It’s Only Common Sense: Stay Curious, My Friends

It’s Only Common Sense: Stay Curious, My Friends The Marketing Minute: AI Is Watching Your Marketing Habits

The Marketing Minute: AI Is Watching Your Marketing Habits

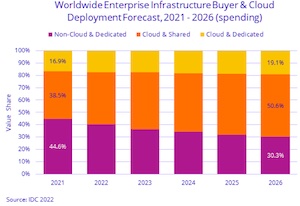

According to the International Data Corporation (IDC) Worldwide Quarterly Enterprise Infrastructure Tracker: Buyer and Cloud Deployment, spending on compute and storage infrastructure products for cloud deployments, including dedicated and shared environments, increased 17.2% year over year in the first quarter of 2022 (1Q22) to $18.3 billion. This growth continues a series of strong year-over-year increases in spending on infrastructure products by both service providers and enterprises despite tight supply of some system components and disruptions in transportation networks. Investments in non-cloud infrastructure increased 9.8% year over year in 1Q22 to $14.8 billion, continuing a streak of growth for this segment into its fifth quarter.

Spending on shared cloud infrastructure reached $12.5 billion in the quarter, increasing 15.7% compared to a year ago. IDC expects to see continuously strong demand for shared cloud infrastructure with spending expected to surpass non-cloud infrastructure spending in 2022 for the first time. Spending on dedicated cloud infrastructure increased 20.5% year over year in 1Q22 to $5.9 billion. Of the total dedicated cloud infrastructure, 47.8% was deployed on customer premises.

For the full year 2022, IDC is forecasting cloud infrastructure spending to grow 22% compared to 2021 to $90.2 billion – the highest annual growth rate since 2018 – while non-cloud infrastructure is expected to grow 1.8% to $60.7 billion. The increased forecast for both segments is partially driven by inflationary pressure and expectations of higher systems prices during 2022 as well as improvements in the supply chain in the second half of the year. Shared cloud infrastructure is expected to grow by 24.3% year over year to $63.9 billion for the full year. Spending on dedicated cloud infrastructure is expected to grow 16.8% to $26.3 billion for the full year.

As part of the Tracker, IDC follows various categories of service providers and how much compute and storage infrastructure these service providers purchase, including both cloud and non-cloud infrastructure. The service provider category includes cloud service providers, digital service providers, communications service providers, and managed service providers. In 1Q22, service providers as a group spent $18.3 billion on compute and storage infrastructure, up 14.5% from 1Q21. This spending accounted for 55.3% of total compute and storage infrastructure spending. Spending by non-service providers increased 12.9% year over year, the highest growth in fourteen quarters. IDC expects compute and storage spending by service providers to reach $89.1 billion in 2022, growing 18.7% year over year.

At the regional level, year-over-year spending on cloud infrastructure in 1Q22 increased in most regions. Once again Asia/Pacific (excluding Japan and China) (APeJC) grew the most at 50.1% year over year. Japan, Middle East and Africa, China, and the United States all saw double-digit growth in spending. Western Europe grew 6.4% and growth in Canada slowed to 1.2%. Central & Eastern Europe, affected by the war between Russia and Ukraine, declined 10.3%, while Latin America declined 11.3%. For 2022, cloud infrastructure spending for most regions is expected to grow, with four regions, APeJC, China, the U.S., and Western Europe, expecting to post annual growth in the 20-25% range. Impact of the war will continue to hurt spending in Central and Eastern Europe, which is now expected to decline 54.6% in 2022.

Long term, IDC expects spending on compute and storage cloud infrastructure to have a compound annual growth rate (CAGR) of 14.5% over the 2021-2026 forecast period, reaching $145.2 billion in 2026 and accounting for 69.7% of total compute and storage infrastructure spend. Shared cloud infrastructure will account for 72.6% of the total cloud amount, growing at a 15.4% CAGR. Spending on dedicated cloud infrastructure will grow at a CAGR of 12.1%. Spending on non-cloud infrastructure will grow at 1.2% CAGR, reaching $63.1 billion in 2026. Spending by service providers on compute and storage infrastructure is expected to grow at a 13.4% CAGR, reaching $140.8 billion in 2026.