The Hidden Enabler of Autonomous Warfare: Advanced PCB Technologies Behind Defense AI

The Hidden Enabler of Autonomous Warfare: Advanced PCB Technologies Behind Defense AI It’s Only Common Sense: Stay Curious, My Friends

It’s Only Common Sense: Stay Curious, My Friends

TrendForce reports global smartphone production has faced back-to-back quarterly declines. After plunging nearly 20% in 1Q23, second-quarter numbers dwindled further by approximately 6.6%, settling at a modest 272 million units. The first half of 2023 clocked in at a mere 522 million units—marking a 13.3% YoY decline and setting a ten-year low for both individual quarters and the first half of the year combined.

TrendForce identifies three key reasons behind this slump in production:

- The easing of pandemic restrictions in China failed to spur demand.

- The demographic dividend from the emerging Indian market has yet to translate into tangible demand.

- Initially, it was estimated that brands would return to normal production levels as excess inventory was cleared. However, the current economic downturn has kept consumer spending in check—undermining first-half production more than expected.

Transsion Overtakes Vivo to Enter Global Top 5, Q2 Production Surges by Over 70%

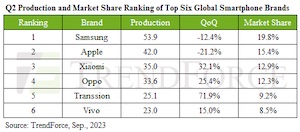

In a dramatic shake-up of global rankings, Transsion (including TECNO, Infinix, and itel) eclipsed Vivo to secure the fifth spot for the first time ever. TrendFroce reveals that Transsion’s high production output benefited from a trifecta of inventory replenishment, new product launches, and its entry into mid-to-high-end markets. Demonstrating robust production performance since March, the company’s growth trajectory is poised to extend its momentum into Q3. Meanwhile, Vivo (including Vivo and iQoo) is treading cautiously amid a sluggish global economy, which is evident in its conservative production plan: Vivo churned out 23 million units in Q2—a modest quarterly increase of 15%—and as a result, slipped to sixth place in global rankings.

Apple Closes Gap with Samsung, Vying for Global Market Leadership in 2023

Samsung continues to lead in production rankings, delivering 53.9 million units in Q2. However, it suffered a 12.4% QoQ downturn. Amid global economic headwinds and fierce competition, coupled with a waning halo effect from its flagship phone releases earlier in the year, Samsung’s Q2 performance lagged behind the same period last year. Although Samsung is set to roll out new foldable models in Q3, the impact on its overall growth is expected to be marginal given the relatively low sales volume compared to its Galaxy S series.

Apple’s second quarter is typically the weakest quarter in terms of production, owing to its transition between older and newer models. Output for the second quarter clocked in at 42 million units, marking a 21.2% dip from the preceding quarter. The upcoming iPhone 15/15 Plus could face headwinds due to suboptimal yields in its CMOS Image Sensors, potentially impacting its Q3 production performance. Intriguingly, Apple and Samsung are neck-and-neck in their annual production projections. Should the iPhone 15 series outperform market expectations, Apple stands a good chance of ousting Samsung from its long-held position as the global market leader.

Xiaomi (including Xiaomi, Redmi, and POCO) is reveling in a bountiful Q2, posting production numbers of around 35 million units—a staggering seasonal uptick of 32.1%. This boom can be attributed to a strategic depletion of channel inventory coupled with the allure of new product launches. However, Xiaomi’s channel inventory still runs high, setting the stage for a Q3 that is likely to mirror its Q2 performance. On the other side of the spectrum, Oppo (including Oppo, Real, and OnePlus) also had a fruitful Q2. The brand primarily rode the wave of rebounding demand in Southeast Asia and other regions, amassing approximately 33.6 million units and marking a seasonal leap of 25.4%. With seasonal demands on the horizon, Oppo’s Q3 production is poised for an estimated growth of 10~15%, primarily targeting markets in China, South Asia, Southeast Asia, and Latin America, hot on Xiaomi’s heels.

Overall Economic Recovery Remains Unclear, Smartphone Production May Be Further Reduced in H2

Demand in consumer markets such as China, Europe, and North America has not shown a significant rebound as we move into the second half of the year. Even if economic indicators in the Indian market improve, it is still difficult to reverse the global decline in smartphone production. TrendForce predicts that the smartphone market may undergo another shift in Q2 this year due to poor global economic conditions, and production for the second half may consequently be further reduced. Looking ahead to 2024, the current economic outlook is not optimistic. TrendForce maintains its forecast of a 2~3% annual increase in global production, depending on regional economic trends. Whether this will further drag down production remains to be seen.