The Right Approach: I Hear the Train A Comin'

The Right Approach: I Hear the Train A Comin' It’s Only Common Sense: OCCAM—the Time Is Now

It’s Only Common Sense: OCCAM—the Time Is Now Marcy's Musings: The Growing Industry

Marcy's Musings: The Growing IndustryWorldwide Ethernet Switch Market Up 3.3% YoY in 1Q 2017

June 13, 2017 | IDCEstimated reading time: 6 minutes

The worldwide Ethernet switch market (Layer 2/3) recorded $5.66 billion in revenue in the first quarter of 2017 (1Q17), an increase of 3.3% year over year. Meanwhile, the worldwide total enterprise and service provider (SP) router market recorded $3.35 billion in revenue in 1Q17, decreasing 3.7% on a year-over-year basis. These growth rates are according to results published in the International Data Corporation (IDC) Worldwide Quarterly Ethernet Switch Tracker and Worldwide Quarterly Router Tracker.

From a geographic perspective, the 1Q17 Ethernet switch market once again recorded its strongest growth in the Middle East and Africa (MEA) region, which increased a solid 9.1% year over year. At the country level, the United Arab Emirates (up 38.2% year over year) and South Africa (up 25.6% year over year) were among the standouts. Western Europe also saw strong growth, increasing 6.0% year over year in 1Q17, with Belgium (up 27.6% year over year) and Sweden (up 12.0% year over year) as growth pacesetters. Asia/Pacific (excluding Japan)(APeJ) grew at a rate just above the overall market with a 3.5% year-over-year increase in 1Q17. New Zealand (up 20.5% year overyear) was the regional growth leader in 1Q17. North America grew at a below-market rate in 1Q17, increasing 2.5% on a year-over-year basis, with Canada increasing at a stronger 4.5%.

Latin America experienced flat-to-declining performance in 1Q17, with a 0.4% contraction year-over-year. Argentina was a bright spot in the quarter, growing 57.4% on an annualized basis. Japan, in a reversal from the previous quarter, declined 0.6%. Central and Eastern Europe saw the steepest decline of 1Q17, contracting 2.4% year-over-year, as declines in Poland (down 30.4% year-over-year) and Czech Republic (down 29.2%) weighed on the region.

"The Ethernet switch market, across the enterprise and Datacenter segments, is characterized by two competing forces: faster speeds and increased standardization," said Rohit Mehra, vice president, Network Infrastructure at IDC. "Both forces drive port shipments up, but price erosion from standardization and product maturity means that improved price-performance becomes more important across regions. That said, continued penetration of cloud coupled with the digital transformation imperative will drive market growth throughout 2017."

10Gb Ethernet switch (Layer 2/3) revenue decreased 1.6% year over year in 1Q17, coming in at $1.98 billion, while 10Gb Ethernet switch port shipments grew 23.9% year over year with over 10.7 million ports shipped in 1Q17. 40Gb Ethernet revenue came in at $609.5 million in 1Q17, declining 7.2% over 1Q16, while port shipments fell just below 1.3 million, representing a decrease of 21.9% year over year. 10Gb and 40Gb Ethernet are now joined by emerging 100Gb Ethernet (revenue up 323.5% and shipments up 776.4% on annualized basis in 1Q17) to be the primary drivers of the overall Ethernet switch market. 1Gb Ethernet switch revenue decreased 0.5% year over year in 1Q17, despite a 11.0% increase in port shipments in the same period, pointing to a maturing campus segment.

The worldwide enterprise and service provider router market contacted 3.7% on a year-over-year basis in 1Q17 based on a 4.4% decrease in the larger service provider segment and a 1.4% decrease in enterprise routing. This will be a market to watch closely over the coming quarters as software-defined architectures start to take hold across the WAN, with the potential for SD-WAN to disrupt traditional routing architectures and WAN transport services markets especially at the network edge.

The combined enterprise and service provider router market saw a varied regional performance in 1Q17, with APeJ recording the strongest growth (up 8.8% year over year). Japan, the only other region to record growth, increased 5.2% year over year in 1Q17. MEA was down 1.0%, while CEE declined 4.1% over the period. Other regions saw greater declines in 1Q17. Western Europe was down 7.1% on annualized basis, while North America contracted 9.8%. Latin America saw the steepest decline of all, decreasing 23.4% over 1Q16.

Vendor Highlights

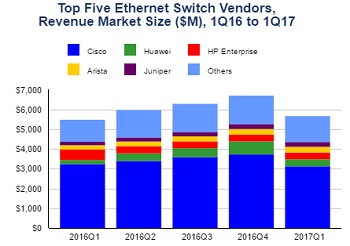

Cisco finished 1Q17 with a year-over-year decline of 3.5% in the Ethernet switching market and market share of 55.1%, down from its 55.6% share in 4Q16 and down from 59.0% in 1Q16. In the vigorously contested 10GbE segment, Cisco held 52.4% of the market in 1Q17, down from 53.0% in the previous quarter. Cisco saw its combined service provider and enterprise router revenue decrease 13.3% on an annualized basis, while its market share came in at 43.9% in 1Q17, up from 42.2% in 4Q16, but down from 48.8% in 1Q16.

Huawei continued to perform well in both the Ethernet switch and the router markets on an annualized basis. Huawei's Ethernet switch revenue grew 69.8% year over year in 1Q17 for a market share of 6.3%, down from 9.9% in 4Q16 and up from 3.9% in 1Q16. Huawei's enterprise and SP router revenue increased 17.0% over the same period, to finish with 19.8% of the total router market in 1Q17 compared to 18.8% in 4Q16 and 16.3% in 1Q16.

Hewlett Packard Enterprise's (HPE) Ethernet switch revenue grew 0.8% sequentially in 1Q17 and its market share stands at 6.0% in 1Q17, up from its 5.0% share in 4Q16. (Note: HPE and H3C are tracked separately as of 2Q16).

Arista Networks performed well in 1Q17, with its Ethernet switching revenue rising 37.1% year over year and earning a market share of 5.1%, up from 3.9% in 1Q16. Arista's market share in the 100Gb segment stands at 27.8%.

Juniper's Ethernet switching increased by a notable 39.2% year over year in 1Q17, bringing its market share to 4.3% versus 3.2% in 1Q16. Juniper also saw a 3.4% year-over-year increase in combined service provider and enterprise router revenues, with market share of 15.6%, compared to 14.5% in 1Q16.

"Cloud and software-defined architectures are starting to shake up the status quo in the Ethernet switch and router markets," said Petr Jirovsky, research manager, Worldwide Networking Trackers. "This is already impacting leading and upstart networking vendors in various ways and points to an imperative for vendors to adapt and be nimble, and not depend on the status quo."

The Worldwide Quarterly Ethernet Switch Tracker and the Worldwide Quarterly Router Tracker provide total market size and vendor shares for the Ethernet switch and router technologies in an easy-to-use Excel pivot table format. The geographic coverage for both the Ethernet switch market and the router market includes eight major regions (USA, Canada, Latin America, Asia/Pacific (excluding Japan), Japan, Western Europe, Central and Eastern Europe, and Middle East and Africa) and 60 countries. The Ethernet switch market is further segmented by speed (100Mb, 1000Mb, 10Gb, 40Gb, 100Gb), product (fixed managed, fixed unmanaged, modular), and layer (L2, L3, ADC). Measurement for the Ethernet switch market is provided in vendor revenue, value, and port shipments. The router market is further split by product (high-end, mid-range, low-end, SOHO), deployment (service provider, enterprise), connectivity (core, edge), and the measurements are in vendor revenue, value, and unit shipments.

About IDC Trackers

IDC Tracker products provide accurate and timely market size, vendor share, and forecasts for hundreds of technology markets from more than 100 countries around the globe. Using proprietary tools and research processes, IDC's Trackers are updated on a semiannual, quarterly, and monthly basis. Tracker results are delivered to clients in user-friendly excel deliverables and online query tools.

About IDC

International Data Corporation (IDC) is the premier global provider of market intelligence, advisory services, and events for the information technology, telecommunications, and consumer technology markets. With more than 1,100 analysts worldwide, IDC offers global, regional, and local expertise on technology and industry opportunities and trends in over 110 countries. IDC's analysis and insight helps IT professionals, business executives, and the investment community to make fact-based technology decisions and to achieve their key business objectives. Founded in 1964, IDC is a wholly-owned subsidiary of International Data Group (IDG), the world's leading media, data and marketing services company that activates and engages the most influential technology buyers.

Share on:

Suggested Items

Amphenol Reports Q1 2024 Results, Announces New Stock Repurchase Program

04/26/2024 | BUSINESS WIREAmphenol Corporation reported first quarter 2024 results. In addition, the Company is announcing a new three-year, $2 billion stock repurchase program.

Chinese Smartphone Market Maintains its Recovery Momentum at 6.5% Growth in 1Q24,

04/26/2024 | IDCAccording to preliminary data from the International Data Corporation (IDC) Worldwide Quarterly Mobile Phone Tracker, China smartphone shipments grew 6.5% year over year (YoY) to 69.3 million units in 1Q24.

Nanotechnology Market to Surpass $53.51 Billion by 2031

04/25/2024 | PRNewswireSkyQuest projects that the nanotechnology market will attain a value of USD 53.51 billion by 2031, with a CAGR of 36.4% over the forecast period (2024-2031).

Technica USA Presents Inaugural Supplier Alliance Award at IPC APEX EXPO 2024

04/24/2024 | Technica USADuring IPC APEX EXPO 2024, Technica USA took the opportunity to thank all of their supply partners that made the effort to join them for the exhibition in their booth, as well to all of our SMT partners that had their own booths, with the latest in automation and process technology.

IDTechEx Report Unveils 3D Electronics Status and Opportunities

04/22/2024 | PRNewswire3D electronics is an emerging manufacturing approach that enables electronics to be integrated within or onto the surface of objects. 3D electronic manufacturing techniques empower new features, including mass customizability, greater integration, and improved sustainability in the electronics industry.