It’s Only Common Sense: Stay Curious, My Friends

It’s Only Common Sense: Stay Curious, My Friends The Marketing Minute: AI Is Watching Your Marketing Habits

The Marketing Minute: AI Is Watching Your Marketing Habits

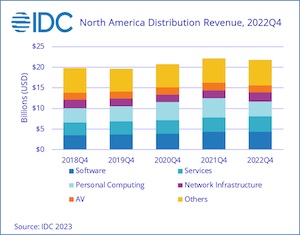

Revenue reported in the International Data Corporation (IDC) North America Distribution Tracker (NADT) for the fourth quarter of 2022 (4Q22) came in at $21.7 billion with a modest year-on-year decline of 1.8% ending the sustained growth that distribution experienced over the past two years. The soft 4Q22 results were driven by a 23% decline in personal computing but were largely offset by double-digit year-on-year growth in consumer electronics, network infrastructure, storage, and security with growth ranging from 12% to 30% in these categories.

For the full year 2022, NADT revenues reached $84.4 billion, an increase of 6.8% year on year. Personal computing and peripherals & accessories were each down more than 3% year on year while all other categories saw positive growth for the year.

"Tier 1 IT distributors continued to perform exceptionally well in a difficult environment despite the slowdown in personal computing and other categories in the fourth quarter," said Ruth Flynn, research vice president, IDC Tracker & Data Products. "While overall revenues were down slightly, the breadth of their portfolio and performance against the broader market remains strong. For example, NADT personal computing device revenues were about 1% ahead of projected PC revenues in Q4 and 5% ahead for the year, while overall NADT revenue growth was in-line with projected total IT spending growth in North America according to IDC’s Worldwide Black Book Forecast."

Notebook sales, which typically account for two thirds of personal computing device sales, declined 29% year on year and 30% compared to the previous quarter, the largest product decline in NADT Personal Computing revenue since 2018. In contrast, NADT revenues in the enterprise space saw strong double-digit growth (with a large boost from Seagate HDDs with over 500% growth in Q4 2022).

IDC's North America Weekly Distribution Tracker is built on the exclusive partnership between IDC and the Global Technology Distribution Council (GTDC) and provides the industry's most comprehensive view of technology distribution data and market trends in the U.S. and Canada. The data in this Tracker is actual sales data collected weekly from sales receipts across the largest distributors in North America for more than 1,700 brands over several years. This data is mapped to IDC's taxonomy with nearly 200 categories organized into 14 distinct product groups with detailed product attributes across categories.