Dan’s Biz Bookshelf: ‘Abundance: How We Build a Better Future’

Dan’s Biz Bookshelf: ‘Abundance: How We Build a Better Future’ Trouble in Your Tank: In Complex Systems, Design Rules Aren’t Optional

Trouble in Your Tank: In Complex Systems, Design Rules Aren’t Optional It’s Only Common Sense: The Phone Is Still Your Competitive Advantage

It’s Only Common Sense: The Phone Is Still Your Competitive Advantage

Huawei Ban Temporarily Relaxed

July 9, 2019 | TrendForceEstimated reading time: 2 minutes

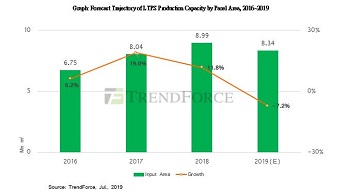

WitsView, a division of TrendForce, says that demand for LTPS devices were previously expected to grow steadily in 2019 and cause utilization for LTPS production lines to climb. But due to the effects of the Huawei ban, LTPS area produced is expected to shrink starting from 3Q, with the annual area produced expected to fall by about 7.2% compared to 2018, arriving at just 8.3 million square-meters. This is the first time in recent years that LTPS area faces the risk of decline. However, it is worth observing whether panel demand will recover swiftly as the US relaxes for now the sales ban on Huawei in the wake of G20.

TrendForce explains that as LTPS production capacity ceases to expand, panel suppliers are fighting for orders from clients, leading to intense competition in panel prices. Furthermore, LTPS panels with narrower bezels, energy-saving and other specifications performed better in the market and thus increase customers' acceptance of LTPS panels. It was originally forecast that, as more and more brands increasingly adopt LTPS devices, the share of these devices in the smartphone market will rise from 37% last year to 42.1% this year. But the Huawei ban near the end of May introduced some changes to the supply-demand situation of LTPS panels.

TrendForce points out that Huawei's phone shipments for 2019 were originally feared to become impacted by the US ban, impacting orders along the panel supply chain. This moved panel suppliers to adjust utilization from June onwards. Since this series of order adjustments was caused by a sudden event, panel manufacturers probably won't be able to completely transfer production capacity to other applications or clients in the short-term. After the decline of the South China “white box” market, most customer brands also don't have the ability to absorb the additional production capacity of panel manufacturers. The expected share of LTPS devices in the global smartphone market is therefore cut down to 40.6%, which also implies a spike in LTPS panel oversupply pressure in the short term.

Originally, panel manufacturers and phone customer brands had to take some time to adjust their supply/demand situation under the restrictions of the ban. TrendForce therefore predicted that as phone brands began to set their annual goals for 2020 entering 4Q19, total utilization for LTPS production lines may get a chance to recover. But after the relaxing of the Huawei ban, it remains to be observed whether utilization may experience a full recovery by mid-3Q or the end of 3Q.

Meanwhile, another risk limiting the future development of LTPS panels is AMOLED panel supply. Production capacity for AMOLED panels will increase as China's panel manufacturers actively increase production capacities overall, and phone customer brands will also increase their demand for AMOLED panels. This will no doubt crowd out LTPS panels to some extent in the future, and as soon as LTPS panels lose the support of demand from large-scale customers such as Huawei, they will necessarily expand their market reach, either moving towards mid-range or low-end phones and eroding the shares of a-Si devices, or accelerating the turn towards non-phone applications.

Share on:

Subscribe

Stay ahead of the technologies shaping the future of electronics with our latest newsletter, Advanced Electronics Packaging Digest. Get expert insights on advanced packaging, materials, and system-level innovation, delivered straight to your inbox.

Subscribe now to stay informed, competitive, and connected.

Suggested Items

Global Electronics Association and CalcuQuote, an Elisa Industriq Business, Launch Joint Supply Chain Intelligence Initiative

04/29/2026 | Global Electronics AssociationThe Global Electronics Association and CalcuQuote, Elisa Industriq today announced a partnership to deliver timely, actionable supply chain intelligence for the electronics industry.

Is China Plus One Still Happening in the PCB Industry?

04/28/2026 | Manfred Huschka, Manfred Huschka Management Consulting (Shenzhen) Ltd.For much of the past five years, China Plus One has been shorthand for supply-chain diversification: reducing dependency on mainland China by adding manufacturing capacity elsewhere in Asia. In the PCB industry, however, in early 2026, it is more nuanced. It looks less like a clean geographic shift and more like a layered, capital-intensive rebalancing of global capacity, one that still leaves China deeply embedded at the center.

It's Only Common Sense: See Your Marketing as a Discipline, Not a Department

04/27/2026 | Dan Beaulieu -- Column: It's Only Common SenseWhat does marketing mean to you? Is it a corner office with cool posters on the wall? Is it the person running your LinkedIn page or the trade show booth with the shiny graphics and the bowl of candy? Yes, marketing is those things, but it’s more than that. It’s a discipline, and if you treat it like a department, you’re already losing.

Roundtable: Advanced Materials

04/27/2026 | I-Connect007 Editorial TeamDriven largely by the need for advanced chip technology for super compute ability and AI applications, low Dk, low-loss resin systems, and heavy copper laminate are attracting significant attention and global resources. There are numerous unavoidable challenges in this market that will impact manufacturers and the supply chain, and they may be hitting critical mass sooner than OEMs and fabricators think. In this roundtable discussion, moderator Marcy LaRont speaks with topic experts: Mark Goodwin, John Fix, and Ed Kelley.

Infineon Further Extends Global Leadership in the Automotive Semiconductor Market

04/13/2026 | InfineonInfineon Technologies AG has once again proven to be the world’s leading automotive semiconductor supplier.