mindset. Most people don’t want to hear the truth that winners find business in down cycles. Losers blame the economy.