Dan’s Biz Bookshelf: ‘The New Age of Innovation’

Dan’s Biz Bookshelf: ‘The New Age of Innovation’ It’s Only Common Sense: The Customer Isn’t Always Right

It’s Only Common Sense: The Customer Isn’t Always Right The Marketing Minute: Building Connections in the Electronics Industry

The Marketing Minute: Building Connections in the Electronics Industry

Rising Demand Will Help the LTPS Market Reach a Healthy Equilibrium in 2019

February 14, 2019 | TrendForceEstimated reading time: 3 minutes

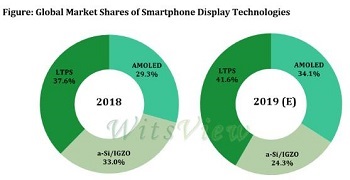

The latest analysis of the panel market by WitsView, a division of TrendForce, finds that low prices and technological maturation have substantially widened the adoption of LTPS panels among smartphone makers. The share of devices featuring LTPS panels in the global smartphone market is projected to grow from 37.6% in 2018 to 41.6% in 2019. However, panel suppliers have ended large-scale expansions of their production capacity for LTPS panels since they are gradually shifting their technological focus for smartphone displays to AMOLED. On the whole, 2019 is expected to be a year during which the market for LTPS panels will be at its healthiest state in terms of supply and demand.

Boyce Fan, the research director of WitsView, pointed out that the activation of the new Gen-6 LTPS lines in China has expanded the total production capacity and ratcheted up the price competition among suppliers. Furthermore, panel suppliers have steadily improved their LTPS manufacturing processes and generally attained a decent level of technical maturity. Hence, smartphone makers are now more receptive to the adoption of the LTPS technology, which is also seeing a rapid increase in its market visibility.

On the other hand, the price decline for LTPS panels is easing due to new trends in smartphone design and panel manufacturing. “The screen of devices has become larger because the full-screen design is now the market mainstream,” said Fan. “At the same time, the notch cut-out and the use of the COF (chip-on-film) package for driver ICs have made panel fabrication more challenging and increased the amount of waste glass during the process. These observations imply that the area of glass needed for producing smartphone panels has expanded in order compensate for the lower yield rate, and this in turn is pushing the LTPS market toward a more stable supply-demand balance.”

Panel suppliers have steadily shifted their focus to AMOLED in their development of smartphone panels, and they are now aggressively boosting their production capacity for the technology. The total production capacity for AMOLED panels is expected to keep growing over the next few years, raising the chance of oversupply. Conversely, the growth in the total production capacity for LTPS panels has tapered off. Because prices of LTPS panels are now relatively low, there is a greater potential for raising the consumption of the LTPS capacity as smartphone makers look for ways to upgrade the hardware specifications of their devices. Moreover, LTPS is gradually making inroads in other applications as well, such as in-vehicle displays and notebook displays. WitsView therefore believes that the market for LTPS panels will move away from oversupply and reach a healthy equilibrium in the short term.

WitsView also contends that the prospect of the LTPS technology maintaining its market leadership during the next several years will hinge on the progress that the Chinese panel suppliers have made in advancing their AMOLED technology. Chinese panel suppliers are currently ramping up production on their new AMOLED lines, and WitsView expects that the supply pressure on the AMOLED market will build up to a very high level in 2020. Some of the new production lines in China will also have been in operation for more than a year in 2020. The capacity growth, together with anticipated improvements in the cost and technical aspects of the manufacturing process, will probably make AMOLED more of a threat to the market share of LTPS by that time.

The competition between LTPS and AMOLED in the mid-to-high range of the smartphone market has been especially fierce and will intensify in the future. When AMOLED edges out LTPS and becomes mainstream in the mid-to-high range segment, then the market for the latter technology will again face oversupply. To mitigate the effect of this anticipated scenario, suppliers of LTPS panels will be concentrating their promotional efforts in the lower rungs of of the smartphone market. This move in turn will accelerate the decline in market share for the a-Si technology in the lower-end segments. Suppliers of LTPS panels can also adjust their product mixes to give more weight to applications other than smartphone displays. In sum, targeting the lower-end segments of the smartphone market and developing products for other applications are likely going to be the main components of a strategy to lessen the market impact from the maturation of the AMOLED technology.

About TrendForce

TrendForce is a global provider of the latest development, insight, and analysis of the technology industry. Having served businesses for over a decade, the company has built up a strong membership base of 435,000 subscribers. TrendForce has established a reputation as an organization that offers insightful and accurate analysis of the technology industry through five major research divisions: DRAMeXchange, WitsView, LEDinside, EnergyTrend and Topology. Founded in Taipei, Taiwan in 2000, TrendForce has extended its presence in China since 2004 with offices in Shenzhen and Beijing.

Share on:

Suggested Items

Betamek Achieves Top Level 5 in MaRii’s Supplier Competitiveness Assessment

01/21/2025 | BetamekBetamek Berhad, an original design manufacturer (ODM) and a leading player in electronics manufacturing services (EMS) for the automotive industry, proudly announces that its wholly-owned subsidiary, Betamek Electronics (M) Sdn. Bhd. (Betamek Electronics), has achieved Level 5.

NovoLINC Secures Investments to Assist AI Computing with Groundbreaking Thermal Interface Technology

01/21/2025 | PRNewswireNovoLINC, a thermal technology startup spun out of Carnegie Mellon University, announced seed funding led by M Ventures, with participation from Foothill Ventures and TDK Ventures. NovoLINC's breakthrough nanocomposite thermal solutions reduce thermal resistance to an industry-record low (< 1mm²-K/W), according to company co-founders, CSO Prof. Sheng Shen and CTO Dr. Rui Cheng.

U.S. Department of Commerce Announces CHIPS Incentives Awards with Corning, Edwards Vacuum, and Infinera

01/21/2025 | U.S. Department of CommerceThe U.S. Department of Commerce announced it finalized three separate awards under the CHIPS Incentives Program’s Funding Opportunity for Commercial Fabrication Facilities.

Beyond Design: Electro-optical Circuit Boards

01/22/2025 | Barry Olney -- Column: Beyond DesignPredicting the role of PCB designers in 10 years is a challenge. If only I had a crystal ball. However, we know that as technology progresses, the limitations of copper PCBs are increasingly apparent, particularly regarding speed, bandwidth, and signal integrity. Innovations such as optical interconnects and photonic integrated circuits are setting the stage for the next generation of PCBs, delivering higher performance and efficiency. The future of PCB design will probably incorporate these new technologies to address the challenges of traditional copper-based designs.

The Pulse: Ultra Upgrade Unknowns—What’s Coming for UHDI?

01/21/2025 | Martyn Gaudion -- Column: The PulseAs we enter the second quarter of the 21st century, there appears to be a new chapter in PCB technology. Ultra high density interconnect (UHDI) has become a buzzword, but it’s actually not that new; many of the processes were already established in the high-volume production of Asian cell phones and tablets. What is new and challenging, however, is migrating the line widths and stackups—once the domain of handheld consumer products—into the lower volume specialized environment of the commercial world.