Driving Innovation: Mechanical and Optical Processes During Rigid-flex Production

Driving Innovation: Mechanical and Optical Processes During Rigid-flex Production It’s Only Common Sense: Your Biggest Competitor Is Complacency

It’s Only Common Sense: Your Biggest Competitor Is Complacency The Chemical Connection: Onshoring PCB Production—Daunting but Certainly Possible

The Chemical Connection: Onshoring PCB Production—Daunting but Certainly Possible

Contract Prices of DRAM Products Projected to Drop by 15% QoQ in 2Q19

February 19, 2019 | TrendForceEstimated reading time: 3 minutes

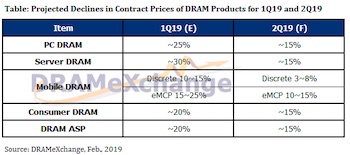

The latest analysis from DRAMeXchange, a division of TrendForce, forecasts that the ongoing oversupply will result in significant price declines for DRAM products during 1H19. Demand remains weak in 1Q19 due to the off-season and the high inventory level that was carried over from the previous quarter. Contract prices of DRAM products across all major application markets already registered declines of more than 15% MoM in January, and they will continue their descent in February and March. Regarding contract price trends in 1Q19, the PC DRAM market is forecasted to see a decline of more than 20% QoQ, while the server DRAM market may witness an even larger drop of nearly 30% QoQ.

Looking ahead to the second quarter, DRAMeXchange points out that the oversupply situation will persist despite some recovery in demand because an extended period is needed to deal with the issue of high inventory. Contract prices of mainstream DRAM products are forecasted to drop by around 15% QoQ on average in 2Q19. As for the second half of this year, DRAMeXchange believes that the uncertainties resulting from political and economic events worldwide will continue to constrain the growth in end demand. Although there are new sources of demand related to 5G, AIoT, IIoT, and automotive electronics, these application markets are still in the nascent stage of development and will not have much influence on the DRAM market in 2019. Since DRAM suppliers have also scaled back their capacity expansions, the gap between supply and demand will narrow. However, this will not be enough to stop prices from falling. Instead, the price downswing will moderate over the next several quarters.

Mobile DRAM Prices are Relatively Steady while the Decline in Server DRAM Prices is the Most Noticeable

With respect to the price trends in the major application markets, PC DRAM prices are the most sensitive to demand changes and often serve as an indicator of the overall price trajectory. The average QoQ decline in contract prices of PC DRAM products was already 10% in 4Q18 and is projected to be nearly 25% in 1Q19. Currently, the average contract price of mainstream 8GB PC DRAM modules is on its way to under $45.

Server DRAM products, which share similar attributes with PC DRAM products, had enjoyed the largest price gain during 2017 and 2018. However, a temporary slowdown in the demand for servers in 2H18 caused a pile-up of inventory in the server DRAM market. Going into 1Q19, server DRAM prices will register sharp monthly declines as inventory reduction has become a vital issue. The downswing will not start to moderate until 3Q18 at the earliest because only by then will the overall inventory of server DRAM products return to an optimal level. From the demand angle, clients operating internet data centers still want to expand their businesses, but the recovery of the stock-up demand is insignificant so far due to the constraint imposed by the excessively high inventory.

The situation is quite the opposite in the mobile DRAM market. The price increase that the mobile DRAM market attained in the 2017-2018 period was the smallest compared with the gains made by the PC DRAM and server DRAM markets. Consequently, the following price decline that the mobile DRAM market is experiencing right now is also the smallest. For 1Q19, the declines in contract prices of discrete and eMCP products are projected to be under 20% QoQ. Looking ahead to 2Q19, the mobile DRAM market will benefit from the lessening of the inventory pressure and the releases of new flagship devices from Android phone makers. Nevertheless, the overall demand growth is still going to be too weak to prevent prices from falling. DRAMeXchange forecasts that the QoQ declines in contract prices of mobile DRAM products will be around 10-15% for 2Q19.

Contract prices of specialty DRAM products are projected to drop by 10-15% QoQ in 2Q19. The specialty DRAM market will not see prices rebounding in the short term since it has many competing suppliers, and the demand for this type of products will unlikely make a strong recovery in the near future.

About TrendForce

TrendForce is a global provider of the latest development, insight, and analysis of the technology industry. Having served businesses for over a decade, the company has built up a strong membership base of 435,000 subscribers. TrendForce has established a reputation as an organization that offers insightful and accurate analysis of the technology industry through five major research divisions: DRAMeXchange, WitsView, LEDinside, EnergyTrend and Topology. Founded in Taipei, Taiwan in 2000, TrendForce has extended its presence in China since 2004 with offices in Shenzhen and Beijing.

Share on:

Testimonial

"Advertising in PCB007 Magazine has been a great way to showcase our bare board testers to the right audience. The I-Connect007 team makes the process smooth and professional. We’re proud to be featured in such a trusted publication."

Klaus Koziol - atgSuggested Items

Aircraft Wire and Cable Market to surpass USD 3.2 Billion by 2034

10/30/2025 | Global Market Insights Inc.The global aircraft wire and cable market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 3.2 billion by 2034, according to recent report by Global Market Insights Inc.

The Marketing Minute: Marketing With Layers

10/15/2025 | Brittany Martin -- Column: The Marketing MinuteMarketing to a technical audience is like crafting a multilayer board: Each layer serves a purpose, from the surface story to the buried detail that keeps everything connected. At I-Connect007, we’ve learned that the best marketing campaigns aren’t built linearly; they’re layered. A campaign might start with a highly technical resource, such as an in-depth article, a white paper, or a podcast featuring an engineer delving into the details of a process. That’s the foundation, the substance that earns credibility.

ICT Symposium Review: Sustainability and the Circular Economy

10/09/2025 | Pete Starkey, I-Connect007It was pleasant autumnal weather as we made our way once again to Meriden, the nominal centre of England, for the 2025 Annual Symposium of the Institute of Circuit Technology. Delegates were welcomed by technical director Emma Hudson who introduced and moderated a skilfully coordinated programme, focused on the highly relevant theme of sustainability.

Circular Packaging Market to Reach $98.0 Billion by 2035

10/08/2025 | Fact.MRThe market's journey from USD 45.8 billion in 2025 to USD 98.0 billion by 2035 represents substantial growth, the market will rise at a CAGR of 7.9% demonstrating the accelerating adoption of sustainable packaging systems and circular economy solutions across food & beverage, personal care, and e-commerce sectors.

It’s Only Common Sense: Stop Whining About the Market—Outwork It

10/06/2025 | Dan Beaulieu -- Column: It's Only Common SenseWhenever the market hiccups or the industry cycle dips, I hear the same tired chorus: “The market is down. Customers aren’t buying. What can we do? We just have to wait it out.” Nonsense. If you think that by showing up, opening your doors, and waiting for the economy to smile kindly upon you, that success will follow, you are in the wrong business. Worse yet, you’re living in the wrong mindset. Most people don’t want to hear the truth that winners find business in down cycles. Losers blame the economy.