The Hidden Enabler of Autonomous Warfare: Advanced PCB Technologies Behind Defense AI

The Hidden Enabler of Autonomous Warfare: Advanced PCB Technologies Behind Defense AI It’s Only Common Sense: Stay Curious, My Friends

It’s Only Common Sense: Stay Curious, My Friends

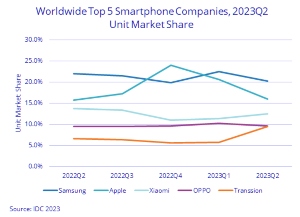

Worldwide smartphone shipments declined 7.8% year over year to 265.3 million units in the second quarter of 2023 (2Q23), according to preliminary data from the International Data Corporation (IDC) Worldwide Quarterly Mobile Phone Tracker. While this marks the eighth consecutive quarter of contraction as the market struggles with soft demand, inflation, macroeconomic uncertainties, and excess inventory, the rate of decline is slowing compared to previous quarters.

"The good news is that inventory levels are improving and the latest market chatter suggests that by Q3 excess inventory in finished devices and components should clear up," said Nabila Popal, research director with IDC's Mobility and Consumer Device Trackers. "As inventory levels normalize, we are finally hearing optimism from key OEMs and supply chains and expect the market to return to growth by the end of the year and into 2024. As the market ramps back up, it is also an opportunity for vendors to gain share. IDC expects a shift in the vendor rankings at the bottom of the stack, as we already see happening this quarter with Transsion entering the Top 5 for the first time."

China witnessed a year-over-year decline of 2.1% in 2Q23 after five quarters of significant double-digit contractions. While this is better than past quarters, consumer sentiment and spending remain low. Even the much awaited 618 online shopping festival in June, which was expected to boost sales in China, saw a 6.5% year-over-year drop in smartphone sales. The other large regions, including Asia/Pacific (excluding Japan and China), the United States, and Europe, the Middle East, and Africa (EMEA), also saw shipments decline by 5.9%, 19.1%, and 3.1% respectively in 2Q23.

"Although the first half of the year has presented many challenges to the market, we believe that there remains plenty of opportunity awaiting in the second half of the year," said Anthony Scarsella, research director, Mobile Phones at IDC. "The foldable market remains an exciting product to consumers, and the arrival of new models and new vendors joining the race will hopefully translate to wider adoption and lower prices. Moreover, we expect the foldable market to grow nearly 50% in 2023 while the total market remains down."