Trouble in Your Tank: Understanding Interconnect Defects, Part 1

Trouble in Your Tank: Understanding Interconnect Defects, Part 1 It’s Only Common Sense: Marketing Isn’t Fluff, It’s Ammunition

It’s Only Common Sense: Marketing Isn’t Fluff, It’s Ammunition Driving Innovation: Mechanical and Optical Processes During Rigid-flex Production

Driving Innovation: Mechanical and Optical Processes During Rigid-flex Production

DRAM Industry Q1 Revenues Decline 21.2% QoQ

May 25, 2023 | TrendForceEstimated reading time: 2 minutes

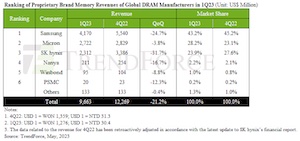

TrendForce reports a dramatic 21.2% QoQ decline in Q1 revenues for the DRAM industry, bringing total revenue down to US$9.663 billion. This significant dip represents the third consecutive quarter where revenues have fallen. A closer look reveals that increased shipment volumes were exclusive to Micron, with other suppliers noting a decrease. The ASP fell for all three major suppliers. An enduring oversupply issue, which has led to an ongoing slump in prices, is the chief culprit behind the decline. Nevertheless, the industry expects a gradual slowing in the rate of price decline following planned production cuts. TrendForce’s Q2 forecast suggests a rise in shipments, but the ongoing price fall might limit potential revenue growth.

Each of the three major suppliers—Samsung, Micron, and SK hynix—reported a drop in quarterly revenue. Samsung saw a decline in both shipment volumes and ASP due to fewer orders for its newly launched devices, resulting in a QoQ decrease in revenue of 24.7%, amounting to about US$4.17 billion. Benefiting from its earlier financial reporting and the tail-end orders of the previous year, Micron climbed to the second position in 1Q23. Despite being the only supplier among the big three to record positive shipment growth, Micron couldn't avoid a minor 3.8% revenue decline, taking its total down to US$2.72 billion. SK hynix faced the steepest decline, with more than a 15% drop in both shipment volume and ASP, leading to a drastic 31.7% plunge in revenue, amounting to approximately USD$2.31 billion.

TrendForce's earlier prediction of the big three shifting from profitability to loss in 1Q23 due to a swift ASP decline came true. With DRAM prices continuing to fall, it's anticipated that Q2 operating profit margins will remain in the red. In response to this, all three major suppliers have started implementing production cuts, with Q2 capacity utilization rates expected to fall to 77% for Samsung, 74% for Micron, and 82% for SK hynix.

In terms of Taiwanese suppliers, Nanya faced a decline in shipments for the fourth consecutive quarter, with Q1 revenues dropping by 16.7%. Mainstream process nodes remained stagnant at 20 nm, lagging behind the big three, leading to a substantial decline in operating profit margins to -44.9%. However, there is a glimmer of hope as the replenishment demand for TV SoC inventory is anticipated to lift the Q2 utilization rate back up to 80% from 70%. Despite receiving several emergency orders for laptops and TVs in Q1, Winbond reported an 8.8% decline in revenues as prices continued to fall. Amidst falling prices and sluggish demand, PSMC experienced a 12.3% dip in its quarterly DRAM revenue. The company's financial performance is primarily tied to its own consumer DRAM products, excluding the revenue from its DRAM foundry services. However, if the foundry service revenue were to be included, the company's quarterly decline would steepen to 22.6%.

Share on:

Testimonial

"Advertising in PCB007 Magazine has been a great way to showcase our bare board testers to the right audience. The I-Connect007 team makes the process smooth and professional. We’re proud to be featured in such a trusted publication."

Klaus Koziol - atgSuggested Items

The Chemical Connection: Onshoring PCB Production—Daunting but Certainly Possible

10/22/2025 | Don Ball -- Column: The Chemical ConnectionIn the past year, several potential customers, concerned about the impending application of tariffs on incoming goods, have asked us what it would take to bring their circuit board production back to the U.S. While they also had other considerations, the threat of new tariffs was the tipping point that started them thinking about the economic advantages of bringing their manufacturing back onshore. It might be interesting to relate our experiences with two of those inquiries.

Global Sourcing Spotlight: Balancing Speed and Flexibility Without Sacrificing Control

10/15/2025 | Bob Duke -- Column: Global Sourcing SpotlightIn global sourcing, speed is a necessity; however, speed without flexibility is a recipe for chaos. Likewise, flexibility without structure leads to inefficiency. Companies thrive when they build agile global sourcing strategies that allow them to move quickly while adapting to market fluctuations, customer demands, and supply chain disruptions. Here’s how leading organizations successfully navigate the critical gap between speed and flexibility in global sourcing.

Beyond the Board: Early Engagement Means Faster Prototyping for Defense Programs

10/14/2025 | Jesse Vaughan -- Column: Beyond the BoardIn the defense electronics sector, speed-to-market has shifted from being a commercial differentiator to a national security imperative. The ability to move from design concept to deployable system in months rather than years can provide the U.S. with important strategic advantages. Prototyping, once regarded as a costly and optional stage, has become the linchpin for accelerating program schedules while safeguarding performance, compliance, and mission reliability.

Technica Hosts In-House Visit from PCBAA

10/01/2025 | Technica USADavid Schild, Executive Director of PCBAA (Printed Circuit Board Association of America) visited Technica USA to discuss the activity in the market and the advocacy of the PCBAA. The organization was formed to work on Capitol Hill, educating, advocating and getting congressional support to legislate on behalf of building a stronger PCB and substrate manufacturing base in the U.S.A.

Global Sourcing Spotlight: Finding the Balance Between Cost and Quality

09/24/2025 | Bob Duke -- Column: Global Sourcing SpotlightIn global sourcing, pursuing lower costs often takes center stage. It’s the shiny lure that gets buyers to cast their lines into unfamiliar waters. But seasoned professionals know that in the long run, sourcing is less about price tags and more about value. The real magic—and margin—lies in finding the balance between cost and quality.