Dan’s Biz Bookshelf: ‘Abundance: How We Build a Better Future’

Dan’s Biz Bookshelf: ‘Abundance: How We Build a Better Future’ Trouble in Your Tank: In Complex Systems, Design Rules Aren’t Optional

Trouble in Your Tank: In Complex Systems, Design Rules Aren’t Optional It’s Only Common Sense: The Phone Is Still Your Competitive Advantage

It’s Only Common Sense: The Phone Is Still Your Competitive Advantage

AR/VR Spending in Asia/Pacific excluding Japan to Reach $34.9B by 2022

March 27, 2019 | IDCEstimated reading time: 3 minutes

Asia/Pacific excluding Japan (APEJ) spending on augmented reality and virtual reality (AR/VR) will reach $7.1 billion in 2019, an increase of 75.2% from the previous year, according to the latest IDC Worldwide Semiannual Augmented and Virtual Reality Spending Guide. IDC expects consumer and enterprise/commercial segments spending in AR/VR products and services to grow at a five-year compound annual growth rate (CAGR) of 70.7% over the forecast period (2017-22).

"As the lines between digital and physical continue to blur, several progressive organizations across Asia Pacific are experimenting or deploying AR/VR technologies to prepare for the future of work. Use cases of AR/VR are emerging across sectors that include delivering more personalized customer experiences, accelerated product designing and go to market, AR guided workflows and maintenance, as well as VR trainings for better learning outcomes and improved health and safety for employees," said Avinav Trigunait, Research Director for Future of Work at IDC Asia/Pacific.

As the technology continues to evolve, several content developments and designing software vendors such as Adobe and Autodesk are including AR/VR features in their solutions to make it easier to develop both AR/VR content and applications. Also, with many new AR/VR software and hardware products being launched in 2019, enterprises are expected to continue exploring the use of AR/VR technologies for a variety of new use cases and IDC forecasts the commercial segment spending in Asia Pacific to surpass consumer spending in 2019, added Trigunait.

Hardware will account for nearly half of all AR/VR spending throughout the forecast followed by software and services. The largest category of hardware spending will be host devices, but AR viewers will have the highest growth rate over the forecast period, (CAGR of more than 150%). Software contributes around 39.3% of the overall spend, of which AR software spending is leading in terms of growth with 108.2% CAGR (2017-22). Likewise, services spending is likely to proliferate by CAGRs of AR Systems Integration 143.0%. Thereby, the robust growth in AR hardware, software and services spending will drive overall AR spending quite ahead of VR spending by 2022.

Consumer is the largest industry in AR/VR spending, which accounts for 41.2% of the overall spend in 2018. Commercial segment AR/VR solutions will see its combined share of overall spending increase from 58.8% in 2018 to more than 64.0% in 2022. Within commercial segment, the industries that are expected to spend the most on AR/VR in 2018 include personal and consumer services followed by education and retail.

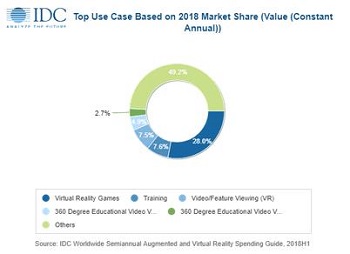

Virtual reality games are a leading use case garnering around 28.03% of the overall AR/VR spend in 2018, followed by training, and video/feature viewing (VR). However, lab and field (post-secondary), and retail showcasing are the fastest growing use case in terms of compound annual growth rate over the forecast (2017-22).

"We see that the commercial segment is showcasing growth given the steady rise in spending throughout the forecast. On the other hand, augmented and virtual reality technology is rising as a consumer focused segment widely noticeable in the gaming and entertainment industry-focused solutions," said Ritika Srivastava, Associate Market Analyst at IDC Asia/Pacific. "Furthermore, there are massive opportunities for industries including education, healthcare, retail and manufacturing to expedite their businesses in digital realm by implementing applications catering from customer interactions, product design and development, trainings and simulations etc.," adds Srivastava.

China market will represent the largest AR/VR spending in the APEJ region with 83.0% share in 2018 and the spending is projected to take off at a five-year CAGR of 76.2% during the forecast period (2017-22). While, AR/VR technology in ASEAN countries of Asia/Pacific (excluding Japan) are slowly gaining trend and experimenting on how AR/VR can improve the industry experience.

The IDC Worldwide Semiannual Augmented and Virtual Reality Spending Guide examines the AR/VR opportunity and provides insights into this rapidly growing market and how the market will develop over the next five years. Revenue data is available for eight regions, 12 industries, 26 use cases, and eleven technology categories. Unlike any other research in the industry, the comprehensive spending guide was created to help IT decision makers to clearly understand the industry-specific scope and direction of AR/VR expenditures today and in the future.

About IDC Spending Guides

IDC's Spending Guides provide detail on key technology markets from a regional, vertical industry, use case, buyer, and technology perspective. The spending guides are delivered via pivot table format or custom query tool, allowing the user to easily extract meaningful information about each market by viewing data trends and relationships

About IDC

International Data Corporation (IDC) is the premier global provider of market intelligence, advisory services, and events for the information technology, telecommunications, and consumer technology markets. With more than 1,100 analysts worldwide, IDC offers global, regional, and local expertise on technology and industry opportunities and trends in over 110 countries. IDC's analysis and insight helps IT professionals, business executives, and the investment community to make fact-based technology decisions and to achieve their key business objectives. Founded in 1964, IDC is a wholly-owned subsidiary of International Data Group (IDG), the world's leading media, data and marketing services company that activates and engages the most influential technology buyers.

Share on:

Subscribe

Stay ahead of the technologies shaping the future of electronics with our latest newsletter, Advanced Electronics Packaging Digest. Get expert insights on advanced packaging, materials, and system-level innovation, delivered straight to your inbox.

Subscribe now to stay informed, competitive, and connected.

Suggested Items

I-Connect007 Editor’s Choice: Five Must-Reads for the Week

05/08/2026 | Marcy LaRont, I-Connect007This week, I’ve selected some outstanding interviews that you’ll want to take note of. First, is a roundtable discussion featuring three dynamic industry cybersecurity experts. Please watch this important discussion that affects us all. Following that, I spotlight the IPC-2581 Consortium, which explains why IPC-2581 is the standard to replace Gerber data for manufacturing. Next, I am including my interview with PCBAA and AAM, who collaborated to release a short documentary on U.S. PCB manufacturing.

Hall of Fame Spotlight Series: Highlighting Karen McConnell

05/07/2026 | Dan Feinberg, I-Connect007In 2021, Karen McConnell was awarded the Raymond E. Pritchard Hall of Fame award in recognition of her contributions to the Association and the electronics industry. As a senior staff member and CAD/CAM engineer at Northrop Grumman Enterprise Services, her primary responsibility was to develop a common, shared EDM (Electronic Document Management) library to support the electrical and PCB design tool initiatives across Northrop Grumman Mission Systems.

A Necessary Shift From Gerber to IPC-2581

05/07/2026 | Tracy Riggan, Global Electronics AssociationIPC-2581 is an open, vendor-neutral data exchange standard developed by the Global Electronics Association to streamline the exchange of PCB design information across fabrication, assembly, and test. It replaces multiple legacy formats—including industry standards, Gerber, and ODB++—with a single, comprehensive, XML-based dataset that captures all manufacturing details.

Meet Emerging Engineers: Patrick Owen and Eric Mickenbecker, Summit Interconnect

05/05/2026 | Michelle Te, I-Connect007Patrick Owen and Eric Mickenbecker both work for Summit Interconnect, and are in their second year of the Global Electronics Association’s Emerging Engineer Program with mentor Brian Chislea. They stopped by the I-Connect007 booth at APEX EXPO and shared a bit of their story with me. Patrick has worked at the Hollister, California, plant since 2018, while Eric has been at the Chicago site since 2023. Like many of their peers, they came to the electronics industry from different paths, but are both excited about making an impact.

PCBAA, AAM Take on the Fight to Rebuild U.S. Manufacturing in New Documentary

05/05/2026 | Marcy LaRont, I-Connect007Throughout most of the 20th century, manufacturing was central to the American Dream of providing stable jobs and pathways to upward mobility. Today, more than 80% of global electronics manufacturing capacity resides in China and greater Asia, raising serious concerns about supply chain resilience and national security.