Trouble in Your Tank: Understanding Interconnect Defects, Part 1

Trouble in Your Tank: Understanding Interconnect Defects, Part 1 It’s Only Common Sense: Marketing Isn’t Fluff, It’s Ammunition

It’s Only Common Sense: Marketing Isn’t Fluff, It’s Ammunition Driving Innovation: Mechanical and Optical Processes During Rigid-flex Production

Driving Innovation: Mechanical and Optical Processes During Rigid-flex Production

Reduced Production Capacity May Become Short-Term Norm for MLCC Suppliers as Consumer Market Slumps

May 18, 2023 | TrendForceEstimated reading time: 2 minutes

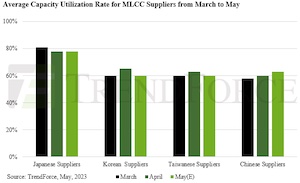

TrendForce reports that global economic headwinds have had a significant impact on the MLCC industry, with shipments from January to April of this year totaling 1.359 trillion units. This represents a 34% decrease compared to the same period in 2021, highlighting the greater impact of global economic headwinds on the MLCC industry compared to the pandemic. An unstable demand for orders from brands and ODMs since 2Q23, coupled with continuous price pressure, has forced MLCC suppliers to control capacity in order to maintain a balance among supply, inventory, and pricing. In May, the average capacity utilization rate of Japanese suppliers was 78%, while Chinese, Taiwanese, and South Korean suppliers stood around 60–63%. Reduced production may become a short-term norm as consumer demand continues to remain weak.

New smartphone releases from Huawei, Honor, and OPPO in the second quarter have failed to effectively boost China’s domestic market consumption, leading brands to adopt a more conservative approach to promoting new products. In the server segment, current estimates project a 2.85% YoY decline in total shipments for the year, with potential further downward adjustments. This will affect material depletion for ODMs, including Inventec, Quanta, and Wistron. Average inventory levels remained high at 4–8 weeks as of the end of April.

ODMs began mass production and shipments of Intel’s 13th generation Raptor Lake CPU platform for both consumer and business models in March—coinciding with the three-year replacement cycle since the pandemic. However, Quanta and Compal, the top two ODMs, reported shipments of only 3.3 million and 2.4 million units in April, respectively. Comparatively, during the same period last year when China was under lockdown and supply chains were disrupted, shipment volumes still managed to reach 3.2 million and 2.2 million units, respectively. This underlines the current sluggish demand in the end-user market, and combined with economic uncertainties, has led OEMs to adopt a more conservative outlook for new product launches.

TrendForce further states that previously, the market generally believed inventory pressure was the main factor impacting the MLCC industry. However, for smartphones, PCs, and laptops, which account for 30% of MLCC demand, ODMs began adjusting their inventory levels as early as the third quarter of last year. By 2Q23, they had gradually returned to normal, with occasional urgent and short orders replenishing stock. Nevertheless, overall demand is still weak due to the sluggish consumer market, resulting in low and unsustainable demand for MLCCs from buyers. In May, the MLCC supplier BB ratio was 0.85, only a slight increase of 0.01 compared to April, indicating extremely low order growth.

Looking ahead to the third quarter, although brands and ODMs still hope the traditional peak season can stimulate demand recovery, the forecasted growth rate for MLCC order volume remains low, hardly reflecting the usual uptick expected during the peak season. One notable exception is the Japanese firm, Murata, which recently bagged an order for components for Apple’s iPhone 15, set to debut in 3Q23. The order volume has already nudged past last year’s figures, indicating that Apple is confident the upgraded hardware and software of the iPhone 15 will continue to turn heads in the consumer market.

Share on:

Testimonial

"Advertising in PCB007 Magazine has been a great way to showcase our bare board testers to the right audience. The I-Connect007 team makes the process smooth and professional. We’re proud to be featured in such a trusted publication."

Klaus Koziol - atgSuggested Items

It’s Only Common Sense: Marketing Isn’t Fluff, It’s Ammunition

11/03/2025 | Dan Beaulieu -- Column: It's Only Common SenseI’ve lost count of the times I’ve heard someone dismiss marketing as “fluff.” You know the tone: a little smirk, a little condescension, and the implication that “real companies” don’t need marketing. They say, “We make a great product. Our work speaks for itself.”

Aircraft Wire and Cable Market to surpass USD 3.2 Billion by 2034

10/30/2025 | Global Market Insights Inc.The global aircraft wire and cable market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 3.2 billion by 2034, according to recent report by Global Market Insights Inc.

The Marketing Minute: Marketing With Layers

10/15/2025 | Brittany Martin -- Column: The Marketing MinuteMarketing to a technical audience is like crafting a multilayer board: Each layer serves a purpose, from the surface story to the buried detail that keeps everything connected. At I-Connect007, we’ve learned that the best marketing campaigns aren’t built linearly; they’re layered. A campaign might start with a highly technical resource, such as an in-depth article, a white paper, or a podcast featuring an engineer delving into the details of a process. That’s the foundation, the substance that earns credibility.

ICT Symposium Review: Sustainability and the Circular Economy

10/09/2025 | Pete Starkey, I-Connect007It was pleasant autumnal weather as we made our way once again to Meriden, the nominal centre of England, for the 2025 Annual Symposium of the Institute of Circuit Technology. Delegates were welcomed by technical director Emma Hudson who introduced and moderated a skilfully coordinated programme, focused on the highly relevant theme of sustainability.

Circular Packaging Market to Reach $98.0 Billion by 2035

10/08/2025 | Fact.MRThe market's journey from USD 45.8 billion in 2025 to USD 98.0 billion by 2035 represents substantial growth, the market will rise at a CAGR of 7.9% demonstrating the accelerating adoption of sustainable packaging systems and circular economy solutions across food & beverage, personal care, and e-commerce sectors.