Driving Innovation: Mechanical and Optical Processes During Rigid-flex Production

Driving Innovation: Mechanical and Optical Processes During Rigid-flex Production It’s Only Common Sense: Your Biggest Competitor Is Complacency

It’s Only Common Sense: Your Biggest Competitor Is Complacency The Chemical Connection: Onshoring PCB Production—Daunting but Certainly Possible

The Chemical Connection: Onshoring PCB Production—Daunting but Certainly Possible

Global Smartphone Shipments Down 6% in Q3 2018

November 2, 2018 | IDCEstimated reading time: 6 minutes

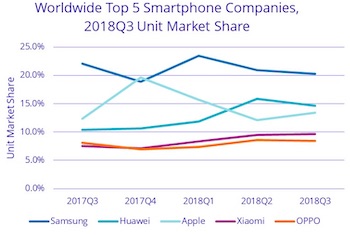

According to preliminary data from the International Data Corporation (IDC) Worldwide Quarterly Mobile Phone Tracker, smartphone vendors shipped a total of 355.2 million units during the third quarter of 2018 (3Q18), resulting in a year-over-year decline of 6.0%. This was the fourth consecutive quarter of year-over-year declines for the global smartphone market, which raises questions about the market's future. IDC maintains its view that the market will return to growth in 2019, but at this stage it is too early to tell what that growth will look like.

While the overall smartphone market has declined for four straight quarters, two things stand out as major factors in the third quarter. Samsung, the largest smartphone vendor in terms of market share, accounting for 20.3% of shipments in 3Q18, declined 13.4% year over year in the quarter. And secondly, China, which is the largest country market for smartphone consumption, accounting for roughly one third of global shipments, was down as well for the sixth consecutive quarter.

Samsung had a challenging quarter with shipments down 13.4% to 72.2 million units shipped. The market share leader continues to feel pressure from all directions, especially with Huawei inching closer to the top after its second consecutive quarter as the number two vendor. In addition, growing markets like India and Indonesia, where Samsung has held leading positions for many years, are being changed by the rapid growth of Chinese brands like Xiaomi, OPPO, and vivo.

Meanwhile, China’s domestic market, which represents roughly one third of all smartphones consumed, has been in decline since the second quarter of 2017, and 3Q18 was the sixth consecutive quarter where the market sees contraction. China was down 11% in the first half of 2018 (1H18), and the challenges continued into 3Q18. Overall IDC expects this decline to decelerate with the market returning to flat growth in 2019.

"China's domestic market continues to be challenged as overall consumer spending around smartphones has been down," said Ryan Reith, program vice president with IDC's Worldwide Mobile Device Trackers. "High penetration levels, mixed with some challenging economic times, has slowed the world's largest smartphone market. Despite this, we believe this market will begin to recover in 2019 and beyond, driven in the short term by a large, built up refresh cycle across all segments, and in the outer years of the forecast supported by 5G migration."

"The race at the top of the market continues to be a heated one as Huawei once again slipped past Apple to the second position," said Anthony Scarsella, research manager with IDC's Worldwide Quarterly Mobile Phone Tracker. "Although Huawei may have beat out Apple in Q3, the holiday quarter could have Apple as the market leader thanks to the launch of three new bezel-less devices. No matter who leads in the overall market the holiday quarter should be an exciting one with a wide selection of new flagship devices available. With the new iPhones, Mate 20, Pixel 3, V40, Note 9, and OnePlus 6T, we can expect consumers will have a plethora of options when upgrade time approaches. The vast selection of high-priced handsets should move ASPs in a positive direction come next quarter."

Page 1 of 2

Share on:

Testimonial

"The I-Connect007 team is outstanding—kind, responsive, and a true marketing partner. Their design team created fresh, eye-catching ads, and their editorial support polished our content to let our brand shine. Thank you all! "

Sweeney Ng - CEE PCBSuggested Items

Aircraft Wire and Cable Market to surpass USD 3.2 Billion by 2034

10/30/2025 | Global Market Insights Inc.The global aircraft wire and cable market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 3.2 billion by 2034, according to recent report by Global Market Insights Inc.

The Marketing Minute: Marketing With Layers

10/15/2025 | Brittany Martin -- Column: The Marketing MinuteMarketing to a technical audience is like crafting a multilayer board: Each layer serves a purpose, from the surface story to the buried detail that keeps everything connected. At I-Connect007, we’ve learned that the best marketing campaigns aren’t built linearly; they’re layered. A campaign might start with a highly technical resource, such as an in-depth article, a white paper, or a podcast featuring an engineer delving into the details of a process. That’s the foundation, the substance that earns credibility.

ICT Symposium Review: Sustainability and the Circular Economy

10/09/2025 | Pete Starkey, I-Connect007It was pleasant autumnal weather as we made our way once again to Meriden, the nominal centre of England, for the 2025 Annual Symposium of the Institute of Circuit Technology. Delegates were welcomed by technical director Emma Hudson who introduced and moderated a skilfully coordinated programme, focused on the highly relevant theme of sustainability.

Circular Packaging Market to Reach $98.0 Billion by 2035

10/08/2025 | Fact.MRThe market's journey from USD 45.8 billion in 2025 to USD 98.0 billion by 2035 represents substantial growth, the market will rise at a CAGR of 7.9% demonstrating the accelerating adoption of sustainable packaging systems and circular economy solutions across food & beverage, personal care, and e-commerce sectors.

It’s Only Common Sense: Stop Whining About the Market—Outwork It

10/06/2025 | Dan Beaulieu -- Column: It's Only Common SenseWhenever the market hiccups or the industry cycle dips, I hear the same tired chorus: “The market is down. Customers aren’t buying. What can we do? We just have to wait it out.” Nonsense. If you think that by showing up, opening your doors, and waiting for the economy to smile kindly upon you, that success will follow, you are in the wrong business. Worse yet, you’re living in the wrong mindset. Most people don’t want to hear the truth that winners find business in down cycles. Losers blame the economy.