Driving Innovation: Mechanical and Optical Processes During Rigid-flex Production

Driving Innovation: Mechanical and Optical Processes During Rigid-flex Production It’s Only Common Sense: Your Biggest Competitor Is Complacency

It’s Only Common Sense: Your Biggest Competitor Is Complacency The Chemical Connection: Onshoring PCB Production—Daunting but Certainly Possible

The Chemical Connection: Onshoring PCB Production—Daunting but Certainly Possible

Supply Chain, Geopolitical Issues to Stem Commercial Appetite Growth of EMEA PC Market in 2019

February 27, 2019 | IDCEstimated reading time: 2 minutes

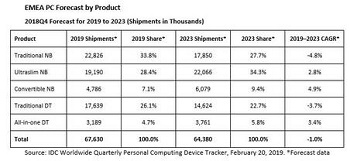

EMEA shipments of traditional PCs (a combination of desktops, notebooks, and workstations) will total 67.6 million in 2019, a 3.5% YoY decline, according to IDC's latest Quarterly PCD Tracker. Ongoing renewals and the impending end of Windows 7 support will provide plenty of units for the commercial segment to remain afloat, but this will be insufficient to offset the heavy decline in the consumer space. Ultramobile devices will continue to fare far better than their traditional counterparts, with ultraslims expected to continue on their strong growth trajectory across both segment groups.

Accelerating demand for mobility to address the growing prevalence of mobile workers, combined with the imminent end of Windows 7 support, now just a year away, will incentivize notebook refreshes in both public and private sectors. The Windows 10 refresh is expected to generate strongest growth in the midmarket as more of the larger accounts were fulfilled at the tail end of 2018. The outlook for desktops remains negative but has been modestly improved, primarily driven by small and ultrasmall form factors that provide an optimal solution to maximizing desk space without compromising on power.

"The Western European PC market is expected to remain constrained, driven by the CPU supply chain shortage and the difficult political situation in major economies," said Malini Paul, research manager, IDC Western European Personal Computing Devices. "While the ongoing shortage of notebooks is anticipated to ease by end of 2019Q2, the CPU supply issue with desktops will continue to impact shipments in the second half of the year."

With data being the most valuable resource for businesses, security will continue to be very important in the commercial space, as companies require devices that can be trusted. Consequently, newer models with enhanced security measures will continue to garner higher demand. The ongoing shift in consumer demand toward more thin and light mobile form factors continues to be a challenge for desktop adoption. However, with better prospects in gaming, strong processing power, and ability to customize, desktops will give the form factor greater relevance in the consumer category. Ultraslims, convertibles, and gaming will continue to drive the consumer space. In addition, the anticipated shift in the CPU shortage toward desktops in 2019H2 will contribute to the overall improvement of notebooks in the consumer market in 2019.

"The overall PC market results in the CEE and MEA regions were very different for 2018. CEE reported healthy growth of 6.5% YoY, whereas MEA contracted by 6.5% YoY. The CEE region was mostly driven by strong demand in Russia in both consumer and commercial sectors, while MEA was inhibited by the economic and political uncertainties and the currency fluctuation in Turkey," said Stefania Lorenz, associate VP, IDC CEMA.

"The outlook for MEA in 2019H1 will remain obscured by economic uncertainty and CPU shortages. However, the region is foreseeing a return to growth in the second half of 2019 as Turkey is expected to turn around after the worst market contraction ever witnessed in 2018H2. The CEE region is expected to slow down in 2019, after four years of continuous growth. The first quarter in 2019 will be affected by the Intel CPU shortage and some built-up inventory across the region, while the remaining quarters of the year are forecast to be flat with few visible deals in the pipeline," she said.

IDC's Quarterly PCD Tracker provides unmatched market coverage and forecasts for the entire device space, covering PCs and tablets, in more than 80 countries — providing fast, essential, and comprehensive market information across the entire personal computing device market.

Share on:

Testimonial

"Advertising in PCB007 Magazine has been a great way to showcase our bare board testers to the right audience. The I-Connect007 team makes the process smooth and professional. We’re proud to be featured in such a trusted publication."

Klaus Koziol - atgSuggested Items

Aircraft Wire and Cable Market to surpass USD 3.2 Billion by 2034

10/30/2025 | Global Market Insights Inc.The global aircraft wire and cable market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 3.2 billion by 2034, according to recent report by Global Market Insights Inc.

The Marketing Minute: Marketing With Layers

10/15/2025 | Brittany Martin -- Column: The Marketing MinuteMarketing to a technical audience is like crafting a multilayer board: Each layer serves a purpose, from the surface story to the buried detail that keeps everything connected. At I-Connect007, we’ve learned that the best marketing campaigns aren’t built linearly; they’re layered. A campaign might start with a highly technical resource, such as an in-depth article, a white paper, or a podcast featuring an engineer delving into the details of a process. That’s the foundation, the substance that earns credibility.

ICT Symposium Review: Sustainability and the Circular Economy

10/09/2025 | Pete Starkey, I-Connect007It was pleasant autumnal weather as we made our way once again to Meriden, the nominal centre of England, for the 2025 Annual Symposium of the Institute of Circuit Technology. Delegates were welcomed by technical director Emma Hudson who introduced and moderated a skilfully coordinated programme, focused on the highly relevant theme of sustainability.

Circular Packaging Market to Reach $98.0 Billion by 2035

10/08/2025 | Fact.MRThe market's journey from USD 45.8 billion in 2025 to USD 98.0 billion by 2035 represents substantial growth, the market will rise at a CAGR of 7.9% demonstrating the accelerating adoption of sustainable packaging systems and circular economy solutions across food & beverage, personal care, and e-commerce sectors.

It’s Only Common Sense: Stop Whining About the Market—Outwork It

10/06/2025 | Dan Beaulieu -- Column: It's Only Common SenseWhenever the market hiccups or the industry cycle dips, I hear the same tired chorus: “The market is down. Customers aren’t buying. What can we do? We just have to wait it out.” Nonsense. If you think that by showing up, opening your doors, and waiting for the economy to smile kindly upon you, that success will follow, you are in the wrong business. Worse yet, you’re living in the wrong mindset. Most people don’t want to hear the truth that winners find business in down cycles. Losers blame the economy.